Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: FED RAISES RATES 25BPS TO 5%-5.25% RANGE; VOTE 11-0

- MNI FOMC: ECONOMY GREW MODESTLY IN Q1, JOB GAINS ROBUST

- MNI FOMC: BANKING SYSTEM IS SOUND, RESILIENT

- MNI FOMC: EXTENT OF CREDIT EFFECTS REMAINS UNCERTAIN

- MNI: ADP Sees Surprising Broad-Based Strength

- MNI US-CHINA: Schumer Announces Framework For Bipartisan China Bill

- MNI US: Yellen: Continued Fallout From War In Ukraine Focus Of G7 Fin Mins Meeting

- YELLEN TO GO TO JAPAN MAY 11-13 FOR G-7 FINANCE MINISTERS MTG, Bbg

Key Links:MNI: Fed Raises Rates To Highest In 16 Years, More Possible / MNI: FOMC May Statement Comparison / MNI: Rough Transcript of Powell's May 3 Press Conference / MNI INTERVIEW: Services Peaking As Fed Hikes Gain Traction-ISM / MNI: U.S. Treasury Expects To Begin Buybacks In 2024

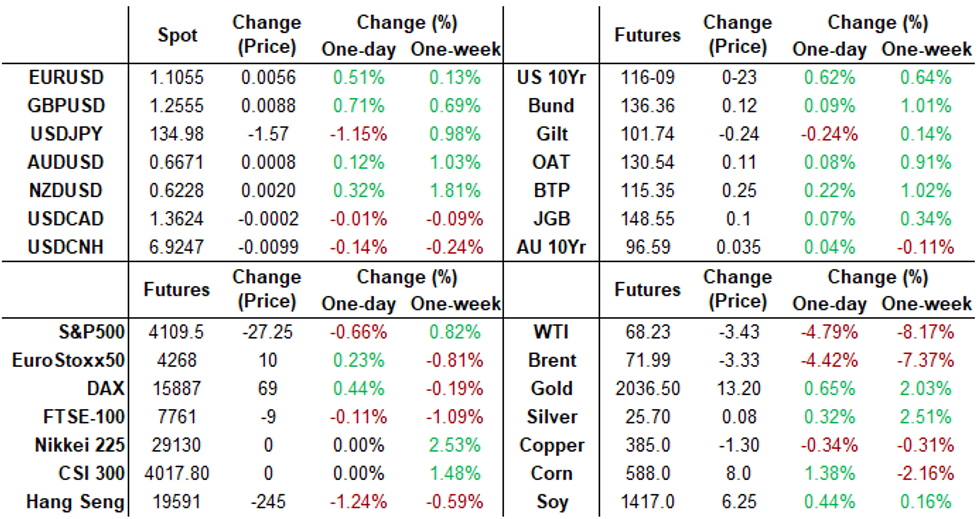

US TSYS: Yields Recede, Fed Opens Door to June Pause

- Wednesday's session remained volatile as Treasury futures extended highs after the FOMC delivered an expected 25bp rate hike to 5.0-5.25% range, support driven by the the Fed opening the door to a pause at the next meeting on June 14.

- The Fed rate path slipped lower after Chairman Powell's press conference, the June meeting dips 2bps to 5.08% but is still +1bps since the announcement.

- Assuming an effective rate of 5.08%, it largely marks a perceived end to the tightening cycle, with today’s hike priced to be unwound with Sep at -27ps to 4.81% (now -1bp post-decision having been +3bp in the presser). December cumulative at 74bp of cuts to 4.35% (now -1.5bp post-decision having been ~4.42%.

- Early Data driven volatility: Treasury futures pared gains after higher than expected ADP employment gain of +296k (+148k est). Little reaction to a minimal downward revision for the final April S&P Global US Service PMI. Rates extended highs but drew fast selling after ISM Service index data showed ongoing volatile new orders.

- Focus now on Friday's headline employment data for April, current mean estimate at +175k vs. 236k prior. Goldman Sachs raised their nonfarm payroll growth forecast by 25k to 250k after this morning's ADP and consistent with evidence from other Big Data sources.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00552 to 5.04042 (+.05473 total last wk)

- 3M -0.05194 to 5.05947 (-.01625 total last wk)

- 6M -0.09477 to 5.02694 (-.07071 total last wk)

- 12M -0.13436 to 4.75162 (-.14781 total last wk)

- O/N -0.00400 to 4.81086%

- 1M -0.01229 to 5.08157%

- 3M -0.01000 to 5.32629% */**

- 6M -0.03843 to 5.39443%

- 12M -0.13572 to 5.29957%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.33269% on 5/2/23

- Daily Effective Fed Funds Rate: 4.83% volume: $118B

- Daily Overnight Bank Funding Rate: 4.82% volume: $273B

- Secured Overnight Financing Rate (SOFR): 4.81%, $1.537T

- Broad General Collateral Rate (BGCR): 4.78%, $565B

- Tri-Party General Collateral Rate (TGCR): 4.78%, $556B

- (rate, volume levels reflect prior session)

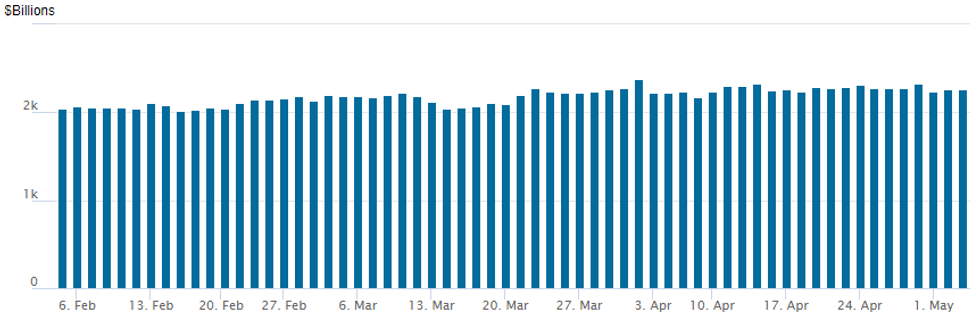

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage slips back to $2,258.222B w/ 102 counterparties, compares to prior $2,267.130B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- 5,000 SFRK3 94.81 puts, total volume over 23k

- 12,500 SFRZ 94.87/95.12/95.37/95.50 put condors ref 95.74

- Block, 20,000 SFRU3 94.68/95.00/95.50 broken put flys, 23.25 on splits

- Block, 5,000 SFRK3 94.62/94.75/94.87 put flys 1.5 ref 94.97

- Block, 5,000 SFRM3 95.31/95.43/95.56 call flys, .25 ref 94.97

- Block, 6,000 SFRN3 94.81/94.93/95.06 put flys, 2.0 ref 95.27

- Block/screen +20,000 SFRK3 94.75 puts, 1.0 ref 94.965

- 2,000 OQU3 95.25/96.25/96.75 broken put fly on 1x3x2 ratio ref 96.94

- 4,500 SFRM 95.06 puts, ref 94.975

- Block, 3,880 SFRM3 94.87/94.93 call spds 3.5 vs. 94.955/0.10%

- Block, 2,500 SFRM3 95.12/95.25 call spds, 1.5 ref 94.975

- Block, 3,000 SFRM3 95.12/95.37 call spds, 2.5 ref 94.98

- 2,000 SFRK3 95.12/95.31/95.37 call trees ref 94.97

- Blocks, 7,900 SFRK3 94.68/94.81/94.93 put flys, 2.75 ref 94.98

- 3,000 SFRU3 95.50/95.56/95.62/95.68 call condors, ref 95.28

- Block, 2,500 SFRM3 94.62/94.75/94.87 put flys, 1.25 ref 94.995

- Block, 5,000 SFRZ3 96.00/96.50/97.00/97.50 call condors, 5.5 ref 95.705

- 2,000 SFRK3 95.00/95.37 call spds, ref 95.00

- 8,000 SFRK3 94.81/94.87 put spds ref 94.985 to -.995

- 1,000 SFRM3 94.37/94.56 1x2 call spds, ref 94.965

- 4,000 SFRM3 94.68/94.75/94.81/94.87 put condors, ref 94.97

- Treasury Options:

- another 10,000 TYM3 114 puts, 16 ref 115-26.5, total volume over 34,000

- 7,000 FVM3 111/112 call spds, 17.5 ref 110-09 to -08.75

- Block, 10,000 TYN3 112.5 puts, 13 ref 116-00

- 5,000 FVM 109.25/111.25 strangles, ref 110-07.75

- over 6,400 FVM3 111 calls, 26.5 ref 110-10.25

- 4,000 TYM3 116.5 calls, 42 ref 115-22.5

EGBs-GILTS CASH CLOSE: Peripheries Impress Pre-ECB

Gilts and Bunds traded mixed Wednesday, with yields climbing from morning lows as the post-close Fed decision and Thursday's ECB came into sight.

- The German curve twist flattened, while the UK saw a mostly parallel shift with yields up 3bp apart from 5Yrs which were up just 2bp.

- Periphery EGBs impressed, with 10Y Italy and Greek spreads respectively down 4bp and 9bp vs Bunds. Sharp BTP spread tightening into the cash close was noteworthy, ahead of the ECB decision Thursday.

- ECB and BoE hike pricing closed on firmer footing, up 3.7bp to 3.72% and 1.6bp to 4.93%, respectively. 25bp hikes are seen as near-locks for May.

- In the ECB's case, a 50bp raise tomorrow has about 15-20% probability attached. Our preview for Thursday's highlight - the ECB decision - is here.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at 2.641%, 5-Yr is unchanged at 2.245%, 10-Yr is down 1.1bps at 2.247%, and 30-Yr is down 0.9bps at 2.371%.

- UK: The 2-Yr yield is up 3.1bps at 3.768%, 5-Yr is up 1.8bps at 3.569%, 10-Yr is up 2.7bps at 3.696%, and 30-Yr is up 3.3bps at 4.095%.

- Italian BTP spread down 4.4bps at 187.1bps / Greek down 8.9bps at 184.7bps

EGB Options: Busy In Rate Plays Pre-ECB

Wednesday's Europe rates / bond options flow included:

- RXM3 133/130ps sold at 24 in 2k

- RXM 133/131ps sold at 20 in 2k

- OEM3 116.50/115.50ps sold at 10.5 in 1k

- ERK3 96.25/96.00ps, bought for 1.5 in 3k.

- ERK3 96.25/96.00ps 1x2, sold at 1 in 2.5k

- ERM3 96.50/96.75/97.00/97.25 call condor bought for 3.75 in 5k

- ERU3 96.125/96.00/95.875/95.625 'broken' put condor bought for 1 in 10k

- 2NM3 96.50/97.00 call spread bought for 4.75 in 4k (Green June, underlying SFIM5)

FOREX: USD Index Weakens 0.6%, Fed Less Certain On Future Tightening

- The USD index weakened ahead of the FOMC rate decision on Wednesday and received another jolt lower as the Fed statement signalled less certainty on future tightening of policy. Despite leaving the door open to more increases, the Fed’s language affirms a meeting-by-meeting approach.

- Despite the initial blip lower which stretched the DXY’s decline to around 0.85%, the index pared those extended losses as the press conference approached. Approaching the APAC crossover, the USD index sits with around 0.6% losses.

- USDJPY traded as low as 134.84 but quickly traded back to levels around 135.50 throughout the press conference. The pair has slipped lower in most recent trade confirming the Japanese Yen as the best performer in G10 on Wednesday. The move lower for USDJPY is a correction following the steep rally witnessed following the Bank of Japan last week. Of note, USDJPY traded within 14 pips of the 2023 highs (137.91) on Tuesday which remains the key resistance for the pair.

- In similar vein, the Swiss Franc also shone, as growth concerns remain the key driver, with bank stability still a background concern, keeping major equity indices at depressed levels.

- CAD trades broadly unchanged on the session, once again underperforming amid the ongoing rout for oil futures where Front-month WTI receded another 4.5%, briefly printing below the $68 mark.

- On Thursday, markets turn their focus to the ECB, who is set to hike its key policy rates by 25bp on May 4, with latest inflation and banking sector data diminishing the case for 50bp.

FX: Expiries for May04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0940(E3.0bln), $1.1000(E1.3bln), $1.1075(E1.1bln), $1.1100(E1.2bln)

- USD/CNY: Cny7.00($1.7bln)

Stocks Were Extending Lows As Powell Discussed Bank Supervision

- Support for stocks waned as Chairman Powell discussed the bank's supervisory role. While early March bank failures "have now all been resolved and all depositors have been protected" Powell said the "resolution and sale of First Republic is an important step toward drawing a line under that period of severe stress."

- Stocks have since bounced off late session lows: S&P E-Mini Future down 6.25 points (-0.15%) at 4130.25; Nasdaq up 19.1 points (0.2%) at 12098.18 while DJIA lags, down 117.39 points (-0.35%) at 33560.42.

- Focus turns to quarterly earnings after the close, salient stocks include: Allstate, Equinix, QUALCOMM Inc, Cognizant Technology, Williams Cos, Albemarle Corp, MetLife Inc, Zillow Group Inc, Marathon Oil Corp, Ingersoll Rand Inc Etsy Inc, APA Corp.

E-MINI S&P TECHS: (M3) Pullback Considered Corrective

- RES 4: 4288.00 High Aug 19 2022

- RES 3: 4244.00 High Feb 2 and a medium-term bull trigger

- RES 2: 4223.00 High Feb 14

- RES 1: 4206.25 High May 1

- PRICE: 4112.00 @ 1545 ET May 3

- SUP 1: 4098.34/4068.75 50-day EMA / Low Apr 26

- SUP 2: 4061.11 38.2% retracement of the Mar 13 - Apr 18 bull leg

- SUP 3: 4052.50 Low Mar 30

- SUP 4: 4018.75 50.0% retracement of the Mar 13 - Apr 18 bull leg

S&P E-minis traded lower Tuesday and the contract breached the 20-day EMA. The move lower appears to be a correction - for now. Trend conditions remain bullish with moving average studies in a bull-mode set-up. The focus is on 4206.25, the May high and bull trigger. A break would confirm a resumption of the uptrend and open 4223.00, the Feb 14 high. Initial support to watch is 4098.34, the 50-day EMA.

COMMODITIES: Crude Oil Near Second 5% Slide But Gold Spurred By Weaker USD

- Crude oil has slumped further today, with WTI currently -4.7% after yesterday’s >5% decline, attributed to further demand concerns and with an additional rolling over back closer to session lows after the FOMC went through with a mostly priced 25bp hike.

- OPEC+ will monitor the situation on the oil market according to Russia Deputy PM Novak based on Tass reports, with it necessary to understand the reasons for the price drop and whether it may prove temporary. Further cut commitments by Russia will be drawn into question by the market based on its oil exports remaining high despite claims of 500 kbpd cuts.

- WTI is -4.7% at $68.32, having pushed through the round $70, further support at $69.02 (76.4% retrace of Mar 20 – Apr 12 rally) and coming close to $67.02 (Mar 24 low).

- Brent is -4.3% $72.05, pushing through support at $74.06 (76.4% reatrce of Mar 20 – Apr 12 bul run) and $72.34 (Mar 24 low), opening a key support at $70.10 (Mar 20 low).

- Gold is +0.45% at $2025.77, supported by the DXY slipping through the day. The yellow metal has pushed through resistance at $2019.4 (May 2 high) and briefly spiking to $2035.95 on FOMC-related volatility. The bull trigger remains at $2048.7 (Apr 13 high).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/05/2023 | 0130/1130 | ** |  | AU | Trade Balance |

| 04/05/2023 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 04/05/2023 | 0715/0915 | ** |  | ES | S&P Global Services PMI (f) |

| 04/05/2023 | 0745/0945 | ** |  | IT | S&P Global Services PMI (f) |

| 04/05/2023 | 0750/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 04/05/2023 | 0755/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 04/05/2023 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 04/05/2023 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 04/05/2023 | 0830/0930 | ** |  | UK | BOE M4 |

| 04/05/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 04/05/2023 | 0830/0930 | ** | | UK | S&P Global Services PMI (Final) |

| 04/05/2023 | 0900/1100 | ** | | EU | PPI |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 04/05/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 04/05/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 04/05/2023 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 04/05/2023 | 1230/0830 | ** | | US | Trade Balance |

| 04/05/2023 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 04/05/2023 | 1245/1445 | | EU | ECB Post-Meeting Press Conference | |

| 04/05/2023 | 1400/1000 | * | | CA | Ivey PMI |

| 04/05/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 04/05/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 04/05/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 04/05/2023 | 1650/1250 | | CA | BOC Governor speech/press conference. |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.