Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

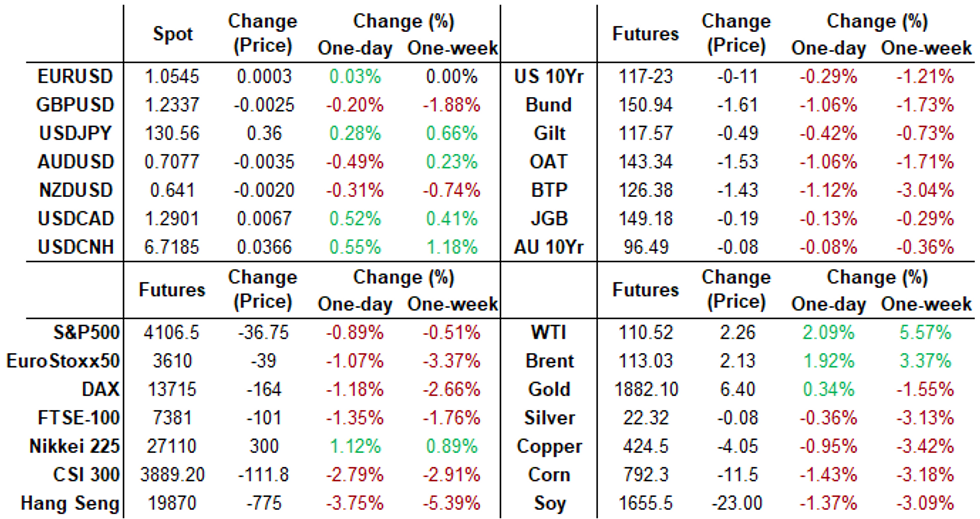

US TSYS: Yield Curves Bear Steepen, Focus on Fed over Jobs Data

Yield curves continued to bear steepen Friday, 2s10s session high of 43.067 back to early March levels as bond yields climbed to 3.2338% high -- last seen early December 2018. Relative calm end to the week for a NFP session.- Tsy futures bounced higher briefly, scaled back amid steady selling after Apr NFP jobs gained more than estimated +428k vs. +380k est, avg hourly earning little weaker than exp at 0.3% vs. 0.4% est. Total down-revisions to Feb-Mar -39k.

- Fed out of blackout: limited react to essay published by Minneapolis Fed Pres Kashkari: Long-Term Real Rates Are Already Back To Neutral. ""If the economy is in fact in a higher-pressure equilibrium, that might indicate the neutral long-term real rate has increased, which would then require even higher rates to reach a contractionary stance that would bring the economy into balance."

- MNI interview w/ Richmond Fed Barkin: interest rate increases are not on a preset course and he would like to see interest rates on a path to normal that is as fast as feasible, backing this week's historic FOMC decision to raise the fed funds rate 50bps, while not ruling out the potential for a supersized 75bp increase if needed.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00343 to 0.81857% (+0.48857/wk)

- 1M -0.00272 to 0.84214% (+0.03885/wk)

- 3M +0.03115 to 1.40186% (+0.06700/wk) * / **

- 6M -0.00757 to 1.96457% (+0.05386/wk)

- 12M +0.02257 to 2.69471% (+0.06614/wk)

- * Record Low 0.11413% on 9/12/21; ** 2Y high 1.40614% on 5/4/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $74B

- Daily Overnight Bank Funding Rate: 0.82% volume: $284B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.79%, $992B

- Broad General Collateral Rate (BGCR): 0.80%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.80%, $336B

- (rate, volume levels reflect prior session)

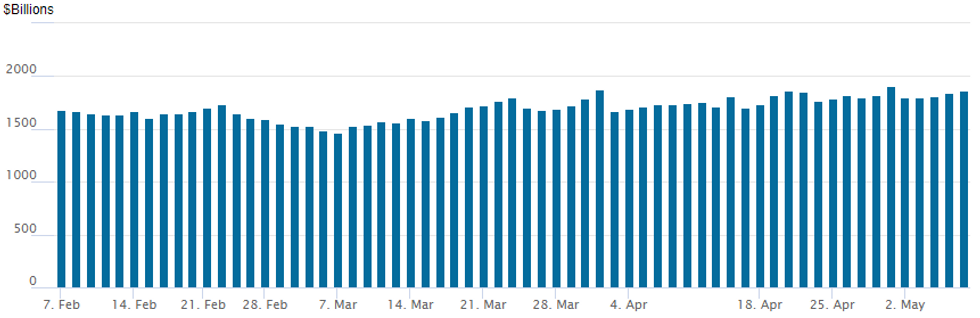

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage at 1,861.866B w/ 84 counterparties vs. prior session's 1,844.762B (all-time high of $1,906.802B on Friday, March 29, 2022).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Quiet end to a hectic policy week, active accounts continued to fade the rise in yields via upside calls/call spd buys, unwind downside puts/put spread longs, the majority of Eurodollar and Treasury option trade Friday.

SOFR Options:- +7,000 SFRU2 97.62/97.75/97.81/97.93 call condors, 1.75

- -5,000 Jun 98.12/98.18 strangles, 6.5

- -10,000 short Jun 96.37 puts, 18

- +5,000 Dec 96.75/97.00/97.25 call flys, 3.0

- Overnight trade

- 8,000 Jul 97.50 calls vs. short Jul 96.62/96.87 call spds

- +15,000 TYM 116.5/119.5 call over risk reversals, 2 ref 117-29

- -6,000 TYM 124 puts, 550

- +4,500 FVN 113 calls, 28

- +10,000 TYM 117.25 puts, 37

- -12,000 wk2 TY 116/116.5 put spds, 5

- Overnight trade

- 4,000 TYM 118.5/120 put spds

- -4,000 TYM 116.5 puts, 15-16 ref 118-00

- -4,000 TYM 118.5/120 put spds, 107 ref 118-00

- -10,000 TYM 117.25/118.5 put spds, 34

- +4,500 TYN 120 calls, 25 ref 117-11.5

- -4,500 USM 132/134/136 put trees, 22-24 ref 137-02 to -03

EGBs-GILTS CASH CLOSE: Yields Rise Again As ECB Looks More Hawkish

An apparent hawkish turn from influential ECB members applied fresh pressure on European FI Friday, with rate hike expectations rising and German yields hitting multi-year highs.

- The key comment was from Banque de France's Villeroy who said he sees rates in positive territory by year-end.

- Gilts outperformed, with the short-end continuing to rally post-dovish BoE.

- 10Y Bund yields rose to the highest since Aug 2014.

- 10Y BTP spreads rose only slightly but closed above the 200bp mark for the first time since April 2020.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.5bps at 0.32%, 5-Yr is up 8.5bps at 0.851%, 10-Yr is up 8.8bps at 1.132%, and 30-Yr is up 7bps at 1.241%.

- UK: The 2-Yr yield is down 4.1bps at 1.506%, 5-Yr is down 1bps at 1.66%, 10-Yr is up 3.1bps at 1.995%, and 30-Yr is up 4.8bps at 2.173%.

- Italian BTP spread up 0.9bps at 200.4bps / Greek up 3.6bps at 244.4bps

Euribor Plays Abound As ECB Turns More Hawkish

Friday's Europe rates / bond options flow included:

- RXM2 152/150ps sold at 61 in 3k

- RXM2 154.50/152ps 1x2, sold at 52 in 1.75k

- IKN2 124.00/121.00ps vs 125.50/126.50cs, bought the ps for 46 in 10k

- ERU2 99.87/99.75/99.62/99.37 broken put condor bought for 2.25, circa 60k total

- ERU2 100.99.87/99.75p fly, sold at 1.75 in 10k

- ERU2 99.75^ bought for 26.5, 27, and 27.5 in 12.5k total

- ERU2 99.62/99.50/99.37p fly, bought for 1.25 in 15k

- ERZ2 99.25p, sold at 20.5 up to 22.25 in 15.9k

- ERZ2 99.25^, bought for 47.5 in 4.5k

Late Equity Roundup: Mildly Lower on Week

Equity indexes weaker into the close are off session lows, upper half of range SPX emini futures, ESM2 currently -30.25 points (-0.73%) at 4113.75 -- near week opener of 4146.25.

- Earnings cycle past the halfway mark, resumes Monday w/ Duke Energy (DUK), Tyson (TSN) before the open, Trex (TREX), Int Flavor/Fragrances (IFF), Cargurus (CARG) after the close.

- SPX leading/lagging sectors: Energy sector extends earlier gains (+2.91%) O&G consumables outpacing energy and equipment serving names. Utilities sector follows (+0.81%). Laggers: Materials sector holding near lows (-1.40%) w/ construction materials shares lagging; Communications sector (-1.30%).

- Meanwhile, Dow Industrials currently trades -97.15 points (-0.29%) at 32901.08, Nasdaq -173 points (-1.4%) at 12144.66.

- Dow Industrials Leaders/Laggers: United Health outperforms (UNH) +5.10 at 499.82, Chevron (CVX) +4.00 at 170.26. Laggers: Home Depot (HD) continues to sag -4.47 at 294.64, Nike (NKE) -3.62 at 115.01.

- RES 4: 4588.75 High Apr 5

- RES 3: 4509.00 High Apr 21 and a key short-term resistance

- RES 2: 4366.33 50-day EMA

- RES 1: 4303.50/4355.50 High Apr 26/28 / Low Apr 18

- PRICE: 4113.75 @ 1600ET May 6

- SUP 1: 4056.00 Low May 2 and the bear trigger

- SUP 2: 4029.25 High May 13 2021

- SUP 3: 4000.00 Psychological round number

- SUP 4: 3958.00 2.00 proj of the Mar 29 - Apr 18 - 21 price swing

COMMODITIES: Solid Weekly Gains For Oil, Putin Address Monday

- Oil sits circa 1.25% higher on the day for weekly gains of 2.5% (Brent) and 4.5% (WTI) as the EU moves closer to a stricter ban of Russian oil and the US looks to replenish its emergency reserves following the SPR release.

- WTI is +1.3% at $109.65 having earlier stopped just shy of resistance at yesterday’s high of $113.51, with a second resistance level shortly after that at $113.90 (76.4% of Mar 7 -15 downleg).

- The most active strikes today in CLM2 have been $100/bbl puts.

- Brent is +1.2% at $112.28, again drawing close to $114 (May 5 high) after which it would open a bull trigger at $115.76.

- Gold is +0.3% at $1883.15 but still down -0.7% on the week as long-end Treasuries trade above 3% and compete for safe haven demand. It’s the third straight weekly drop although Putin’s expected address on Monday could trigger renewed geopolitical tension demand.

- Technicals are unchanged from yesterday, with resistance is eyed at the 20-day EMA of $1910.4 whilst support is seen at the $1850.5 (May 3 low).

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/05/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Services PMI |

| 09/05/2022 | 0645/0845 | * |  | FR | Current Account |

| 09/05/2022 | 0645/0845 | * | | FR | Foreign Trade |

| 09/05/2022 | 1230/0830 | * |  | CA | Building Permits |

| 09/05/2022 | 1300/1400 |  | UK | BOE Saunders Speaks at Resolution Foundation Event | |

| 09/05/2022 | 1400/1000 | ** |  | US | Wholesale Trade |

| 09/05/2022 | 1500/1100 | ** | | US | NY Fed survey of consumer expectations |

| 09/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 09/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.