Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI REALITY CHECK: High Prices No Drag on US Retail Spending

- MNI BRIEF: NY Fed Shifts Bond Buys to 7-30Yrs, Away from TIPS

- MNI BRIEF: Fed Advisor Warns Price Expectations Could Rise

- Dallas Fed BARKIN "U.S. RECOVERY OUTPACED MOST OF REST OF THE WORLD," Bbg

- BARKIN: SPENDING HAS COME BACK FASTER THAN EMPLOYMENT, Bbg

- BARKIN: HOPEFUL THAT WE'RE ON BRINK OF COMPLETING THE RECOVERY, Bbg

- BLACKROCK'S RIEDER THINKS WE NEED TO TAPER: CNBC

US TSY SUMMARY:

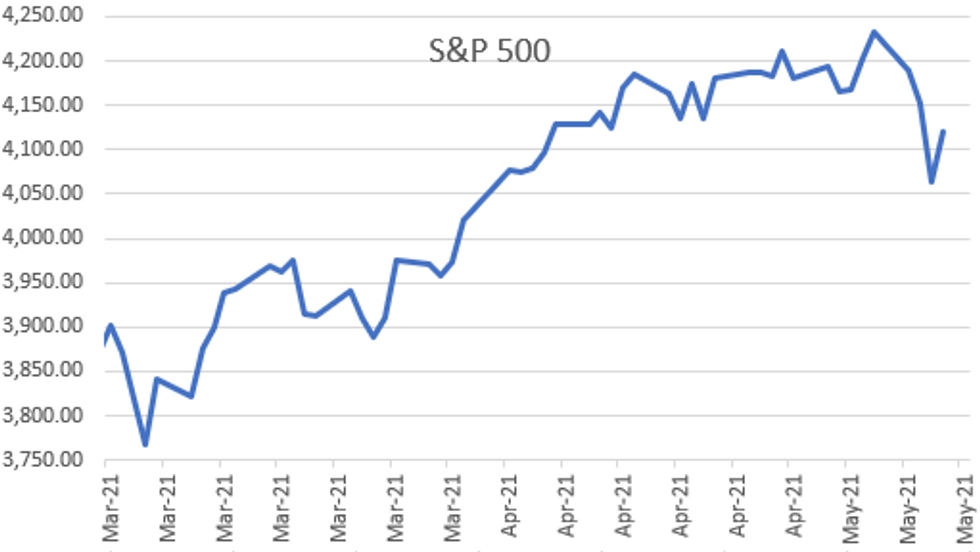

Rates finish stronger, holding narrow second half range after making session highs around noon time, robust volumes, TYM1 near 1.6m late. Equities stronger, but off early Monday all-time highs (ESM1 +63.0 after NY FI close.

- Post-Data Chop in Rates and Equities: Tsys and equities dropped post data -- PPI +0.6% vs. +0.3% est, weekly claims fall to 473k vs. 490k est, continuing claims more or less in-line -- then quickly bounce back near opening levels.

- Final leg of Tsy supply: $27B 30Y auction -- Tsys Gapped Lower on Weak 30Y, 1.8Bp Tail. US Tsy $27B 30Y bond auction (912810SX7) drew 2.395% high yield (2.320% last month) vs. 2.377% WI; w/ 2.22 bid/cover (2.47 prior). Indirects drew 59.88% vs. 60.96% prior, 20.06% directs vs. 21.95%, and 20.05% for dealers vs. 17.09% prior.

- VIX pared gains after run through 200-day moving avg: CBOT VIX pared gains, currently -4.76 at 22.83 vs. an overnight high of 28.93.

- The vol index blew through 50- and 200-day moving average yesterday on a run to 28.38 (Early March levels).

- The 2-Yr yield is down 0.6bps at 0.1569%, 5-Yr is down 3.1bps at 0.8321%, 10-Yr is down 2.9bps at 1.6625%, and 30-Yr is down 1.8bps at 2.3931%.

US

FED: Near term inflationary pressures including supply chain issues could soon start to put upward pressure on longer term inflation expectations in the U.S., Atlanta Fed policy adviser Brent Meyer told MNI on Wednesday. Meyer warned a temporary build-up in pressures could soon become an issue and his main concern now is if firms "misinterpret" price changes as something more permanent.

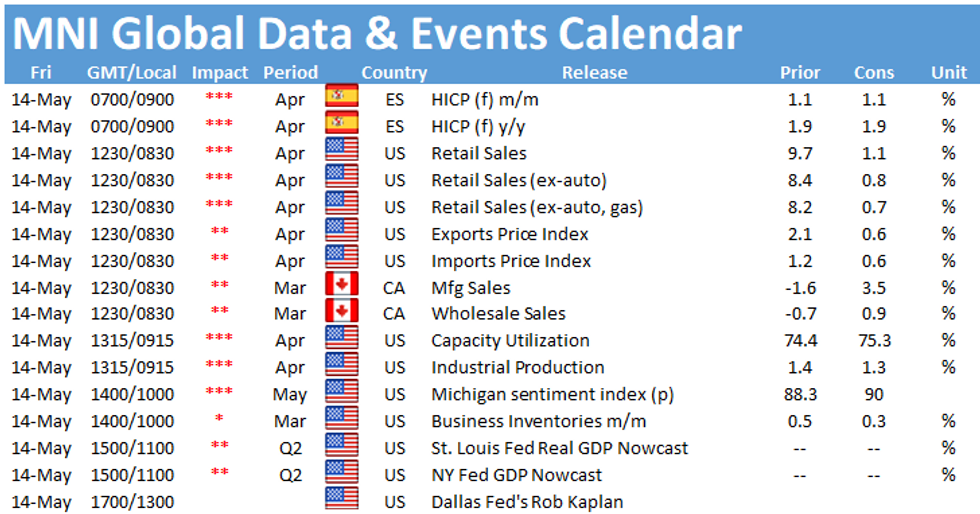

US: U.S. April retail sales growth likely slowed over March as reopenings and vaccinations tapered, industry experts told MNI, although more fiscal relief and tax refunds mean higher prices for goods won't be a drag on spending.

- "I'm expecting that we'll see another solid month" of spending, said Jack Kleinhenz, chief economist at the National Retail Federation, noting that the ability to spend improved through the month, with stimulus money in "full force" and tax refunds on the way, however delayed.

- April spending intentions improved over March, Kleinhenz said, citing data from the NRF, with 46% of consumers surveyed by the trade group saying they felt comfortable shopping in stores because of widespread vaccine availability. Another 40% said they felt comfortable going to bars and restaurants and 35% said they're willing to travel and go on vacation, he said.

OVERNIGHT DATA

- US APR FINAL DEMAND PPI +0.6%, EX FOOD, ENERGY +0.7%

- US APR FINAL DEMAND PPI EX FOOD, ENERGY, TRADE SERVICES +0.7%

- US APR FINAL DEMAND PPI Y/Y +6.2%, EX FOOD, ENERGY Y/Y +4.1%

- US APR PPI: FOOD +2.1%; ENERGY -2.4%

- US APR PPI: GOODS +0.6%; SERVICES +0.6%; TRADE SERVICES +0.5%

- US JOBLESS CLAIMS -34K TO 473K IN MAY 08 WK

- US PREV JOBLESS CLAIMS REVISED TO 507K IN MAY 01 WK

- US CONTINUING CLAIMS -0.045M to 3.655M IN MAY 01 WK

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 513.57 points (1.53%) at 34100.29

- S&P E-Mini Future up 57.25 points (1.41%) at 4115

- Nasdaq up 114.6 points (0.9%) at 13146.36

- US 10-Yr yield is down 2.9 bps at 1.6625%

- US Jun 10Y are up 9.5/32 at 132-7

- EURUSD up 0.0005 (0.04%) at 1.2077

- USDJPY down 0.23 (-0.21%) at 109.43

- WTI Crude Oil (front-month) down $2.45 (-3.71%) at $63.68

- Gold is up $10.17 (0.56%) at $1825.67

- EuroStoxx 50 up 5.02 points (0.13%) at 3952.45

- FTSE 100 down 41.3 points (-0.59%) at 6963.33

- German DAX up 49.46 points (0.33%) at 15199.68

- French CAC 40 up 8.98 points (0.14%) at 6288.33

US TSY FUTURES CLOSE:

- 3M10Y -1.638, 165.492 (L: 164.297 / H: 168.577)

- 2Y10Y -1.606, 150.868 (L: 149.474 / H: 154.061)

- 2Y30Y +0.002, 224.527 (L: 221.759 / H: 225.4)

- 5Y30Y +1.709, 156.319 (L: 153.115 / H: 157.042)

- Current futures levels:

- Jun 2Y up 0.5/32 at 110-12.5 (L: 110-12 / H: 110-12.87)

- Jun 5Y up 4/32 at 124-3 (L: 123-30.25 / H: 124-05)

- Jun 10Y up 8/32 at 132-5.5 (L: 131-27 / H: 132-09)

- Jun 30Y up 14/32 at 156-1 (L: 155-14 / H: 156-13)

- Jun Ultra 30Y up 15/32 at 182-16 (L: 181-26 / H: 183-11)

US EURODOLLAR FUTURES CLOSE

- Jun 21 +0.005 at 99.840

- Sep 21 +0.005 at 99.830

- Dec 21 +0.010 at 99.785

- Mar 22 +0.010 at 99.80

- Red Pack (Jun 22-Mar 23) +0.010 to +0.020

- Green Pack (Jun 23-Mar 24) +0.030 to +0.040

- Blue Pack (Jun 24-Mar 25) +0.045 to +0.055

- Gold Pack (Jun 25-Mar 26) +0.050 to +0.060

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N +0.00225 at 0.06225% (-0.00188/wk)

- 1 Month +0.00275 to 0.10088% (-0.00050/wk)

- 3 Month +0.00175 to 0.15588% (-0.00400/wk) ** (vs. Record Low 0.15413% on 5/12)

- 6 Month +0.00250 to 0.19263% (-0.00012/wk)

- 1 Year -0.00025 to 0.26463% (-0.00637/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $67B

- Daily Overnight Bank Funding Rate: 0.05% volume: $253B

- Secured Overnight Financing Rate (SOFR): 0.01%, $895B

- Broad General Collateral Rate (BGCR): 0.01%, $378B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $352B

- (rate, volume levels reflect prior session)

New Buckets: 7-10Y, 10Y-22.5Y, 22.5Y-30Y as the Desk plans to purchase approximately $80 billion over the monthly period from 5/14/21 to 6/11/21:

- Fri 5/14 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Mon 5/17 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Tue 5/18 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 5/19 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 5/20 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 5/21 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

PIPELINE: Slow Finish After Heavy Start to Wk

- Date $MM Issuer (Priced *, Launch #)

- 05/13 $1.85B #JP Morgan PerpNC5 $25par pfd, 4.625%

- 05/13 $1.5B #Arthur J Gallagher $650M 10Y +90, $850M 30Y +115

- 05/13 $1.45B #Goodyear $850M 8Y 5%, $600M 10Y 5.25%

- 05/13 $750M #Vornado Realty 00M $5Y +135, $350M 10Y +180

EGBs-GILTS CASH CLOSE: Inflation Fears Fade...For Now

Bunds and Gilts clawed back early sharp losses from around midday London time onward, with yields ultimately closing up but well off highs.

- This came against a backdrop of recovering equities, with US Data still inflationary (high PPI, low jobless claims) but not nearly the level of surprise of Wednesday's CPI, which fuelled the selloff.

- Curves have faded their steepening bias to trade fairly flat on the session.

- EGB periphery spreads mostly wider, Italy 3.0bps wider. Supply may have been a factor; Italy sold E9.25bln of BTPs; Ireland sold E1.5bln of IGBs).

- Ascension Day holiday in several countries (France, Germany, Netherlands and others) meant little data today.

- Friday sees little data (Spain final Apr CPI), and the ECB April meeting accounts.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.2bps at -0.658%, 5-Yr is up 0.6bps at -0.512%, 10-Yr is up 0.3bps at -0.12%, and 30-Yr is down 0.9bps at 0.437%.

- UK: The 2-Yr yield is down 0.2bps at 0.103%, 5-Yr is up 0.7bps at 0.409%, 10-Yr is up 1.2bps at 0.898%, and 30-Yr is up 1.3bps at 1.438%.

- Italian BTP spread up 3bps at 117.7bps / Spanish spread up 2.1bps at 70.6bps

FOREX: US Dollar Unphased By Bounce In Equities, USDCAD Rebounds

- G10 currencies took a back seat on Thursday as global equity indices staged a recovery during the US session. Dollar indices remain in marginal positive territory as the greenback struggled to pick a direction. G10 ranges remained fairly subdued while larger moves were seen in the EM space with the likes of MXN and RUB rising close to 1%.

- CHF led gains, appreciating ~0.3% against both the EUR and the USD. NZDUSD also higher, advancing 0.25% to 0.7175 as of writing, with mildly firmer risk sentiment propping the kiwi off its lows. Despite the minor gains, the pair still resides down 1.5% since the start of the week.

- USDCAD has had a fairly strong bounce after failing to break through multi-year support on Wednesday. Risk-off prompted the initial bounce back above noted pivot support at 1.2062. The level has recently been flagged as potentially reinforcing the current medium-term bear leg if breached or lead to a reversal if the support manages to contain CAD strength.

- CAD weakness was exacerbated by comments from the Bank of Canada. Governor Tiff Macklem, in a press conference, said that a further appreciation of the Canadian dollar would create risk for the bank's outlook. While nothing entirely new, USDCAD took another leg higher towards then end of the session to briefly print above 1.22 (+0.54%).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.