Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US Tsys: Finishing Near Lows

Tsys drifting near second half lows after the bell, 30YY at 3.2381% after tapping 3.2661% high earlier, last seen July 10. No obvious headline driver for continued weakness since rates extended session lows around 1000ET.

- Volume picked up in second half as Sep/Dec Tsy futures rolling picks up ahead the Aug 31 First Notice date (Dec takes lead.

- Coming into the session, however, Tsys tracked overnight price action in EGBs, as Tsys scaled off overnight highs (30YY tapped 3.1828% low) yield curves flatter with short end underperformed, 2s10s slipped to 33.136 inverted low currently at -29.492 (-3.112).

- Domino effect from soaring European energy prices (gas appr 10% higher, coal +5.1%) coupled with ongoing Russia/Ukraine war effect on gas prices and China growth slow-down is weighed on Euro, Sterling and short end EGBs on prospect of higher rates to contain inflation.

- Technicals for TYU2 currently trading 117-25 (-10.5), Treasuries maintain a softer tone and the contract is trading at its recent lows. 118-05, 50.0% of the Jun 14 - Aug 2 bull cycle, has been cleared and this signals scope for an extension towards 117-14+ next, the Jul 21 low. Price has recently cleared a trendline support drawn from the Jun 14 low and this reinforces the current bearish theme. Initial firm resistance is at 119-31, the Aug 15 high.

- Muted midday trade w/ focus on this week's annual Jackson Hole Economic Symposium: Reassessing Constraints on the Economy and Policy on Friday, August 26 as Chairman Powell discusses the Fed's economic outlook at 1000ET (0800 local), text is expected but no Q&A.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00400 to 2.31714% (+0.00628 total last wk)

- 1M +0.04072 to 2.42743% (-0.00529 total last wk)

- 3M +0.02200 to 2.97971% (+0.03614 total last wk) * / **

- 6M +0.01800 to 3.56557% (+0.03828 total last wk)

- 12M +0.01628 to 4.03214% (+0.05686 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 2.98400% on 8/18/22

- Daily Effective Fed Funds Rate: 2.33% volume: $94B

- Daily Overnight Bank Funding Rate: 2.32% volume: $289B

- Secured Overnight Financing Rate (SOFR): 2.28%, $960B

- Broad General Collateral Rate (BGCR): 2.26%, $393B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $383B

- (rate, volume levels reflect prior session)

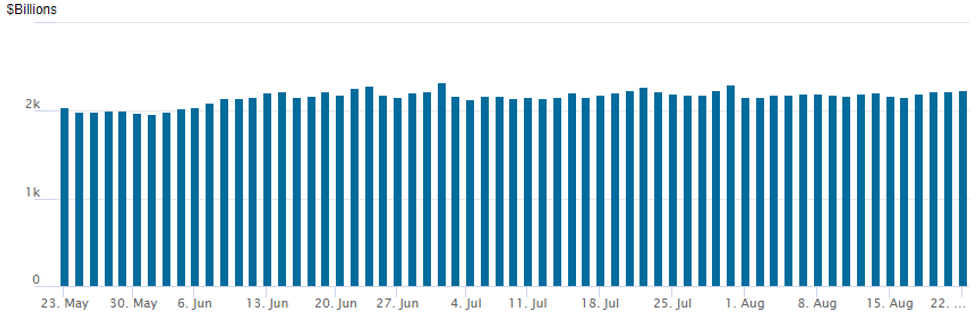

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage inches higher to $2,235.665B w/ 100 counterparties vs. $2,221.680B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Notable pick-up in Treasury option put volume Monday, albeit September expiry's tied to squaring ahead of this Friday's option expiration. Downside put buying picked up as underlying futures price in higher chances of rate hikes partially tied to Europe's inflation linked energy price surge.Highlight trade included Block buys of 15,000 each TYX 115 puts, 32 vs. 118-04/0.21% and TYV 116 puts, 28 vs. 118-03.5/0.24%, while paper bought +15,000 TYX 116/117 put spds, 19-20.

- SOFR Options:

- 5,000 SFRZ2 95.25 puts

- +10,000 SFRZ2 95.87/96.00 put spds, 2.5 ref 96.405

- +3,000 Green Dec SOFR 96.00/96.50/97.00 put flys, 7.5

- -1,000 SFRV2 96.75 calls, 6.0 ref 96.41

- Eurodollar Options:

- 4,000 Oct 95.75/96.00 put spds

- 1,200 Oct 95.50/95.75/96.00 put trees

- 1,300 short Dec 97.75/98.25 call spds

- Treasury Options: (Sep options expire Friday)

- 9,000 TYU 118.5/119.25 1x2 call spds, 3

- Block, +15,000 TYX 115 puts, 32 vs. 118-04/0.21%

- Block, +15,000 TYV 116 puts, 28 vs. 118-03.5/0.24%

- 5,000 FVV 113 calls

- +15,000 TYX 116/117 put spds, 19-20

- 4,000 TYU 116/117 put spds ref 118-02.5

- 2,150 FVV 113.5/115 call spds

- -5,000 FVV 113 calls, 20 ref 111-24

- +10,000 TYU 117.25/117.5/118 broken put flys, 8 ref 118-04 to -05

- Update, over 6,000 USV 130/134 put spds, 29-39

- +5,000 TYU 117.5 puts, 14-15

- 2,000 TYU 118 straddles, 58

- 3,000 TYU 117/117.5 put spds, 4

- 2,000 TYU 115.5 puts, 1

EGBs-GILTS CASH CLOSE: Selling Resumes On Energy Concerns

Bunds and Gilts picked up Monday where they left off last week: selling off, with an early rally reversing in the afternoon.

- There was relatively more market attention paid to FX (with EURUSD crashing through parity) and equities as European energy/power prices soared anew, heightening economic concerns.

- Gilts underperformed; UK short end weakness picked up later in the session as DMO announced a possible 2 or 3Y tender operation Thursday - 2Y yields hit a fresh post-2008 high.

- Periphery spreads widened amid the broader risk-off move; Italy underperformed, with the spread to Bunds at a fresh post-July high.

- While the Fed's weekend Jackson Hole event is the week's focus, lots of attention Tuesday on Eurozone, UK, and US PMI data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 7.1bps at 0.895%, 5-Yr is up 7.9bps at 1.121%, 10-Yr is up 7.6bps at 1.306%, and 30-Yr is up 4.7bps at 1.451%.

- UK: The 2-Yr yield is up 10.5bps at 2.63%, 5-Yr is up 10.5bps at 2.381%, 10-Yr is up 10.3bps at 2.514%, and 30-Yr is up 12.5bps at 2.839%.

- Italian BTP spread up 5.7bps at 232.7bps / Greek up 3.2bps at 250.3bps

EGB Options: Mostly Downside

- OEV2 123/122ps sold at 16.5 in 5k

- OEV2 124.50/123.00ps vs 127c, bought the ps for flat in 4k

- RXV2 145.5/144/143p fly, bought for 14.5 in 2.5k, total 5k done

- DUU2 109.80/109.60ps sold at 16 in 28k

- ERU2 99.125/98.875ps, sold at 2.5 in 5k

- ERU2 99.125/99.00 put spread bought for 2.5 in 16k. Note: 26k bought all day between 2 / 2.5

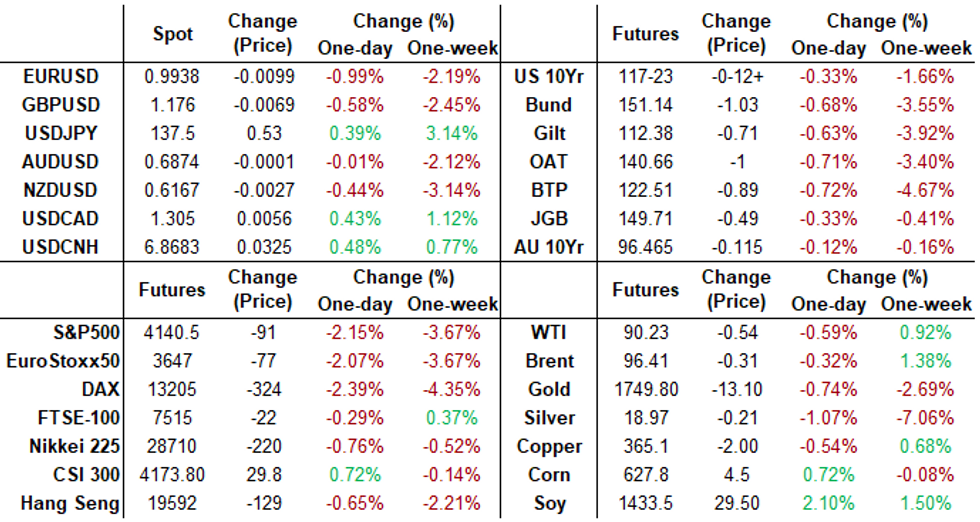

FOREX: EURUSD Sinks To Fresh Cycle Low Below 0.9950

- EURUSD (-1.03%) has come under further pressure on Monday as weakness across equity markets and higher core yields strengthen the renewed bullish momentum for the greenback seen over the past two weeks. The pair is now trading comfortably back below the psychologically significant parity mark and has sunk to a fresh cycle low of 0.9926 as of writing.

- The European energy crisis and ongoing fears regarding the growth outlook continue to act as strong fundamental headwinds for the single currency.

- Furthermore, the technical bear trigger at 0.9952 has been breached. The next notable support resides at 0.9883, the 1.764 projection of the Jun 9 - 15 - 27 price swing while further out, scope is seen for a move towards the channel base at 0.9734.

- The dollar index has risen 0.8% on Monday, extending above the 1.0900 mark and narrowing the gap with the July highs at 1.0929. Most G10 currencies have also fallen victim to the greenback rally, with USDCNH notably rising 0.5% on the back of China’s reference lending rates being lowered. The PBOC action prompted a much stronger showing from Aussie, which spent the majority of Monday in positive territory and despite giving up these gains, remains a relative outperformer with AUDUSD close to unchanged for the session at 0.6870.

- USDJPY looks set to extend its winning streak to five sessions. This comes despite a slightly weaker session overnight for the pair before the overall USD bid, sparked a 100-pip bounce to 137.65 highs. The nearest objective on the topside is 137.96, the Jul 22 high.

- Tuesday’s focus will be on the European flash PMI’s scheduled for the early European session. The market’s attention then turns to Jackson Hole and associated commentary from Fed Chair Powell at the end of the week.

Late Equity Roundup, Rout Deepens

Stock indexes continued to extend lows in late trade, prospect of higher rates tied to EU energy price surge weighing on stocks (Consumer Discretionary, Communication Services and IT underperforming) and short FI markets Monday. Currently, SPX eminis trade -96 (-2.27%) at 4135.25; DJIA -680.97 (-2.02%) at 33024.2; Nasdaq -332.9 (-2.6%) at 12371.8.

- Equity earnings cycle nearly complete, still some notable announcements next week: Nvidia (NVDA) late Wednesday $508 est, Dell late Thursday $1.636 est.

- SPX leading/lagging sectors: Energy sector mildly weaker (-055%) buoyed by energy/technology companies Diamondback Energy (FANG) +0.41%, Marathon (MRO) +0.37%, Baker Hughes (BKR) +0.44%; followed by Consumer Staples (-1.22), Utilites (-1.47) and Health Care follow (-1.64%). Laggers: As noted, Consumer Discretionary (-2.89), Consumer Services (-2.84%) and Information Technology -2.88%

- Dow Industrials Leaders/Laggers: Procter Gamble (PG) -$0.19 at 149.54, Verizon (VZ) -0.32 at 44.10, Dow -0.93 at 54.56. Laggers: Microsoft (MSFT) -8.42 at 277.69, Salesforce (CRM) -7.32 at 176.48, Home Depot (HD) -7.98 at 313.34.

E-MINI S&P (U2): Corrective Pullback

- RES 4: 4419.15 2.236 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4400.00 Round number resistance

- RES 2: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 1: 4288.00/4327.50 High Aug 19 /16 and the bull trigger

- PRICE: 4160.00 @ 1300ET Aug 22

- SUP 1: 4164.93 20-day EMA

- SUP 2: 4078.40 50-day EMA

- SUP 3: 4000.00 Round number support

- SUP 4: 3913.25 Low Jul 26 and a key support

The S&P E-Minis outlook remains bullish, however, a corrective cycle suggests scope for a pullback near-term. This will allow an overbought reading in momentum studies to unwind - attention is on the 20-day EMA at 4164.93. A breach of this EMA would signal scope for a deeper pullback, potentially exposing the 50-day EMA, at 4078.40. Key resistance and the bull trigger is at 4327.50, the Aug 16 high.

COMMODITIES: Oil Swings On Mixed Demand/Supply Forces, Gold Slides Lower

- Crude oil has seen a very mixed day, ultimately only down slightly, sliding on China growth fears plus potentially the hope of the Iran JCPOA deal and the eventual release of Iranian supply, before rebounding sharply as Saudi Arabia hinted at further OPEC+ action in response to futures volatility.

- Most recently on Iranian deal consideration, the US State Dept’s Ned Price says the US is encouraged by Iran dropping some “non-starter” demands, appearing to include the lifting of the terrorist label, but with comments that the US is still “engaging with” EU partners and not planning to take one day longer than needed to response to the EU, it doesn’t seem like a decision is imminent.

- WTI is -0.6% at $90.23 having touched a session low of $86.60, which in a doubling down on the bearish outlook came close to testing support at $85.73 (Aug 16 low).

- Brent is -0.2% at $96.58 off a session low of $92.42 that moved closer to the bear trigger at $91.22 (Jul 14 low).

- Gold is -0.55% at $1737.45 in a continuation of last week’s slide on USD strength and surging Treasury yields. A bear cycle is firmly in play having fleetingly cleared support at $1729.5 (61.8% retrace of Jul 21 – Aug 10 climb) after which sits $1711.7 (Jul 27 low).

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/08/2022 | 0030/0930 | ** |  | JP | IHS Markit Flash Japan PMI |

| 23/08/2022 | 0715/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 23/08/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 23/08/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 23/08/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 23/08/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 23/08/2022 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 23/08/2022 | 0800/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 23/08/2022 | 0830/0930 | *** |  | UK | IHS Markit Manufacturing PMI (flash) |

| 23/08/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 23/08/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 23/08/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 23/08/2022 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 23/08/2022 | 1100/1300 | | EU | ECB Panetta at ECB Policy Panel at EEA Annual Congress | |

| 23/08/2022 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 23/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 23/08/2022 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 23/08/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 23/08/2022 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 23/08/2022 | 1400/1000 | *** | | US | New Home Sales |

| 23/08/2022 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 23/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/08/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.