Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI EXCLUSIVE: Fed Could Relax Rules to Boost Dealer Capacity

- MNI EXCLUSIVE: RCEP Boosts China In Asia Amid Decoupling Fears

- MNI POLICY: BOC Poll Sees Surge in Investor Fears of Mkt Shock

- MNI US Treasury Sec Mnuchin: Plenty Of Firepower Left

- MNUCHIN, POWELL TO TESTIFY BEFORE SENATE BANKING CMTE DEC. 1, Bbg

- CHICAGO FED EVANS: TREASURY DECISION ON FED PROGRAMS `DISAPPOINTING', Bbg

US

FED: The Federal Reserve may extend regulatory relief for banks and push for wider clearing of Treasuries to help dealers provide liquidity during market volatility, former Fed officials, researchers and market sources told MNI. For more see 11/20 MNI Policy Main Wire at 1047ET.

FED: Chicago Fed's Evans on CNBC:- Evans said that 13-3 facilities have been "helpful" as a "backstop", says the Treasury's decision not to extend beyond end-year is "disappointing". Says Fed providing substantial monetary support. But there are risks from virus spread, moving into the 'indoor season', a lot of challenges/risks - so it would be good to have more support coming from "all directions".

- Asked if Fed purchases need to be increased, Evans notes what the Fed has already done so far. Says Fed looking at the scale of its asset purchases, and the role that they can play, but providing tremendous amounts of support already. "In a pretty good place at the moment to see how everything is going to play out" (transition, fiscal stimulus, public health).

- Interestingly, Evans looks past the December FOMC (which many observers have pointed to for potential action): Says he's looking at Spring for better understanding of labor dynamics as to whether the Fed should do more.

- Extending maturity of asset purchases 'part of the tool kit'; can increase the size of the balance sheet more quickly if appropriate.

US: Treasury Secretary Mnuchin on CNBC addresses the non-extension of Fed/Treasury 13-3 lending programs under the CARES Act beyond the end-year expiration date:

- Says re the controversy over the past 24 hours and the Fed's opposition to the decision - it's "straightforward and people are missing the issue. Congressional intent is that it expires on Dec 31 this year". Says he and Powell have discussed for the past few weeks.

- Mnuchin notes there is only $25B of loans outstanding, and to the extent that more is required, there is $750B of firepower so the gov't still has plenty of lending capacity.

- Mnuchin says they'll work with Congress to re-appropriate the unused funds for proceeds such as PPP loans. Regarding Chicago Fed's Evans' comments earlier in CNBC, Mnuchin says he "would go ask [Evans] to read the law, or speak to the Chair of the Committee [Powell]". If all else is equal, the Fed would always like to keep its tools outstanding. "We don't need to buy more corporate bonds, the municipal market is working."

- In its 2021 US economic outlook, JPMorgan argues that "recent restrictions on activity associated with the latest surge in [COVID] case counts will likely deliver negative growth in 1Q21", at a -1.0% annualized rate for the quarter (following a forecast +2.8% in Q420).

- However, JPM sees a bounce back thereafter in part due to recent "favorable news on the vaccine trials", and an anticipated further $1trn in fiscal support ("with the most likely timing on agreement being late 1Q21"). So +4.5% growth in Q2, and +6.5% in Q3.

- However inflation to remain subdued, with lingering labor market slack keeping inflation within a 1.5-2.0% range next year "despite the long-speculated death of the Phillips Curve". Core PCE to hit 2% in mid-2021 for a few months before falling back below target by end-year.

- This will keep the Fed "mostly out of the picture", with no rate hikes at least through end-2022. But notes that they recently changed their call for the Dec 2020 FOMC, now seeing an extension of maturity of purchases.

- And if unemployment looks to be heading below 5% by mid-2022, "this could start discussions late next year of the dreaded T-word: tapering".

ASIA

CHINA: The world's biggest free trade deal will help China strengthen its Asian supply chains to rival western-led networks at a time of worsening relations with the U.S., policy advisors in Beijing told MNI. For more see 11/20 MNI Policy Main Wire at 0757ET.

CANADA

BOC: The Bank of Canada reported a surge in investors worried about the possibility of a market shock in the next year, according to a survey published Friday, mostly because the pandemic will dent the global economy or trigger a rush of defaults. For more see 11/20 MNI Policy Main Wire at 1138ET.

OVERNIGHT DATA

US DATA: Q4 NY Fed GDP Nowcast

- New York Fed Staff Nowcast stands at 2.86% for 2020:Q4. According to the NY Fed:

- "A negative surprise from retail sales data was largely offset by positive data revisions, leaving the nowcast unchanged."

CANADA FLASH OCT RETAIL SALES 'RELATIVELY UNCHANGED'

CANADIAN SEP RETAIL SALES +1.1%; SALES EX-AUTOS/PARTS +1.0%

CANADA SEP RETAIL SALES EX-AUTOS/PARTS-GASOLINE +1.1%

MARKET SNAPSHOT

- DJIA down 188.01 points (-0.64%) at 29345.43

- S&P E-Mini Future down 17.75 points (-0.5%) at 3569.75

- Nasdaq down 19.8 points (-0.2%) at 11920.09

- US 10-Yr yield is down 0 bps at 0.8292%

- US Dec 10Y are up 4.5/32 at 138-16

- EURUSD down 0.0016 (-0.13%) at 1.1858

- USDJPY up 0.08 (0.08%) at 103.83

- WTI Crude Oil (front-month) up $0.41 (0.98%) at $42.15

- Gold is up $5.65 (0.3%) at $1873.50

- European bourses closing levels:

- EuroStoxx 50 up 15.63 points (0.45%) at 3467.6

- FTSE 100 up 17.1 points (0.27%) at 6351.45

- German DAX up 51.09 points (0.39%) at 13137.25

- French CAC 40 up 21.23 points (0.39%) at 5495.89

US TSY SUMMARY: Tsys Well Bid On Late Equity Selling

Bonds leading late session rally, levels back up to early overnight highs, yield curves flatter as equities extended session lows after the bell (ESZ0 -23.0).

- Decent overall volumes a little deceiving as session rather a quiet late week affair -- is tied to broad pick-up in Dec/Mar rolling with limited time ahead first notice on Nov 30 w/ Thanksgiving holiday next Thu (Friday early close). Near 350,000 TYZ/TYH and 375 FVZ/FVH rolls traded by the bell.

- Data-lite session, there were several Fed speakers on the session largely repeating the company line of lower for longer, general willingness to extend duration. Chicago Fed Evans on CNBC earlier: Extending maturity of asset purchases 'part of the tool kit'; can increase the size of the balance sheet more quickly if appropriate.

- Evans also said that 13-3 facilities have been "helpful" as a "backstop", says the Treasury's decision not to extend beyond end-year is "disappointing". Says Fed providing substantial monetary support.

- Late headline announced Fed Chair Powell and Tsy Sec Mnuchin will testify before the Senate Banking Committee on Dec 1.

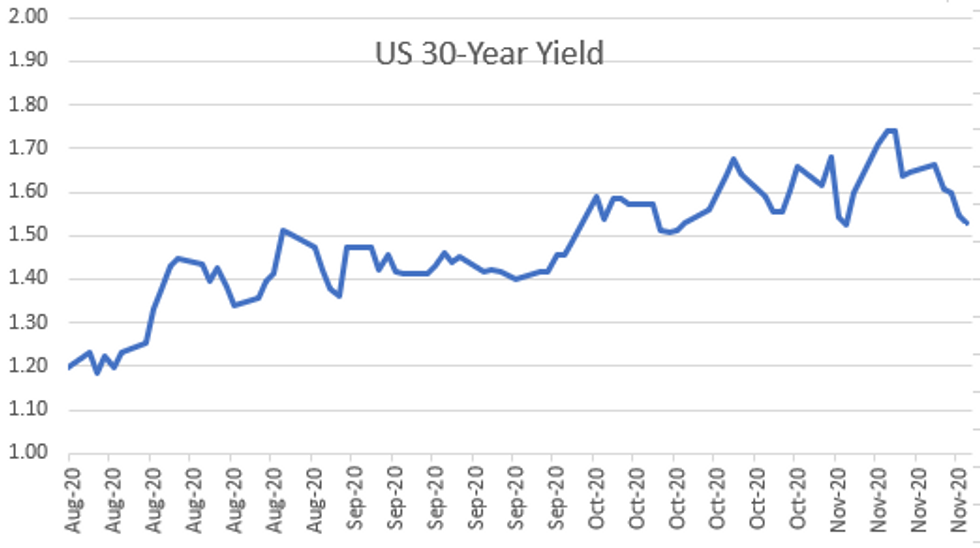

- The 2-Yr yield is down 0.2bps at 0.1594%, 5-Yr is down 0.1bps at 0.3715%, 10-Yr is down 0.3bps at 0.826%, and 30-Yr is down 1.8bps at 1.5273%.

US TSY FUTURES CLOSE: Near Late Session Highs

Futures holding just off late session highs, yield curves flatter for the most part, relatively modest risk-off support with equities making session lows after the bell. Update:

- 3M10Y -0.003, 76.331 (L: 74.759 / H: 78.29)

- 2Y10Y +0.181, 66.582 (L: 65.098 / H: 68.541)

- 2Y30Y -1.107, 136.9 (L: 136.075 / H: 140.069)

- 5Y30Y -1.473, 115.61 (L: 115.16 / H: 118.136)

- Current futures levels:

- Dec 2Y up 0.37/32 at 110-12.37 (L: 110-12.12 / H: 110-12.62)

- Dec 5Y up 1.5/32 at 125-19.25 (L: 125-17.75 / H: 125-20.5)

- Dec 10Y up 4.5/32 at 138-16 (L: 138-12 / H: 138-20)

- Dec 30Y up 25/32 at 174-1 (L: 173-15 / H: 174-09)

- Dec Ultra 30Y up 1-22/32 at 219-11 (L: 217-31 / H: 219-21)

US TSY FUTURES: December/March Futures Roll Update

Dec/Mar roll volumes surge ahead Nov 30 "first notice" date approaches, position holders contend with shortened Thanksgiving holiday workweek next week. Dec futures won't expire until mid-late December: 10s, 30s and Ultras on 12/21; 2s & 5s 12/31.

- TUZ/TUH appr 182,500 0.125 last; 14% complete

- FVZ/FVH appr 376,100 -10.0 last; 16% complete

- TYZ/TYH appr 341,700 12.50 last; 17% complete

- UXYZ/UXYH under 145,700, 18.5 last; 20% complete

- USZ/USH 166,500, -1-11.75 last; 16% complete

- WNZ/WNH 135,400, 1-21 last; 25% complete

US EURODLR FUTURES CLOSE: Lead Quarterly Steady After 3M Set' New All-Tim Low

Futures holding steady inthe short end to modestly higher out the strip. Lead quarterly EDZ0 steady since 3M LIBOR set -0.00775 to 0.20488% (-0.01712/wk) -- new all time low (prior 0.20500% on 11/9/20). Current levels:

- Dec 20 steady at 99.753

- Mar 21 steady at 99.785

- Jun 21 steady at 99.790

- Sep 21 +0.005 at 99.790

- Red Pack (Dec 21-Sep 22) steady to +0.005

- Green Pack (Dec 22-Sep 23) +0.005 to +0.010

- Blue Pack (Dec 23-Sep 24) +0.005 to +0.015

- Gold Pack (Dec 24-Sep 25) +0.015 to +0.020

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N +0.00025 at 0.08263% (-0.00062/wk)

- 1 Month +0.00463 to 0.15013% (+0.01375/wk)

- 3 Month -0.00775 to 0.20488% (-0.01712/wk)**

- 6 Month -0.00675 to 0.24875% (+0.00275/wk)

- 1 Year -0.00213 to 0.33650% (-0.00288/wk)

- ** 3M New record Low 0.20488% on 11/20/20 (prior 0.20500% on 11/9/20)

- Daily Effective Fed Funds Rate: 0.08% volume: $62B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $182B

- Secured Overnight Financing Rate (SOFR): 0.06%, $911B

- Broad General Collateral Rate (BGCR): 0.04%, $344B

- Tri-Party General Collateral Rate (TGCR): 0.04%, $316B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $12.801B accepted vs. $32.255B submission

- Next scheduled purchases:

- Mon 11/23 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Tue 11/24 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

PIPELINE: Issuance Running Total $109.48B For Month

Date $MM Issuer (Priced *, Launch #)

- 11/20 $Benchmark Rep of Serbia investor calls

- -

- $7.555B Priced Thursday; $65.13B/wk

- 11/19 $3B *Charter Comm's $1B +11Y +147, $650M tap 30Y +207, $1.35B +40Y +227

- 11/19 $1.8B *AES Corp $800M 5Y +100, $1B 10Y +160

- 11/19 $1.2B *Allstate 5Y +40a, 10Y +70a

- 11/19 $555M *Uzbekistan 10Y 3.7%

- 11/19 $500M *Goldman Sachs +5Y +255

- 11/19 $500M *Massachusetts Electric 10Y +88

FOREX: NZD/USD Hits Multi-Year High

Strength in antipodean FX persisted throughout the Friday session, prompting a new multi-year high in NZD/USD printed up at 0.6950, clearing the best levels seen in 2019 to narrow the gap with December 2018 high of 0.6970.

- Initial USD weakness faded into the Friday close as EUR/USD was sold into the Friday WMR fix. Ranges, however, were tight, providing few new technical or fundamental signals as markets begin to hone in on the December FOMC meeting as the next flashpoint for price action.

- NZD, AUD and GBP were the strongest Friday, with SEK, EUR the weakest.

- Focus turns to global prelim November PMI numbers, IFO numbers from Germany and FOMC minutes. Thanksgiving holidays in the coming week, however, could keep market action light.

EGBs-GILTS CASH CLOSE: Resolving In A Bullish Direction To End The Week

Bunds and Gilts ultimately resolved in a bullish direction for the most part, with an early move lower in yields reversing only temporarily in the early afternoon. Periphery spreads a little wider.

- Focus is swiftly turning to next week's political agenda with EU budget negotiations and another fraught schedule of Brexit talks (reports out of this morning's briefing to EU ambassadors on progress of the talks were mixed).

- Also of note Monday will be Flash November PMIs.

- Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is down 1.6bps at -0.751%, 5-Yr is down 1.3bps at -0.761%, 10-Yr is down 1.2bps at -0.583%, and 30-Yr is down 0.2bps at -0.176%.

- UK: The 2-Yr yield is down 1.3bps at -0.042%, 5-Yr is down 1.5bps at -0.007%, 10-Yr is down 2.1bps at 0.302%, and 30-Yr is down 3.1bps at 0.889%.

- Italian BTP spread up 0.3bps at 121.6bps

- Spanish bond spread up 0.7bps at 64.8bps

- Portuguese PGB spread unchanged at 60.6bps

- Greek bond spread up 1.6bps at 127.8bps

UP TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.