Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI UN: Security Council To Meet Friday To Discuss Grain Deal

- MNI EU: Borrell: Russian Attacks On Odesa Will Cause World Shortage Of Grain

- MNI US-RUSSIA: Washington Announces Broad New Package Of Russia Sanctions

- RUSSIA IS NOT PREPARING TO ATTACK CIVILIAN SHIPS IN BLACK SEA DESPITE U.S. CLAIMS - RIA QUOTES RUSSIAN AMBASSADOR TO U.S

US TSYS: Rates Off Late Session Lows as Stocks Head South

- Treasury futures are weaker across the board after the bell, drifting off second half lows after the first block buy at 1324:02ET: +5,000 FVU3 107-06.25, buy through 107-06 post-time offer. As was the case in EGBs, session moves were largely flow driven, not headline related on the day.

- Futures opened and continued to extend lows after weekly claims came out lower than expected at 228k vs. 240k est., Philly Fed -13.5 vs. -10 est. Sporadic knee-jerk selling saw front month 10Y futures initially mark 112-09.5 low (-22.5) before bouncing to 112-14 amid moderate two-way trade.

- Trading desks reported heavy round of selling in 10s into midday: over 15,000 TYU3 extended session low to 112-00 (-1-00). Unexpected consequence, 2s10s curve bounced off the session inverted low of -105.083 (compares to appr 40-year lows tapped in early March and July of -110.89) to -98.802, up +3.185 on the day.

- Despite the late drift off lows, rate hike projections gain slightly: July running at 96% w/ implied rate of +24bp to 5.318%. September cumulative of +28.2bp at 5.360%, November cumulative of 34.2bp at 5.42%, and December cumulative of 28.8bp at 5.366%. Fed terminal holding at 5.42% in Nov'23.

- Dearth of economic data over the next two sessions, awaiting the latest FOMC policy announcement next Wednesday. July 26.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.02777 to 5.29134 (+.06140/wk)

- 3M +0.01205 to 5.34557 (+.03568/wk)

- 6M +0.01346 to 5.41260 (+.03706/wk)

- 12M +0.02340 to 5.30920 (+.05519/wk)

- Daily Effective Fed Funds Rate: 5.08% volume: $106B

- Daily Overnight Bank Funding Rate: 5.07% volume: $262B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.456T

- Broad General Collateral Rate (BGCR): 5.03%, $589B

- Tri-Party General Collateral Rate (TGCR): 5.03%, $581B

- (rate, volume levels reflect prior session)

FED Revers Repo Operation: New Lows

NY Federal Reserve/MNI

The latest operation recedes to $1,721.001B (lowest since early April May'22), w/ 100 counterparties, compared to $1,732.804B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Modest overnight summer volumes on better overall call trades segued to low delta put structures from midday on Thursday. Underlying futures weaker while rate hike projections gain slightly: July running at 96% w/ implied rate of +24bp to 5.318%. September cumulative of +28.2bp at 5.358%, November cumulative of 34.2bp at 5.42%, and December cumulative of 29.1bp at 5.368%. Fed terminal holding at 5.42% in Nov'23. Salient trade includes: Salient trade includes:

- SOFR Options:

- +5,000 SFRZ3 94.43/94.68 2x1 put spds, 4-4.5

- 1,500 SFRZ3 94.25/94.50/94.75/95.00 put condors ref 94.62

- 8,700 SFRH4 96.00/96.50/97.00/97.50 call condors

- +3,500 OQU3 95.37/95.75 2x1 put spds, 2.5 ref 95.67

- +5,000 SFRM4 93.75/94.50 2x1 put spds, 7.5 ref 95.25

- +3,000 SFRZ3/SFRH4 97.00/97.75 call spd spd, 2.0 net, March over

- 1,250 SFRZ3 95.00/95.25/95.87/96.12 call condors ref 94.645

- Block, 4,000 SFRZ3 94.75/95.00 call spds, 4.0 ref 94.655

- Block, 4,000 OQZ3 97.00/97.25 call spds, 4.0 ref 96.095

- Treasury Options:

- 1,300 FVV3 108/111.5 call spds,

- 1,000 TYU3 112.5/114.5/115.5 1x3x2 broken call flys, 18 ref 112-04.5

- 7,500 FVV3 109.5/110.75 call spds ref 108-05.5

- 1,000 FVU3 106/107/108 put flys, ref 107-09.25

- over 26,500 TYQ3 112 puts, 2 ref 112-18.5

- 6,000 FVU3 107/107.25 put spds 8 ref 107-15.5

- 5,000 FVQ3 108 calls, 1.5 ref 107-15.25

- 7,500 TYQ3 113.75 calls, 3 ref 112-18

- over 5,000 FVU 108.75 calls, 17.5 last

- 2,000 FVU3 107 puts 31 ref 107-16.25

- 2,100 TYU3 115 calls ref 112-20.5

- over 5,200 TYQ3 113 calls, 9-5

- over 5,000 TYQ3 113.25 calls, 5-2 ref 112-28

EGBs-GILTS CASH CLOSE: Yields Continue To Claw Back UK CPI Drop

European yields continued to rebound from Wednesday morning's UK CPI-inspired drop, with curve short-end/bellies underperforming Thursday.

- While there were no obvious catalysts to the selloff, a combination of solid Australian and US labour market data rekindled a hawkish central bank narrative, and UK and Bund yields were dragged higher through to the cash close.

- Gilts underperformed, with the UK curve bear flattening as BoE hike expectations bounced (terminal pricing +7bp), tipping 2Y yields just shy of the 5% handle. MNI's review of Wednesday's UK CPI data is here.

- German yields rose 5-6bp across the curve, with 10Y yields ending higher than Monday's close.

- All in all, German 10Y yields are 17bp up from Wednesday's low, UK just 13bp.

- Periphery spreads tightened, led by Italy - 10Y BTP again tested the 160bp mark to Bunds.

- Attention first thing Friday morning will be on UK retail sales data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.9bps at 3.123%, 5-Yr is up 5.6bps at 2.571%, 10-Yr is up 5.2bps at 2.49%, and 30-Yr is up 3.5bps at 2.504%.

- UK: The 2-Yr yield is up 8.4bps at 4.994%, 5-Yr is up 7.5bps at 4.385%, 10-Yr is up 6.2bps at 4.277%, and 30-Yr is up 3.5bps at 4.412%.

- Italian BTP spread down 2.4bps at 161.8bps / Spanish down 1.1bps at 99.7bps

EGB Options: Euribor Call Fly Buying Continues Thursday

Thursday's Europe rates / bond options flow included:

- ERZ3 96.25/96.375/96.50 call fly bought for 0.9 (synth) in 12k

- ERU4 96.25/96.75/97.25 call fly paper paid 9 on 10K

- 0RU3 96.50^ bought for 41.5 in 1k

- 2RU3 97.125 call sold at 15 in 1k (v 97.01)

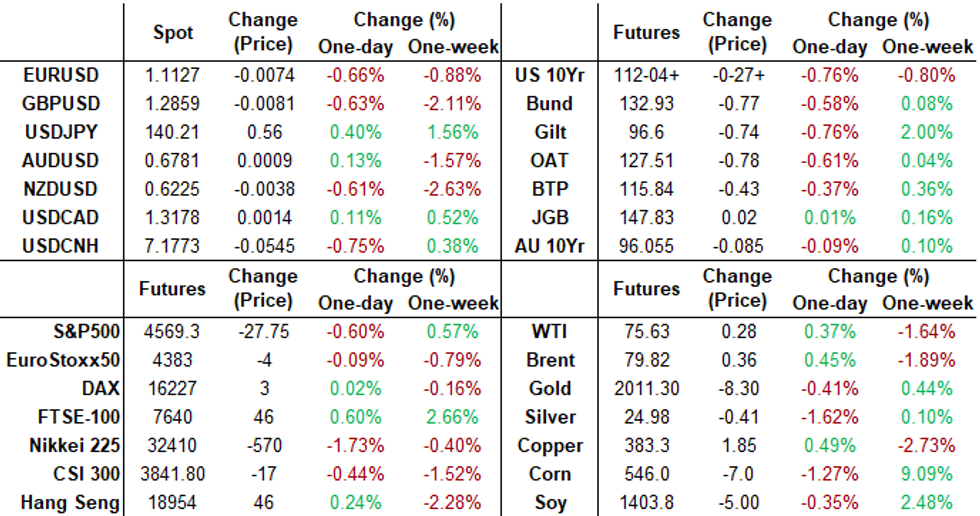

FOREX: Greenback Extends Recovery Amid Higher US Yields, CHF Underperforms

- After a modest uptick on Wednesday, the USD index has extended its recovery during today’s session amid a substantial move higher for US yields. Lower than expected jobless claims appeared to rekindle a hawkish central bank narrative, enhanced by the earlier strong jobs data in Australia bolstering the theme across global markets.

- USDCHF is the best performing currency pair on Thursday, having advanced 0.93% as we approach the APAC crossover. Yield differentials the biggest factor underpinning the recovery with USDJPY also retaking the 140.00 handle in the process.

- EURUSD and GBPUSD were seen grinding lower over the course of US trade, mirroring the adjustment of the broad USD index. For GBPUSD, the price action marks an extension of the prior day’s move following the softer-than-expected UK inflation prints. Markets are on watch for a potential reversal pattern - which gathered strength on the show below 1.2866 - the 50% retracement of the late June upleg. This opens potential for losses toward 1.2801 initially, before 1.2751, the July 10 low.

- Despite pulling back, the Australian dollar remains an outperformer in G10 following the solid June jobs report. Australia added 32.6k jobs across the month, doubling market expectations.

- Offsetting the firmer greenback narrative somewhat was USD/CNH, which sits 0.80% lower on the session. The redback benefitted from a much stronger-than-expected lean in the USD/CNY mid-point fixing. The PBoC also tweaked limits to allow companies to borrow more overseas, opening the door to the potential for an uptick in capital inflows, providing further support to the yuan.

- Japan National Core CPI y/y is the data highlight overnight before next week’s Bank of Japan meeting/decision. On Friday we will also see retail sales data for both the UK and Canada.

FX: Expiries for Jul21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1100(E551mln), $1.1150-60(E535mln), $1.1200-05(E783mln), $1.1220-30(E747mln), $1.1300(E675mln)

- USD/JPY: Y138.60($600mln), Y140.00($649mln), Y141.50($704mln)

- EUR/GBP: Gbp0.8600(E651mln)

- AUD/USD: $0.6700(A$862mln), $0.7400(A$1.1bln)

- AUD/NZD: N$1.0900(A$1.0bln)

- USD/CAD: C$1.3145-55($1.1bln), C$1.3300($732mln)

LATE EQUITIES: SPX Extends Losses, Courts Pause MSFT/Activision Merger Trial

- SPX Eminis and Nasdaq indexes extending session lows with DJIA still outperforming, but paring gains, apparently in a knee-jerk reaction to latest Microsoft/Activision merger headlines that the FTC will "pause it's merger trial, allowing settlement talks".

- Earlier in the week, Reuters reported "Microsoft Corp (MSFT.O) is in talks about an extension of its acquisition contract with video game maker Activision Blizzard (ATVI.O), which is set to expire on Tuesday, so the parties can overcome the remaining regulatory hurdles to their $69 billion deal."

- Currently, DJIA is up 199.09 points (0.57%) at 35260.18, S&P E-Mini Futures down 28.5 points (-0.62%) at 4568.75, Nasdaq down 271 points (-1.9%) at 14087.73.

- Laggers: Consumer Discretionary, Communication Services and Information Technology underperformed in the second half. Chip stocks are weaker, paring gains after rallying the last couple weeks on AI demand. Of note, Monolithic Power -7.35%, Enphase -5.0%, Applied Materials -4.95%, AMD -4.65%.

- Tesla weighs on Consumer Discretionary, -9.0% in late trade even after beating earnings and revenue ests late Wednesday: $0.91 versus estimate of $0.82. Revenues of $24.93B versus estimates of $24.48B.

- Leading gainers: Health Care, Utilities and Energy sectors outperformed in the second half. Pharmaceutical shares buoyed Health Care, J&J +5.75%, BMY +2.75%, LLY +2.15%. Oil and Gas shares driving Energy higher: Valero and Hess Energy up +2.2-2.1%.

- Reminder: earnings after today's close: Capital One, PPG and CSX.

E-MINI S&P TECHS: (U3) Bull Channel Top Cleared

- RES 4: 4739.50 High 13 Jan’22

- RES 3: 4661.90 3.0% 10-dma envelope

- RES 2: 4631.00 High 29 Mar’22

- RES 1: 4609.25 High Jul 20

- PRICE: 4569.50 @ 1455 ET Jul 20

- SUP 1: 4492.63 / 4368.50 20-day EMA / Low Jun 26 and a key support

- SUP 2: 4391.14 50-day EMA

- SUP 3: 4337.83 Bull channel base drawn from the Mar 13 low

- SUP 4: 4269.50 Low Jun 2

E-mini S&P sits slightly lower on the day, consolidating a solid rally this week and helping to alleviate the overbought conditions present in the most recent bout of strength. Prices have topped the bull channel drawn off the March 13th low at 4608.50, marking another positive shift for S/T momentum. This clears the way for a test of the March 29th 2022 high at 4631.00 and - ultimately - all time highs. Any corrective pullback would initially target the 20-day EMA at 4492.63 for support, however the Tuesday low of 4544.50 could also slow any decline.

COMMODITIES: Volatile Crude Oil And Surging Gold

- Crude oil has seen a volatile day, sliding through the European session on global growth fears and then weak US data (another weak regional Fed survey plus a small rise in initial claims) before recovering strongly.

- The rebound has been helped by an explosion at South Korea’s Ulsan refinery, a new record high for US gasoline, a pause in the slide in equities and US Energy Secretary Granholm telling the Senate that the US won’t be importing any oil from Iran or Venezuela.

- WTI is +2.4% at $112.20 having cleared support at the 20-day EMA of $106.5 but now moving nearer to $115.56 (May 17 high).

- Brent is +2.6% at $111.93, having cleared support at $107.79 (May 13 low) before retreating to eye $115.69 (May 17 high).

- Gold is +1.4% at $1841.63 on continued haven demand, accentuated by the slide in the US dollar. Bucking its recent vulnerable patch, it nears resistance at $1858.8 (May 12 high).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/07/2023 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 21/07/2023 | 0600/0700 | *** | | UK | Public Sector Finances |

| 21/07/2023 | 0600/0700 | *** | | UK | Retail Sales |

| 21/07/2023 | 0645/0845 | * |  | FR | Retail Sales |

| 21/07/2023 | 1230/0830 | ** |  | CA | Retail Trade |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.