HIGHLIGHTS

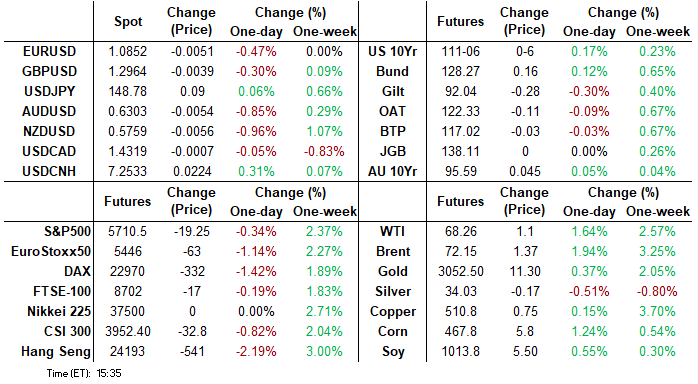

- Tsys opened higher, extended highs early Thursday, carry-over support from Wednesday's post-FOMC rally while initial European equity weakness spilled over to US stocks, contributing to early Thursday tone.

- Still bid after the close, Treasury futures scaled back from morning highs after Existing Home Sales comes out better than expected, Leading Index near in-line.

- Stocks retreated since posting session highs late Thursday morning as Information Technology and Consumer Staples stocks traded weaker.

MNI US TSYS: Firmer/Near Lows, Curves Manage to Bull Steepen off Lows

- Still bid after the bell, Treasury futures look to finish near late Thursday session lows. Rates reversed early morning support after much stronger than expected Existing Home Sales for February, rising to 4.26mln on a seasonally-adjusted annual basis from 4.09mln in January - versus expectations of a decline to 3.95mln.

- Prior to that, Initial jobless claims came in at 223k in the Mar 15 week - which is the reference period for March's nonfarm payrolls report - basically matching the 224k expected (221k prior was rev from 220k). Continuing claims registered 1,892k in the Mar 8 week, a touch softer vs the 1,887k expected though more than offset by a downward revision to the prior week.

- Treasury had extended overnight highs - carry-over support after Wednesday's post-FOMC rally, while weaker European equities spilled over to US stocks, contributing to the move. Brief dip in Tsys overnight as EGBs lagged core peers on incoming supply before the weaker equities spurred risk off bid.

- Curves managed to bull steepen off lows, 2s10s +1.335 at 27.559, 5s30s +1.532 at 54.364. Projected rate cuts through mid-2025 recede from this morning's highs (*) as follows: May'25 at -4.5bp (-5.8bp), Jun'25 at -20.1bp (-21.7bp), Jul'25 at -30.7bp (-31.5bp), Sep'25 -46.9bp (-48.3bp).

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00290 to 4.31919 (+0.00279/wk)

- 3M -0.00254 to 4.30284 (+0.00779/wk)

- 6M +0.00216 to 4.23523 (+0.03686/wk)

- 12M +0.00382 to 4.08889 (+0.07105/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (-0.02), volume: $2.376T

- Broad General Collateral Rate (BGCR): 4.28% (-0.02), volume: $943B

- Tri-Party General Collateral Rate (TCR): 4.28% (-0.02), volume: $920B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $106B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $285B

FED Reverse Repo Operation

RRP usage recedes slightly to $192.640B this afternoon from $193.378B Wednesday. Compares to $58.770B (lowest level since mid-April 2021) on February 14. The number of counterparties steady at 47.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported heavy volumes Thursday, mixed SOFR flow leaned towards downside puts through Dec 2025, Treasury options saw large positioning/position squaring ahead Friday's April expiration. Underlying futures bid but off morning highs after existing home sales surge, TYM5 trades 111-06 (+6) after climbing to 111-17.5 high earlier. Projected rate cuts through mid-2025 recede from this morning's highs (*) as follows: May'25 at -4.5bp (-5.8bp), Jun'25 at -20.1bp (-21.7bp), Jul'25 at -30.7bp (-31.5bp), Sep'25 -46.9bp (-48.3bp).

SOFR Options:

Block, +5,000 0QM5 96.62/96.87 call spds 2.5 over 95.87/96.12 put spds vs 96.485/0.28%

-5,000 0QZ5 96.25/96.75/97.25/97.75 call condors, 15.25 ref 96.52

+6,000 SFRM5 95.68/95.75/95.81 put trees, 2 ref 95.91

+10,000 SFRK5 95.68/95.75 put spds, 0.75 ref 95.91

+11,000 SFRZ5 95.12/96.00 put spds, 12.5-12.25 ref 96.345

+3,000 SFRZ5 95.50/95.75/96.00/96.25 put condors, 8.75 ref 96.355

+2,500 SFRZ5 95.68/95.87 put spds, 5.0 ref 96.36

+2,500 SFRM5 95.68/95.81 put spds, 4.25 ref 95.915

Block +5,000 0QN5 96.50/96.75 call spds, 9.5

+20,000 SFRZ5 95.62/96.00 put spds, 10.75 ref 96.35

+6,000 0QM 97.12/2QM5 97.37 call spds, 0.0/Green Sep over

6,900 SFRJ5 96.12/96.25 call spds ref 95.92 to -.925

+10,000 SFRZ5 95.00 puts, 1.5 ref 96.335

2,000 SFRU5 96.31/96.50/96.87/97.06 call condors vs. 95.68/95.81 put spds ref 96.16

2,000 0QM5 96.50/96.75/96.87 broken call flys vs. 96.00/96.12 put spds ref 96.515

2,000 0QK5 96.50/96.62 call spds vs. 95.93/96.00 put spds ref 96.515

2,000 SFRN5 96.18/96.37/96.56 call flys ref 96.145

3,700 0QM5 96.75/96.87 call spds ref 96.505

Treasury Options: April serial options expire Friday

Over -55,000 FVJ5 108.25/108.75 call spds, 1.0 ref 107-31.25 to -30.75

+50,000 FVK5 110 calls, 8 total volume over 133,600 (OI only 15,805)

+8,000 TYM5 111.5 straddles, 224

+9,200 USK5 112/125 call over risk reversals, 8 ref 118-19

+50,000 FVK5 110 calls, 6.5 total volume over 61,600

over -53,000 FVJ5 108 calls, 7-7.5 (currently 10 bid/at 11)

over 10,300 FVJ5 107.5 puts, 0.5

over 17,400 TYJ5 111.5 calls, mostly 3-6, 8 last ref 111-06

4,000 wk1 TY 111.5/112/112.5 call trees ref 111-01.5 (exp 4/4)

3,500 TYK5 113/114 call spds, 8 ref 111-02.5

over 7,400 wk4 FV 107.25/107.5 put spds ref 107-29.25 to -29.5 (exp 3/28)

1,250 FVK5 106.25/106.5 put spds ref 108-00.25

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Bunds As BoE Vote Leans Hawkish

Gilts underperformed Bunds Thursday, with periphery EGB spreads widening.

- Core FI strengthened in the early morning European session as equities pulled back following the overnight post-Federal Reserve gains.

- But gains had reversed by early afternoon, alongside a bounce in US equities (which was not shared by European stocks).

- The BoE decision came in on the hawkish side with an 8-1 vote in favour of holding rates (vs a cut), compared to the 7-2 expected (Mann moved to vote for no change after calling for a 50bp cut last time out). Mixed UK labour market data brought little reaction.

- Both the UK and German curves bear flattened. A widening of periphery/semi-core EGB spreads in the morning was sustained through the session, with European equities likewise failing to regain ground. GGBs underperformed.

- Friday's schedule includes UK public sector finance and Eurozone consumer confidence data, with an appearance by ECB's Escriva.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.5bps at 2.171%, 5-Yr is down 2.9bps at 2.436%, 10-Yr is down 2.4bps at 2.78%, and 30-Yr is up 0.4bps at 3.094%.

- UK: The 2-Yr yield is up 3.3bps at 4.239%, 5-Yr is up 2bps at 4.313%, 10-Yr is up 1.5bps at 4.646%, and 30-Yr is up 0.2bps at 5.216%.

- Italian BTP spread up 2.7bps at 112.7bps / Greek up 3.6bps at 82.3bps

MNI OPTIONS: Limited, Mixed Trade Thursday Includes Bobl Upside

Thursday's Europe rates/bond options flow included:

- OEK5 117.50/118.50 call spread vs. 116.50/115.50 put spread paper paid 11 on 2K for the call spread, 44% delta

- RXM5 128/127/125/124 'wide' body put condor paper paid 26.5 & 27 on 2.5K

- ERM5 97.625/97.50 put spread paper paid 1.75 on 10k

- ERM5 97.75/98.00/98.25 call fly 4K given at 6.75

MNI FOREX: AUD and NZD Consolidate Significant Losses, EURUSD Extends Pullback

- The dollar index spent Thursday’s session steadily reversing the FOMC-inspired move, culminating in the DXY looking to end the day up 0.46%. The greenback was supported by a similar reversal lower for equities, as weakness for European benchmarks dragged the major US indices down, albeit by a more moderate amount.

- The waning risk sentiment left the likes of AUD and NZD at the bottom of the G10 leaderboard. For AUDUSD (-0.96%), we had noted that 0.6400 continued to provide important pivot resistance, and today’s resumption of weakness highlights the medium-term bearish technical outlook.

- Price action has been supported by the weaker-than-expected Australian jobs data overnight, and AUDUSD has significantly narrowed the gap to initial support, which is at 0.6259, the Mar 11 low. Below here, a move below key short-term support at 0.6187, the Mar 4 low, is required to resume the downtrend.

- Crude markets have firmed after the US sanctioned a Chinese “teapot” refinery for the first time, alongside further tankers carrying Iranian crude. Price dynamics prompted a solid reversal higher for the Canadian dollar, leaving USDCAD around unchanged levels.

- The Euro has also weakened, prompting EURUSD to extend its reversal from cycle highs to 140 pips, registering a low of 1.0815. Support for the pair remains much further out, at 1.0599, the 50-day EMA and a short-term pivot level.

- Both SEK and CHF remain weaker on the session, with the Riksbank averting any hawkish risks and the Swiss National Bank siding with the consensus and delivering a 25bp rate cut to 0.25%.

- The Bank of England decision had some very marginal hawkish additions (Mann voting for unchanged), however, the small pop higher for GBPUSD was swiftly pared. Cable has been unable to maintain a rally above 1.30 in recent sessions, prompting the pair to drift back towards 1.2950 ahead of the APAC crossover.

- Japan national CPI crosses early Friday, before Canadian retail sales headlines the North American calendar.

MNI FX OPTIONS: Expiries for Mar21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0785(E764mln), $1.0800(E1.2bln), $1.0900(E1.5bln)

- USD/JPY: Y148.48-50($519mln), Y149.00($1.7bln), Y149.58-75($1.0bln), Y149.85-00($2.0bln)

- EUR/GBP: Gbp0.8350-55(E787mln), Gbp0.8400(E600mln)

- AUD/USD: $0.6300-01(A$697mln)

- USD/CAD: C$1.4280-00($3.8bln)

- USD/CNY: Cny7.2430($600mln)

MNI US STOCKS: Late Equities Roundup: Off Early Highs, Software/Services Weighing

- Stocks have retreated since posting session highs late Thursday morning as Information Technology and Consumer Staples stocks traded weaker. Currently, the DJIA trades down down 1.72 points (0%) at 41964.94, S&P E-Minis down 13.5 points (-0.24%) at 5716.75, Nasdaq down 53.9 points (-0.3%) at 17697.71.

- Software & services shares weighed on the Tech sector in the second half with Accenture PLC -7.66%, Gartner Inc -5.64%, EPAM Systems Inc -4.59% and Cognizant Technology Solutions -3.20%.

- Consumer Staples were weighed by Hershey Co & General Mills, both -1.40%, while Bunge Global and Kroger both declined -1.28%.

- Meanwhile, Energy and Financial sectors led gainers in the second half, oil and gas shares bouncing as crude held gains (WTI +1.10 at 68.26): Marathon Petroleum Corp +0.92%, ConocoPhillips +0.87%, Schlumberger +0.63% and Kinder Morgan Inc +0.54%.

- Banks and insurance names buoyed the Financial sector: Allstate Corp +2.86%, Discover Financial Services +1.36% and Citigroup Inc +1.01%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bearish Structure Remains Intact

- RES 4: 5946.82 50-day EMA

- RES 3: 5864.25 Low Jan 13 and a recent breakout level

- RES 2: 5820.86 20-day EMA

- RES 1: 5770.50 High Mar 19

- PRICE: 5704.25 @ 13:34 GMT Mar 20

- SUP 1: 5559.75 Low Mar 13 and the bear trigger

- SUP 2: 5483.50 2.00 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 3: 5396.00 2.236 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 4: 5341.87 2.382 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

The trend condition in S&P E-Minis is bearish. Moving average studies are unchanged and remain in a bear-mode set-up highlighting a dominant downtrend. Sights are on 5483.50, a Fibonacci projection. Note that the short-term trend condition is oversold. Recent gains are considered corrective and the bounce is allowing this set-up to unwind. Firm resistance to watch is 5946.82, the 50-day EMA.

MNI COMMODITIES: Crude Gains On New US Sanctions, Gold Steady After New Record High

- Crude markets have firmed after the US sanctioned a Chinese independent refinery for the first time, alongside further tankers carrying Iranian crude. Uncertainty around any ceasefire arrangement in Ukraine added support, along with heightened geopolitical tensions in the Middle East.

- WTI Apr 25 is up by 1.6% at $68.3/bbl.

- US sanctions today are the first instance of a China teapot refinery being added, the main outlet for Iranian oil. A further eight Iranian vessels were also added to the Washington OFAC list today.

- For WTI futures, a bearish condition remains intact, with recent weakness paving the way for an extension towards $63.73 next, the Oct 10 ‘24 low. On the upside, key pivot resistance to watch is $69.51, 50-day EMA.

- Meanwhile, Henry Hub has extended losses today to hit its lowest close since Feb 28. Milder weather and an earlier than expected flip to net storage injections add pressure.

- US Natgas Apr 25 is down by 6% at $3.99/mmbtu.

- Spot gold rose to a fresh record high at $3,057 earlier in the session, before giving up gains to trade 0.1% lower on the day at $3,043/oz.

- A clear uptrend in gold is intact and this week’s resumption of the bull cycle reinforces current conditions.

- Today’s fresh trend high reinforces the bull theme and sights are on $3,079.2 next, a Fibonacci projection.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 21/03/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/03/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/03/2025 | 0900/1000 | ** | EZ Current Account | |

| 21/03/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 21/03/2025 | 1230/0830 | ** | Retail Trade | |

| 21/03/2025 | 1305/0905 | New York Fed's John Williams | ||

| 21/03/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/03/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/03/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |