Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- U.S. CPI SURGES IN APRIL, FASTEST PACE SINCE 2008

- CORE CPI HITS HIGHEST M/M RATE SINCE 1981; FASTEST CORE GOODS INFLATION SINCE AT LEAST 1950s

- FED'S CLARIDA: "SOME TIME" BEFORE TAPERING; FED "WON'T HESITATE" TO FIGHT INFLATION IF NEEDED

- U.S. GASOLINE OUTAGES RISE AS AVG PRICE HITS 6+ YEAR HIGH

- CHENEY REMOVED AS U.S. HOUSE G.O.P. CONFERENCE CHAIR

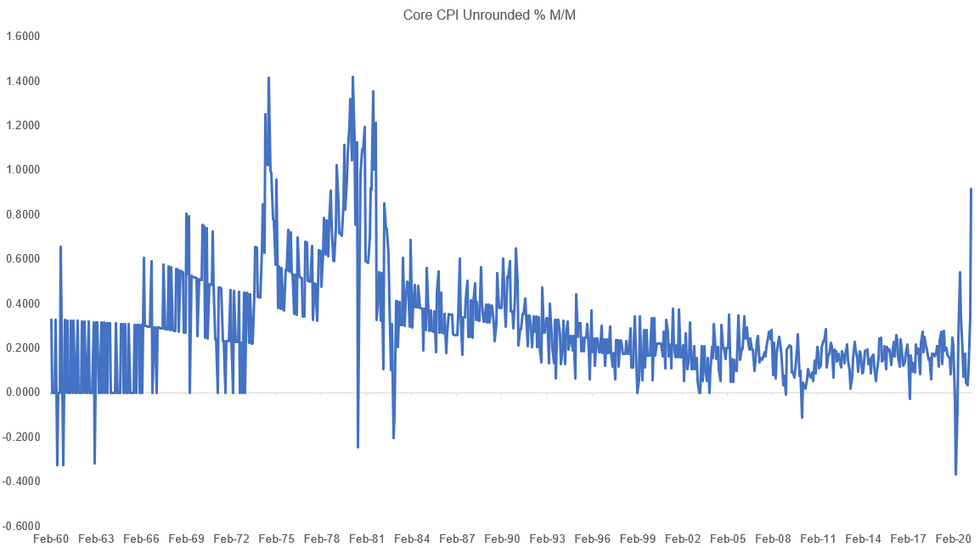

Fig. 1: U.S. April Core M/M Inflation Highest Since Early 1980s

Source: BLS, MNI

Source: BLS, MNI

NEWS:

U.S. CPI (MNI): Monthly CPI growth surged in April, the Bureau of Labor Statistics said Wednesday, with year-over-year headline and core inflation advancing at the fastest pace in roughly a decade. CPI rose 0.8% in April, much stronger than market expectations for a 0.2% gain. Food prices were up 0.4%, while the energy index fell slightly as the 1.4% decline in gasoline prices more than offset price increases in electricity and gas, the BLS said. From a year earlier, CPI was up 4.2%, the largest increase annual increase since September 2008. Excluding food and energy, core CPI was up 0.9% in April, the largest monthly increase since 1982, the BLS said. Nearly all major components increased in April, with used vehicles up 10%, the most since 1953, airline fares up 10.2%, and shelter up 0.4%. From a year earlier, core CPI was up 3%, the largest gain since 1996.

U.S. CPI (MNI): The unrounded core CPI print M/M was the highest (unrounded) since September 1981. Core goods % M/M looks like by far the biggest increase ever in the series going back to the late 1950s, at +2.0% (previous high was August 1974's +1.5%) - core services "just" +0.5% (but highest since Oct 1992). Core goods now rising 4.4% Y/Y, decisively eclipsing services at +2.5%. The breakdown is interesting too: big contributors to services included airfares (+10.2% M/M) and lodging away from home (+7.6% M/M). But other areas were relatively tame: primary rents and owners' equivalent rent each +0.2%M/M. Were it not for these categories remaining subdued, we could have seen an even higher overall print. Used cars were +10.0% M/M (the biggest rise since the series began in 1953) and was responsible for 1/3 of the overall inflation rise. This closely-watched category has quickly caught up to some of the used car price surveys analysts pointed to for an April rise. This could effectively mean though that some of the price increase was "brought forward" from previous months.

FED (MNI): The U.S. economy remains far from ready for higher interest rates and it would likely be "some time" before the Fed tapers QE, Federal Reserve Vice Chair Richard Clarida said Wednesday, noting his disappointment with the latest jobs report. "Notwithstanding the recent flow of encouraging macroeconomic data, the economy remains a long way from our goals, and it is likely to take some time for substantial further progress to be achieved," he told a virtual conference of business economists.

FED (MNI): Fed Vice Chair Clarida causing a bit of a stir with his post-inflation comments this morning that the Fed doesn't have "unlimited tolerance" for inflation; that it "won't hesitate to act" if inflation expectations become unanchored; and that he'll be watching long-term inflation expectation measures very closely. These comments have been seen as hawkish, but he's spending a lot of time in dove mode too, rationalizing the huge upside surprise in the CPI report (andplaying up the downside miss in the jobs report, suggesting continued emphasis on the employment mandate).

FED (BBG): "I am expecting a lot of volatility at least through September," Federal Reserve Bank of Atlanta President Raphael Bostic says, referring to readings on inflation. "Then we will have to see what is happening with the supply chain disruptions and the commodities prices and those sorts of issues"". So for the next four to five months, I think we are going to see volatility and there's going to be a lot of noise that surrounds the true signal"

U.S. (MNI): Oil/refined products analyst @GasBuddyGuy re gasoline outages across the US in light of the Colonial Pipeline outage, writes: "Tuesday US gasoline demand was up 14.3% from the prior Tuesday. Week to datethrough Tuesday, gasoline demand is up 10.7% WoW...The national average priceof gasoline has reached $3 per gallon for the first time October 30, 2014" * "GASOLINE OUTAGES as of 6am CT... percent of all stations in state withoutgasoline: GA 15.4% / AL 1.8% / TN 2.8%/ SC 13.4% / NC 24.8%/ FL 4.2%/ VA 15.0% / MD 3.5%"

U.S. POLITICS (MNI): As widely expected, Rep. Liz Cheney (R-WY) has been removed as chair of the House of Representatives' Republican Conference, the third highest-ranking Republican position in the House behind Minority Leader Kevin McCarthy (R-CA) and Minority Whip Steve Scalise (R-LA). The vote was not recorded and took place behind closed doors. Cheney had become a lightning rod for criticism within the powerful pro-Trump wing of GOP over her vote for impeachment of the former president in January and her subsequent comments refuting Trump's allegations that the 2020 election wasstolen by the Democrats. The move leaves few, if any, anti-Trump members within the GOP leadership ineither the House or the Senate, a situation that could result in the red carpet being rolled out for Trump to make another run at the White House in 2024 should he seek to do so.

CANADA (MNI): MNI spoke to a former BOC analyst about an indemnity deal between the central bank and the government covering any potential losses from selling bonds purchased under its QE program. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

U.K. (MNI): Delivering a statement to the House of Commons Prime Minister Boris Johnson confirms that a full independent public inquiry will be held into the gov'ts handling of the COVID-19 pandemic. Says that the appropriate time for the inquiry to begin would likely be inthe spring of 2022, with the hope then that the pandemic is over in the UK and there is not a threat posed by variants of the virus or a spike in cases of respiratory viruses in the winter of 2021/22.

BOE (MNI): Bank of England Governor Andrew Bailey said that while the financial system had, for the most part, withstood the Covid shock, money market funds had again proven to be a weak spot. Speaking at an ISDA conference he highlighted a fundamental weakness of these funds, which claim to be 'cash-like' vehicles but can't supply cash in a crisis.

ECB (MNI): Central banks could be sued for doing too little, too late on climate change, European Central Bank Executive Board member Frank Elderson said in an ECB podcast posted Wednesday, with the ECB's legal obligation to support the economic policies of the European Union necessarily extending to those underpinning the transition to a green economy.

DATA:

US Treasury Saw April Budget Deficit of USD226B

The Treasury Department Wednesday said the U.S. has racked up a USD1.9 trillion deficit in the first seven months of the fiscal year, with a USD226 billion deficit in the month of April.

The April federal budget deficit was a shift down from March's USD660 billion, when some of the Biden administration's USD1.9 trillion fiscal relief was dispersed. Receipts in April were USD439 billion, up USD197 billion, or 82%, compared to the year-ago month. Outlays were USD665 billion, down USD315 billion, or 32%, compared to April 2020.

The Treasury Department said the federal deficit in the first seven months of fiscal year 2021 was USD1.932 trillion, up USD450 billion compared with the deficit during the same period last year.

SNAPSHOT: Stocks And Bonds Slide, Dollar Higher

Below gives key levels of markets in late afternoon NY trade:

- DJIA down 597.94 points (-1.74%) at 33674.89

- S&P E-Mini Future down 81.5 points (-1.97%) at 4064.5

- Nasdaq down 347.1 points (-2.6%) at 13044.02

- US 10-Yr yield is up 5.9 bps at 1.6808%

- US Jun 10-Yr futures (TY) are down 14.5/32 at 132-0

- EURUSD down 0.0068 (-0.56%) at 1.208

- USDJPY up 0.93 (0.86%) at 109.55

- WTI Crude Oil (front-month) up $0.63 (0.97%) at $65.90

- Gold is down $16.39 (-0.89%) at $1820.85

Prior European bourses closing levels:

- EuroStoxx 50 up 1.37 points (0.03%) at 3947.43

- FTSE 100 up 56.64 points (0.82%) at 7004.63

- German DAX up 30.47 points (0.2%) at 15150.22

- French CAC 40 up 11.96 points (0.19%) at 6279.35

US TSYS SUMMARY: Curve Sharply Steeper On Record-Breaking CPI Print

Another busy day for Treasuries saw a record-breaking (vs expectations, and in some subcomponents) April inflation print pushing yields higher across the curve with little respite through the session.

- The curve initially flattened post-release, with 5s bearing most of the brunt (presumably on Fed hike path repricing); then this reversed as 5s losses stalled and the long end sell-off resumed. 10 Year yields flirted with 1.70%, yields rising 9+bps from pre-CPI.

- The 2-Yr yield is up 0.6bps at 0.1648%, 5-Yr is up 5.8bps at 0.8579%, 10-Yr is up 6.6bps at 1.688%, and 30-Yr is up 6.1bps at 2.4065%.

- Jun 10-Yr futures (TY) down 15.5/32 at 131-31 (L: 131-28.5 / H: 132-18) on the highest volumes since March (>2.3mn).

- Once again, no offsetting move in equities, which sold off alongside global bonds.

- Fed VC Clarida comments shortly after the data, that the Fed "won't hesitate to act" if inflation expectations become unanchored contributed to bearish sentiment.

- 1.3bps stop-through at the 10-Yr auction (1.684% high yield vs 1.697% when-issued) and best bid to cover (2.45x) since Jan 2021 auction helped temporarily stem the bleeding in 10s.

- The heavy data slate continues Thursday with weekly jobless claims and PPI.

USD LIBOR FIX - 12-05-2021

O/N 0.06000 (-0.00063)

1W 0.07250 (0.00125)

1M 0.09813 (0.00438)

2M 0.12850 (0.00137)

3M 0.15413 (-0.00612)

6M 0.19013 (-0.00087)

12M 0.26438 (-0.00075)

SOFR, Other Repo Rates Steady

| REPO REFERENCE RATES (rate, change from prev. day, volume): |

| * Secured Overnight Financing Rate (SOFR): 0.01%, no change, $865B |

| * Broad General Collateral Rate (BGCR): 0.01%, no change, $383B |

| * Tri-Party General Collateral Rate (TGCR): 0.01%, no change, $359B |

Fed Funds, OBFR Steady

| New York Fed EFFR for prior session (rate, chg from prev day): |

| * Daily Effective Fed Funds Rate: 0.06%, no change, volume: $66B |

| * Daily Overnight Bank Funding Rate: 0.05%, no change, volume: $271B |

NY Fed Operational Purchases

Accepts $1.735bn of 20-30Y Tsys, Total Submitted $5.384bn

- Next up is tomorrow's 1500ET Update of the Operational Purchase Schedule. Could be interesting if they make a technical "adjustment" incl to the pace of 20-Year / TIPS as previously flagged.

FOREX: US CPI Sparks Dollar Volatility, Weak Equities Prompt NZD & AUD Slump

- The huge beat in US CPI, rising 0.8% m/m, prompted immediate strength in the greenback as US 10-year yields soared back above 1.65%.

- Despite the initial bout of strength for the Dollar Index, in the region of 0.4%, a full retracement and sharp selling pressure actually led the DXY to make new lows on the session, with EURUSD firming from 1.2072 to fresh highs at 1.2152.

- As the dust settled following the data, the greenback gradually inched back higher throughout the session, to eventually make new highs once again, supported by continued pressure on global equity indices and higher US yields.

- The poor risk sentiment caused an extension of weakness for Aussie and Kiwi, currencies that were firmly in the red following the overnight Asia session. Additional dollar strength throughout US hours prompted losses in the region of 1.5% for AUDUSD and NZDUSD Wednesday.

- CAD remains the clear outlier and outperformer. Roughly unchanged on the day in the face of equity weakness and a surging greenback indicates the strong trend in play following the recent testing of multi-year highs. USDCAD briefly dipped below a major support level to new lows of 1.2046, representing the lowest level for the pair since 2015. The 1.2062 pivot support level will potentially either reinforce the current medium-term bear leg if breached or lead to a reversal if the support manages to contain CAD strength.

EGBs-GILTS CASH CLOSE: US CPI Sends Bund Ylds To 2-Yr Highs

A very busy Wednesday for the European FI space: Bunds and Gilts initially traded firmer, but then the biggest upside surprise in US inflation data history hammered global core FI in the afternoon.

- Curves bear steepened sharply, with Bund yields breaking the 2020 high of -0.1398% to levels not seen since 2019 (Gilts not far from the mid-March 2021 high just below 0.91%).

- Risk appetite recovered from early lows, with equities bouncing strongly, and periphery EGB spreads flat on the session.

- Earlier, UK GDP data surprised to the upside. Portugal sold E1.5bn of OTs.

- Thursday sees a quiet data schedule (some final CPIs); but busy on issuance, with E9.25bln of BTPs on offer, as well as Ireland selling E1.0-1.5bn of IGB. BOE's Bailey and Cunliffe, and ECB's Centeno appear.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 1.2bps at -0.656%, 5-Yr is up 3.1bps at -0.518%, 10-Yr is up 3.8bps at -0.123%, and 30-Yr is up 3.8bps at 0.446%.

- UK: The 2-Yr yield is up 4.1bps at 0.105%, 5-Yr is up 4.7bps at 0.402%, 10-Yr is up 5.3bps at 0.886%, and 30-Yr is up 3.7bps at 1.425%.

- Italian BTP spread unchanged at 114.7bps/ Spanish spread up 0.3bps at 68.5bps

EQUITIES: Stocks Slip as Inflation Fears Realized

- Equities markets fell sharply on the back of the largest surprise relative to expectations on record for the US CPI print, which rose 0.8% m/m and 0.9% for the core reading, realizing the market's concern that there will be a material spike in near-term inflation metrics.

- As such, the heavily sold sectors earlier in the week came under fire again, with consumer discretionary and tech firms the hardest hit. At the other end of the table, banks and financials had a firmer session, with the likes of Citi and Wells Fargo higher by 1%, enjoying the steeper US yield curve.

- Stock markets remained under pressure after the London close, with the e-mini S&P narrowing the gap with the 50-dma support of 4047.72. This level was last crossed on March 25th, but hasn't closed below since the early March stock weakness.- Consumer discretionary and tech names leading the decline, while bank stocks are holding up well.

COMMODITIES: Gold Sees Little Post-CPI Support as Firmer Greenback Weighs

- Oil benchmarks remained firm Wednesday as markets continued to lack any clarity of the resumption of capacity through the hacking-hit Colonial Pipeline, which kept gas prices elevated across the Southern US states, prompting further sporadic reports of panic buying and stockpiling of energy products.

- WTI crude futures rallied to touch $66.63, just shy of the May highs. A break and hold above that level of $66.76 would open the early March cycle highs and resume the multi-month uptrend.

- Gold faltered under the weight of a rallying greenback Wednesday, shrugging off any support that may have stemmed from the surging inflation rate in the US. Prices managed to hold above the week's low of $1818.13, however, which remains the first key support.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.