Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- Mastercard SpendingPulse: U.S. Retail Sales Grew 7.6%, Business Wire

- China Reopens Borders to World in Removing Last Covid Curbs, Bbg

- Laid Off Tech Workers Quickly Find New Jobs, WSJ

US TSYS: Rates Hold Lower, Narrow Band

Early Tuesday risk sentiment after China said it will end quarantine requirements for inbound travelers in early January, gradually evaporated as Tsys continued to drift lower on very light volumes by the close (TYH3<585k), while equities reversed early gains, Dow shares outperformed mildly weaker SPX and Nasdaq shares ahead the FI close. Trade volumes will hopefully improve Wednesday as London returns from extended Christmas holiday.

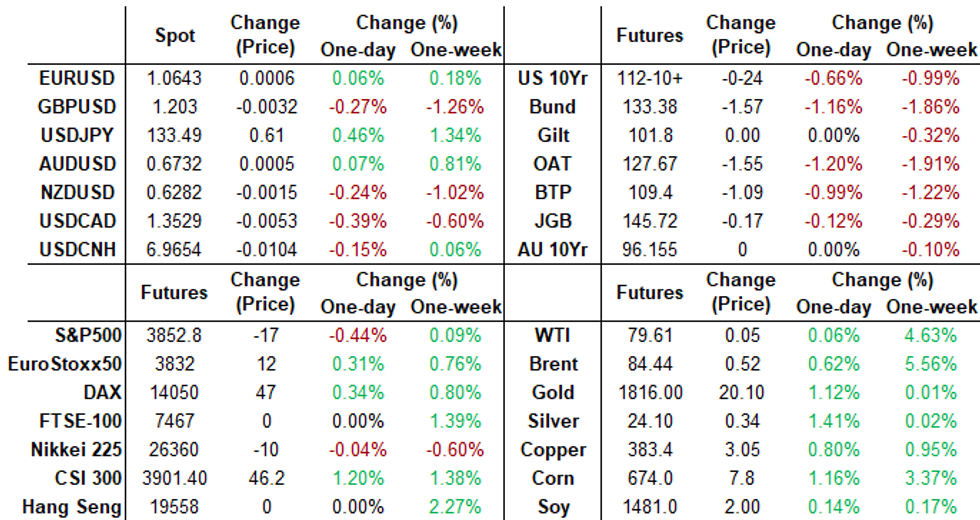

- Carry-over weakness w/ US$ index lowest levels in six months, extended losses from last week when data showed that US core PCE prices, the central bank’s preferred inflation gauge, fell to a four-month low of 4.7% YoY in Nov.

- Little react after $42B 2Y note auction (91282CGD7) stops through: 4.373% high yield vs. 4.390% WI; 2.71x bid-to-cover vs. 2.64x prior. Indirect take-up climbs to 62.22% vs. 56.98% last month, direct take-up 18.71% vs. 20.62%. primary dealer take-up 19.07% vs. 22.39%.

- Focus turns to Wed's data: Richmond Fed Mfg Index (-9, -10) and Pending Home Sales MoM (-4.6%, -1.2%); YoY (-36.7%, --) at 1000ET

- US Tsy auctions: $22B 2Y FRN Note auction re-open (91282CFS5) at 1130ET, $43B 5Y Note auction (91282 CGC9) at 1300ET

SHORT TERM RATES

US DOLLAR LIBOR: No new settlements, below as of Friday, December 16. Benchmark resumes Wednesday, December 27.

- O/N +0.00171 to 4.31671% (-0.00029/wk)

- 1M -0.00185 to 4.38686% (+0.03400/wk)

- 3M +0.00257 to 4.72643% (-0.01943/wk)*/**

- 6M +0.00457 to 5.15314% (-0.03372/wk)

- 12M +0.02800 to 5.44386% (-0.03500/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.77857% on 11/30/22

- Daily Effective Fed Funds Rate: 4.33% volume: $107B

- Daily Overnight Bank Funding Rate: 4.32% volume: $270B

- Secured Overnight Financing Rate (SOFR): 4.30%, $991B

- Broad General Collateral Rate (BGCR): 4.26%, $364B

- Tri-Party General Collateral Rate (TGCR): 4.26%, $352B

- (rate, volume levels reflect prior session)

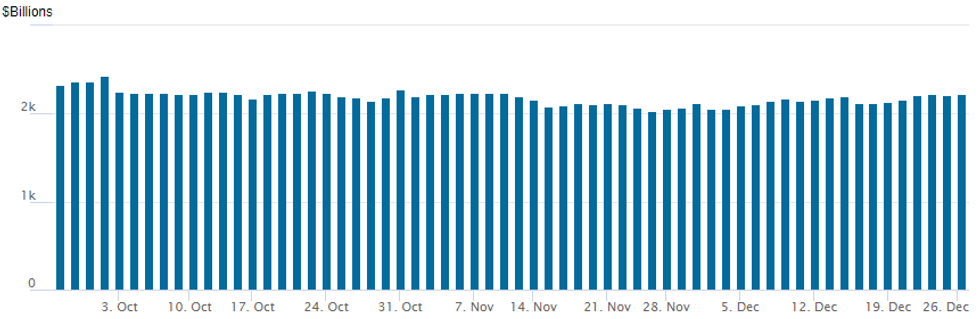

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,221.259B w/ 100 counterparties vs. $2,216.348B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- 2,000 SFRH3 95.25/95.37/95.50 call trees ref 95.065

- -25,000 2QH3 (Green Mar'23 SOFR) 97.37/97.62 call spds, 3.25 ref 96.74

- +10,000 SFRJ 94.75/95.00 put spds 2.5 over 95.50 calls vs. 95.08/036%

- +4,000 SFRH3 95.06/95.18/95.31 call flys, 2.5

- Eurodollar Options:

- -20,000 EDH3 95.25 conversions vs. +SFRH4 97.12 conversion vs.

- -20,000 EDH4 96.00 puts, 53.0 net cr on package

- 5,000 Jun 94.62/95.00 put spds, 17

- Treasury Options:

- +12,000 FVG 108/108.5 put spds, 17.5

- 3,000 wk5 TY 111.5/112 put spds, 4 ref 112-13.5

- 3,857 TYG 114/TYH 115.5 call spds 15 ref 112-18.5

- 2,000 USG 120/124 put spds, 61 ref 125-29

- 1,000 USG 117/120/124 2x3x1 put flys, 55 ref 125-20

- Block, 9,000 wk2 TY 110.5 puts, 10 vs. 112-25/0.14%

- 56,000 TYG 113.5/114.5 call spds 21 ref 112-26.5 to -18

- 2,500 TYG 111 puts, 20

- 1,100 FVG 108 straddles, 24 ref 108-10.25

Late Equity Roundup: Dow Industrials Outperform

Major indexes traded mixed late Tuesday, Dow shares outperformed mildly weaker SPX and Nasdaq shares ahead the FI close. Mining equipment maker Caterpillar and O&G refiner Chevron lead DJIA gainer: +11.19 (-0.03%) at 33194.05; SPX eminis currently trade -22.5 (-0.58%) at 3847.25; Nasdaq -152.9 (-1.5%) at 10345.63.

- Dow Industrials Leaders/Laggers: Caterpillar (CAT) +3.57 at 243.44, Chevron (CVX) +2.41 at 179.81, followed by United Health (UNH) +1.30 at 532.61. Laggers: Goldman Sachs (-3.13) at 342.38, Apple (AAPL) -2.15 at 129.71, Microsoft (MSFT) -2.05 at 236.68.

- SPX leading/lagging sectors: Energy sector leading (+0.95%) partially tied to firmer crude prices (WTI +0.55 at 80.11) w/ O&G refiners narrowly outpacing equipment and servicer stocks. Consumer Staples (+0.34%) followed by Industrials (+0.27%) lead by capital goods, particularly aerospace and defense (Northrop Grumman, NOC +1.25%).

- Laggers: Communication Services and and Consumer Discretionary both appr -1.25%, the latter weighed by auto makers in particular Tesla (-8.27%). Information Technology next up (-1.0%) with semiconductor makers underperforming.

COMMODITIES

- WTI Crude Oil (front-month) up $0.04 (0.05%) at $79.61

- Gold is up $14.75 (0.82%) at $1812.93

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/12/2022 | 1330/0830 | ** |  | US | Advance Trade, Advance Business Inventories |

| 27/12/2022 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 27/12/2022 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 27/12/2022 | 1530/1030 | ** | | US | Dallas Fed manufacturing survey |

| 27/12/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 27/12/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 27/12/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 27/12/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.