Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

Key links: MNI BRIEF: US March Jobs Meet Expectations; Wage Growth Slows

US TSYS

US TSYS: MSNBC interview of former Fed Vice Chair Lael Brainard, currently director of the National Economic Council since February 21, 2023, comments on this morning's March employment data: "really nice report" with "lots of positives in jobs market".

- No market reaction, futures have quietly drifted back near initial post-data lows: USM3 at 133-04 (-31) vs. 132-31 low, 30Y yield at 3.5956% +.0450, TYM3 115-25.5 last (-24) vs. 115-23 low, 10Y yield 3.3775% +.0725.

- Yield curves near lows: 2s10s -7.092 at -60.304 vs. -60.568 low. Very light overall volumes ahead the early session close at 1100ET (Globex 15 minutes later), TYM3 under 320k at the moment.

- A 3-mth average of 345k and 6-mth average of 315k remains far stronger than long-term levels consistent with population growth, whilst in the household survey, employment roared back with 577k as it maintained recent volatility.

- That pushed the u/e rate down to 3.50% (cons 3.6) although as noted it didn’t take that much from 3.57% prior. This u/e rate is only marginally off January’s 3.43% in what was the lowest level since 1969.

- Impressively, this came despite the participation rate rising further to 62.6 (labour force increased another rapid 480k) for a new post-pandemic high (although still 0.5pts off pre-pandemic levels). Interestingly, it was led by non-prime cohorts returning whilst the prime-age participation rate consolidated last month’s increase pre-pandemic recent highs of 83.1%.

SHORT TERM RATES

US DOLLAR LIBOR: No settlements Friday and Monday due to London bank holiday, resume Tuesday. For reference, the levels below are from Thursday, April 6:

- O/N +0.00042 to 4.80971% (+0.00885/wk)

- 1M +0.01015 to 4.90029% (+0.04258/wk)

- 3M -0.01314 to 5.19786% (+0.00515/wk)*/**

- 6M -0.05471 to 5.23743% (-0.07557/wk)

- 12M -0.07386 to 5.12571% (-0.17958/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.22257% on 4/3/23

- Daily Effective Fed Funds Rate: 4.83% volume: $98B

- Daily Overnight Bank Funding Rate: 4.83% volume: $122B

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- Block -10,000 SFRM3 95.25/95.50 call spds, 2.5 to 3.25 vs.

- +10,000 SFRM3 94.93/95.00 put spds, 2.5 to 3.0

- 1,000 SFRK3 95.12/95.18/95.25/95.31 call condors ref 95.165

- 1,500 SFRJ3 95.18/95.25/95.31/95.43 call condors ref 95.17

- Treasury Options:

- 2,000 TYK3 117/118.75/119.5 broken call trees on 2x1x1 ratio, 34 net ref 115-27

- 2,300 FVM3 107/108/109 put trees, 11 ref 110-05

- Block, 7,500 TYK3 114.5 calls vs. TYM 114 put calendar combo, 1-34 net vs. 116-13/0.80%

- +5,000 TYM3 112 puts, 13 ref 116-10.5

- 1,000 TYK3 118/120 call spds ref 116-16

- 2,100 FVK3 108.75 puts, 4.5 ref 110-19.5

- 1,250 FVK 112.5 calls, 11 ref 110-16.75

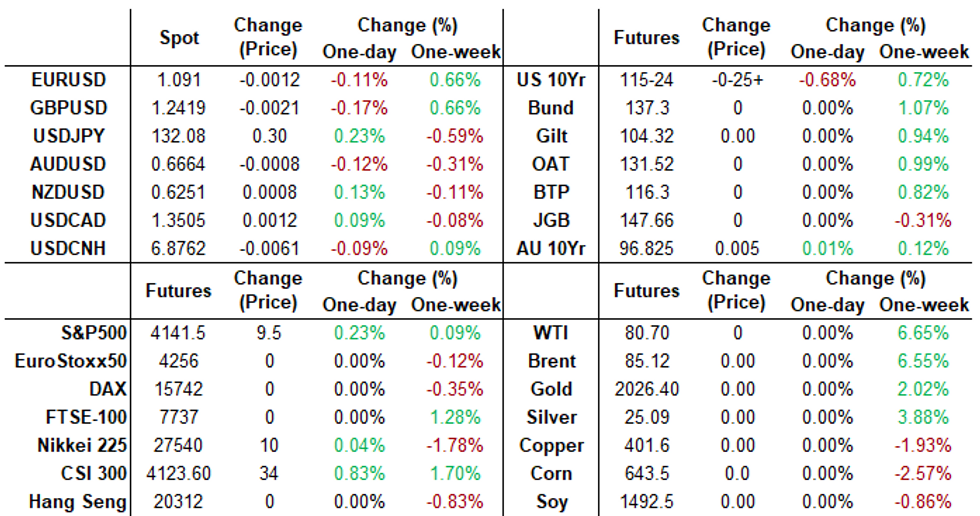

FOREX: EURUSD Sees Decent Retracement Of Payrolls Drop, USDJPY Holding Firmer

- EURUSD trading back at circa 1.09 having touched a low of 1.0877 and now 15 pips lower than before the payrolls release.

- It pushed higher having tested support at 1.0883 (Apr 4 low) for pre-JOLTS levels, and for now at least doesn’t appear to have steam to push lower to next open 1.0802 (20-day EMA).

- USDJPY meanwhile holds most of its climb, trading at 132.24 off a high of 132.38, still near resistance at the 20-day EMA of 132.55, a clear break of which could open some leeway to 133.77 (50% of Mar 8-24 bear leg) in what would be a departure from the recent trend needle pointing south.

- Elsewhere, only NZD maintains gains vs the greenback on the day at typing, although only just at +0.02% from +0.24% prior with NZDUSD trading 0.6247.

S&P Eminis Top of Range

Front month emini futures (ESM3) finished the abbreviated session near post data high of 4142.5 at 4141.50.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/04/2023 | - |  | EU | ECB Lagarde at IMF/World Bank Spring Meetings | |

| 10/04/2023 | 1400/1000 | ** |  | US | Wholesale Trade |

| 10/04/2023 | 2015/1615 | | US | New York Fed's John Williams | |

| 11/04/2023 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 11/04/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 11/04/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 11/04/2023 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 11/04/2023 | - | | EU | ECB Lagarde and Panetta in IMF/World Bank Spring Meetings | |

| 11/04/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 11/04/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 11/04/2023 | 1730/1330 | | US | Chicago Fed's Austan Goolsbee | |

| 11/04/2023 | 2200/1800 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok