Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI POLICY-Fed's Clarida Sees Brighter Economic Outlook

- FED CLARIDA: Tapering And IOER Hike Can Wait

- MNI BRIEF: US 2020 Retail Imports Set to Break Record

- MNI BRIEF: Biden To Offer Outline of Fiscal Package Next Week

- FED CLARIDA: COULD SEE INFLATION ABOVE 2% DUE TO BASE EFFECTS, Bbg

- FED CLARIDA: TIME TO SLOW PACE OF BOND BUYING `WELL DOWN THE ROAD, Bbg

- FED'S CLARIDA: EXPECTS ECONOMY TO TURN IN 'VERY, VERY' IMPRESSIVE PERFORMANCE LATER THIS YEAR, Rtrs

US

FED: Federal Reserve Vice Chair Richard Clarida said Friday the economy's prospects have brightened because of progress on the coronavirus vaccine despite short-term pain from a surge in cases and deaths.

- "The prospects for the economy in 2021 and beyond have brightened and the downside risk to the outlook has diminished," Clarida said in prepared virtual remarks to the Council on Foreign Relations. For more see MNI Policy Mainwire at 1004ET.

- On Fed tapering: "It will be quite some time before we begin tapering our purchases", and says he expects the current buying pace to be maintained through 2021.

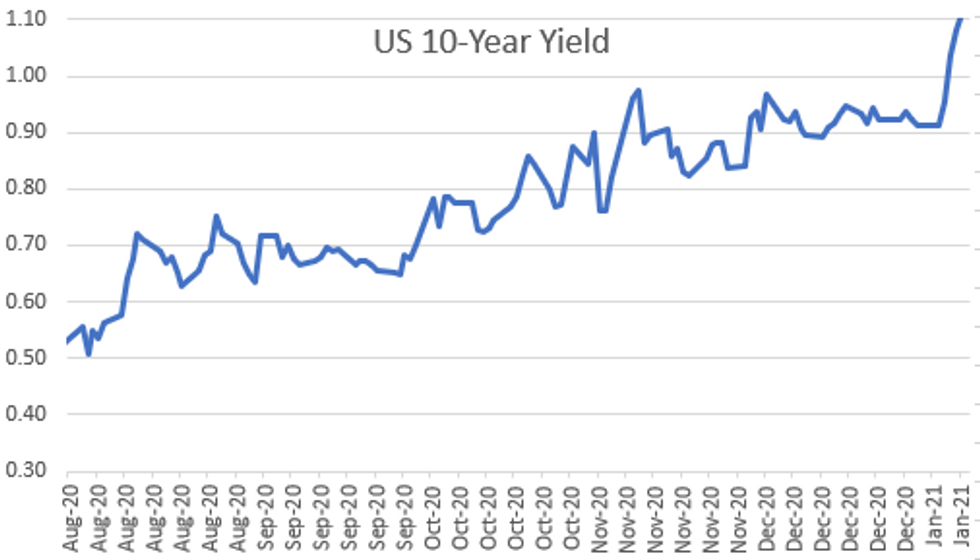

- On adjusting purchase maturity: Says there is no need now or in the near-term to adjust the duration of Tsy purchases. Notes he's not concerned by a 10-Yr Tsy yield above 1.0% - earlier he noted we are still in a regime of "incredibly low" bond yields.

- On IOER: Says he does not see a rise in interest paid on excess reserves on the near-term horizon, and more interestingly says that he does not perceive a need to do that before wider rate liftoff. Note the Fed SEP median is not pencilling in a hike through 2023.

- On today's jobs report: Clarida says that while the headline number was "disappointing", losses were concentrated in COVID lockdown-sensitive hospitality sectors, and he does not expect that jobs pattern to persist into 2021. This echoes comments from Powell and others on some sectors doing better than others in the pandemic, pointing to fiscal/gov't policy being more effective than mon pol in addressing.

- On fiscal policy: Says that he has not yet analyzed the potential for more stimulus after the Georgia Senate outcome (making it easier for the Democrats to pass a fiscal package).

- The Delaware Democrat said his package will include small business aid; additional money for USD2,000 direct checks; billions for vaccine distribution; extension of weekly unemployment benefits; and additional aid to states. Investors predict a package could be USD900 billion

US: Goldman Sachs Raise 2021 US Growth Forecast

- With Democratic control over Congress and the White House, GS further increase their forecasts for a U.S. growth and now expect +6.4% this year (vs. a prior forecast of 5.9% and consensus forecast of only 3.9%).

- Growth should be boosted by the passage of an estimated $750 billion fiscal stimulus package in February or March. The positive growth effects of this stimulus will be more lagged than usual, as new virus strains and slow progress on vaccination weigh on the economy-but consumer spending should rebound strongly in the second and third quarters to push growth higher in the back half of the year.

OVERNIGHT DATA

US DEC NONFARM PAYROLLS -140K; PRIVATE -95K, GOVT -45K

US PRIOR MONTHS PAYROLLS REVISED: NOV +336K; OCT +654K

US DEC AVERAGE HOURLY EARNINGS +0.8% Vs NOV +0.3%; +5.1% YOY

US DEC AVERAGE WEEKLY HOURS 34.7 HRS

US DEC UNEMPLOYMENT RATE 6.7%

- Today's December employment report shouldn't change much on the near-term policy outlook.

- While the -140k headline figure was a disappointment vs +50k consensus, it was almost perfectly offset by +135k cumulative revisions to the previous two months' job gains, and the unemployment rate was unchanged at 6.7%.

- As Fed Chair Powell among others has indicated, the FOMC is already of the mind that the COVID lockdowns are affecting some sectors more than others (the hospitality sector lost ~500k jobs in Dec), and that targeted gov't policy and not monetary policy is the right approach. We await comments by Fed Vice Chair Clarida (1100ET) on the economic / mon pol outlook.

- As for fiscal policy, this wasn't enough of a negative report to get the juices flowing on bigger fiscal stimulus than has already been discussed by the incoming Biden administration, nor so good that it'll nudge fiscal conservatives to sit more firmly on the sidelines.

- There is some talk about strong wage growth (avg hourly earnings +5.1% Y/Y vs +4.5% expected) but this appears to be a product of lower-wage positions being lost rather than a sudden "real" surge in workers' wages.

CANADA DEC EMPLOYMENT -62.6K; JOBLESS RATE +8.6%

CANADA DEC FULL-TIME JOBS +36.5K; PART-TIME -99.0K

- The rise in unemployment was blunted as about 99,000 more people did not want a job, and there could be further weakness as more local shutdowns took effect in recent weeks.

MARKETS SNAPSHOT

- DJIA down 48.32 points (-0.16%) at 30873.83

- S&P E-Mini Future up 6.75 points (0.18%) at 3794.25

- Nasdaq up 69.6 points (0.5%) at 13097.47

- US 10-Yr yield is up 2.1 bps at 1.1%

- US Mar 10Y are down 8.5/32 at 136-22

- EURUSD down 0.0058 (-0.47%) at 1.2208

- USDJPY up 0.12 (0.12%) at 103.98

- WTI Crude Oil (front-month) up $1.32 (2.6%) at $51.93

- Gold is down $68.47 (-3.58%) at $1841.45

- European bourses closing levels:

- EuroStoxx 50 up 22.63 points (0.62%) at 3645.05

- FTSE 100 up 16.3 points (0.24%) at 6873.26

- German DAX up 81.29 points (0.58%) at 14049.53

- French CAC 40 up 37.03 points (0.65%) at 5706.88

US TSY SUMMARY: Choppy Day

Another day in the rearview after the midweek political mayhem that surrounded the DC siege, market attention turned to more prosaic matters of employment figures, economic outlooks and a debate over additional stimulus.

- Alright, there was a persistent droning debate over removing Trump from office by impeachment, the 25th amendment or by resignation through the day -- but focus was more on the much weaker than expected Dec NFP -140k vs +50k est.

- Rates gapped bid but just as quickly reversed/extended lows as focus on large upward revisions to Oct (+645k) and Nov (+336K) kicked off much better selling pressure w/over 90,000 TYH1 from 136-25 to -22. More chop on Dec headline miss, dampening prospect of carry-over surge in early 2021 was dampened by Fed VC Clarida expecting "brighter economic outlook" later in yr and beyond.

- Heavy volumes, rates clawed off midday lows as equities reversed/traded weaker as D-WV Manchin expressed opposition to $2k stimulus. Late headlines that Pres elect Biden will sketch out another economic relief package next wk helped stocks recover late.

- The 2-Yr yield is unchanged at 0.1369%, 5-Yr is up 2.7bps at 0.4865%, 10-Yr is up 3.9bps at 1.1187%, and 30-Yr is up 2.3bps at 1.8761%.

US TSY FUTURES CLOSE: Weaker/Off Lows

Heavy volumes on choppy trade Fri after big Dec NFP miss (-140k vs. +50k est), focus turned to huge up-rev's for Oct and Nov. That said, optimistic Fed speak (Clarida) helped risk appetite for equities as did hopes of more stimulus w/details from Biden expected next week. Huge 10s/Ultra-bond flattener took profits after curves hit multi-year highs on week.

- 3M10Y +3.496, 102.824 (L: 98.329 / H: 103.761)

- 2Y10Y +3.462, 97.129 (L: 93.526 / H: 98.491)

- 2Y30Y +1.597, 172.796 (L: 169.328 / H: 175.214)

- 5Y30Y -1.201, 138.196 (L: 136.924 / H: 141.294)

- Current futures levels:

- Mar 2Y steady at at 110-14.25 (L: 110-13.875 / H: 110-14.75)

- Mar 5Y down 4.75/32 at 125-18 (L: 125-16.75 / H: 125-22.5)

- Mar 10Y down 11.5/32 at 136-19 (L: 136-16.5 / H: 136-29.5)

- Mar 30Y down 19/32 at 168-20 (L: 168-05 / H: 169-13)

- Mar Ultra 30Y down 30/32 at 204-18 (L: 203-20 / H: 206-02)

US EURODOLLAR FUTURES CLOSE: Long End Underperforms

Futures holding steady in the short end to progressively weaker out the strip, heavy volumes on day with Reds-Greens trading avg 225-240k each expiry. Lead quarterly EDH1 held steady since 3M LIBOR set -0.00037 to 0.22438% (-0.01405/wk).

- Mar 21 steady at 99.820

- Jun 21 steady at 99.825

- Sep 21 steady at 99.815

- Dec 21 steady at 99.775

- Red Pack (Mar 22-Dec 22) -0.03 to steady

- Green Pack (Mar 23-Dec 23) -0.055 to -0.035

- Blue Pack (Mar 24-Dec 24) -0.08 to -0.065

- Gold Pack (Mar 25-Dec 25) -0.085 to -0.075

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00000 at 0.08675% (+0.00912/wk)

- 1 Month -0.00625 to 0.12638 (-0.01750/wk)

- 3 Month -0.00037 to 0.22438% (-0.01405/wk)

- 6 Month -0.00475 to 0.24650% (-0.01113/wk)

- 1 Year +0.00038 to 0.32963% (-0.01225/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $59B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $142B

- Secured Overnight Financing Rate (SOFR): 0.10%, $951B

- Broad General Collateral Rate (BGCR): 0.08%, $361B

- Tri-Party General Collateral Rate (TGCR): 0.08%, $340B

- (rate, volume levels reflect prior session)

FED: NY Fed Operational Purchases

- Tsy 0Y-2.25Y, $12.801B accepted vs. $37.746B submission

- Next week's scheduled purchases:

- Mon 1/11 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Tue 1/12 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Wed 1/13 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Thu 1/14 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Thu 01/14 Next forward schedule release at 1500ET

PIPELINE: Strong Start For 2021 With Near $75B Issuance

- Date $MM Issuer (Priced *, Launch #)

- $7.25B Priced Thursday; $74.05B/wk

- 01/07 $3.5B *World Bank (IRBD) $2.35B 2Y FRN SOFR+13, $1.15B 2027 Tap SOFR+34

- 01/07 $3B *Standard Chartered $1.5B 4NC3 +89, $1.5B 6NC5 +100

- 01/07 $750M *Northwestern Mutual Global Funding 5Y +38

- $12.9B Priced Wednesday; $66.8B/wk

- 01/06 $4B *ADB 10Y +15

- 01/06 $3B *Toyota Motor Cr $1B 3Y +25, $750M 3Y FRN SOFR+33, $700M 5Y +40, $550M 10Y +62.5

- 01/06 $2.25B *BNP Paribas 6NC5 +90

- 01/06 $2B *Kommunalbanken 5Y +9

- 01/06 $1B *AerCap Ireland 5Y +155

- 01/06 $650M *Ares Capital +5Y +180

FOREX: US$ Mixed As Market Looks Through NFP

The headline change in nonfarm payrolls missed expectations, although once net revisions were factored in the release was broadly inline with market expectations. As a result, markets looked through the December NFP release, with more focus resting on Biden's looming inauguration on January 20th and the continued upside in US equities.

- The USD traded mixed, with the EUR one of the poorest performers and GBP among the strongest. USD/JPY finished the week particularly well, extending the recovery off Wednesday's 102.59 low. The pair is testing the 50-day EMA at 103.97. A break and close above would strengthen S/T bullish conditions and signal scope for stronger rally.

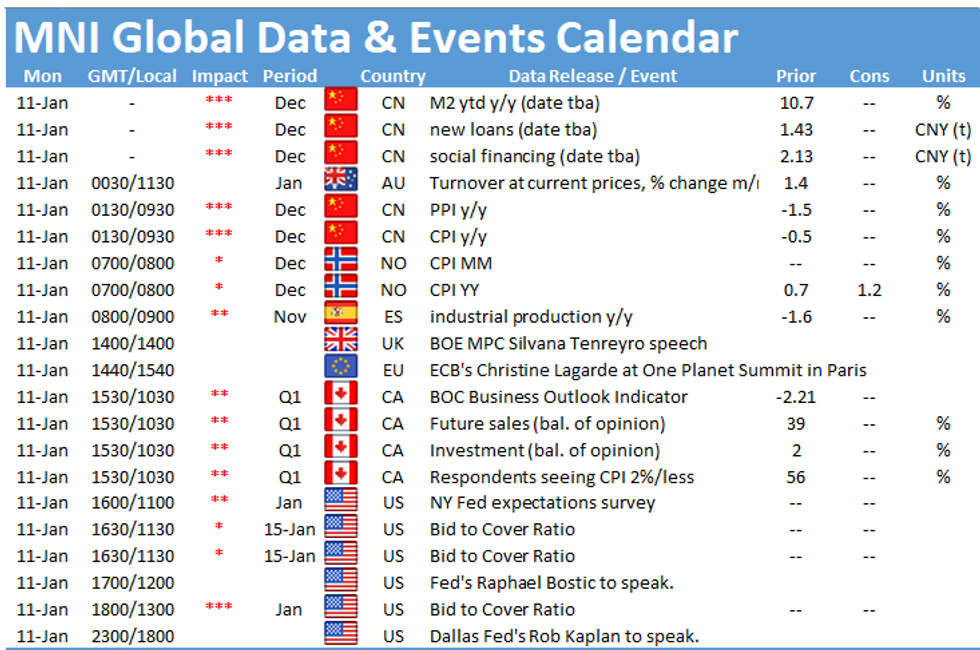

- Various inflation gauges take focus in the coming week, with CPI & PPI data due from China, Japan and the US. The central bank speakers schedule will also be of interest, with notable speeches including BoE's Tenreyro on negative rates, ECB's Lagarde, Fed's Powell and Fed's Clarida on the topic of the new Fed framework.

EGBs-GILTS CASH CLOSE: BTP Yield Touches New All-Time Low

While Bunds and Gilts traded with little direction, BTPs were the star of the session, with the 10-Yr yield touching a fresh all-time low of 0.504% before retracing higher.

- A fairly constructive if largely uneventful morning session (no 1st tier data. no issuance and no speakers) ahead of US Nonfarm payrolls. While we saw some knee-jerk downside price action on the latter, ultimately Gilts and Bunds settled in ranges.

- The ECB speaker slate is a little more active next week, with Lagarde among others appearing. Plenty of supply too, including the UK, EFSF, Netherlands, Austria, Germany, Portugal, and Italy.

- Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 0.3bps at -0.701%, 5-Yr is up 0.4bps at -0.73%, 10-Yr is up 0.3bps at -0.519%, and 30-Yr is up 0.5bps at -0.126%.

- UK: The 2-Yr yield is up 0.7bps at -0.128%, 5-Yr is up 1.2bps at -0.044%, 10-Yr is up 0.4bps at 0.288%, and 30-Yr is down 0.3bps at 0.87%.

- Italian BTP spread down 3bps at 105bps / Spanish down 0.6bps at 56bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.