Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Williams Favors Fed QE Taper Completion Before Rate Hikes

- MNI BRIEF: Fed's Williams- AIT Won't Cause Sharp Rate Reversal

- MNI BRIEF: NY Fed: 1-Yr Inflation Expectations Jump to 4.8%

- WILLIAMS: DELTA VARIANT FEARS MAY BE FACTOR BEHIND LOWER YIELDS, Bbg

- KASHKARI: I'M IN THE CAMP THAT INFLATION IS TRANSITORY, Bbg

- MNI: Canada Names Carolyn Rogers From BIS as New BOC Deputy

US

FED: New York Fed President John Williams Monday said he prefers seeing an end to the process of drawing back on asset purchases before raising short-term interest rates.

- "My own view is the simplest, natural way is to first do a taper or finish that then think about liftoff," he said. "That does seem to me the most straightforward way to do it and to communicate what we're doing."

- "I do think we have some flexibility to avoid" an overlap of QE taper and interest rate hikes at the same time, Williams told reporters after a speech to a Bank of Israel and Center for Economic and Policy Research conference. For more see MNI Policy main wire at 1131ET.

FED: New York Fed President John Williams said Monday theoretical models suggest the central bank's average inflation targeting framework should not induce a sharp rise in interest rates to counter inflation.

- In a high-level theoretical overview of average inflation targeting, Williams said there is "no predictable pattern of sharp reversals or large overshooting of policy rates relative to neutral, either for static or dynamic AIT policies." Williams, speaking at a Bank of Israel/Centre for Economic Policy Research conference, said the rebound to the neutral rate may be larger under average inflation targeting but it should be gradual.

- Median inflation expectations three years out remained unchanged at 3.6%, the New York Fed said. The increase in the year-ahead measure was driven by respondents who have some college education but measures of disagreement across respondents reached new series' highs at both year-ahead and three-year-ahead horizons, the Survey of Consumer Expectations showed.

- The survey also showed households' labor market expectations continued to improve as the mean perceived probability of losing one's job in the next 12 months decreased from 12.6% to 10.9%, reaching a new series' low, and the mean perceived probability of finding a job in the next three months increased by 0.2 percentage point to 54.2%, the highest reading since February 2020.

CANADA

BOC: Canada named Carolyn Rogers as the top deputy of its central bank on Monday, bringing home a veteran of the country's banking supervisor who had been working at the Bank for International Settlements to fill a spot that had been vacant since December.

- Rogers won't start until Dec. 15, meaning the position will be unfilled for a year after the departure of Carolyn Wilkins. The governor and senior deputy are recommended by the BOC's outside board of directors and approved by the finance minister for seven-year terms.

- "I am confident that, in addition to her exceptional resume, Ms. Rogers will bring a fresh perspective to the Bank of Canada," Finance Minister Chrystia Freeland said in a statement.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 123.22 points (0.35%) at 34993.6

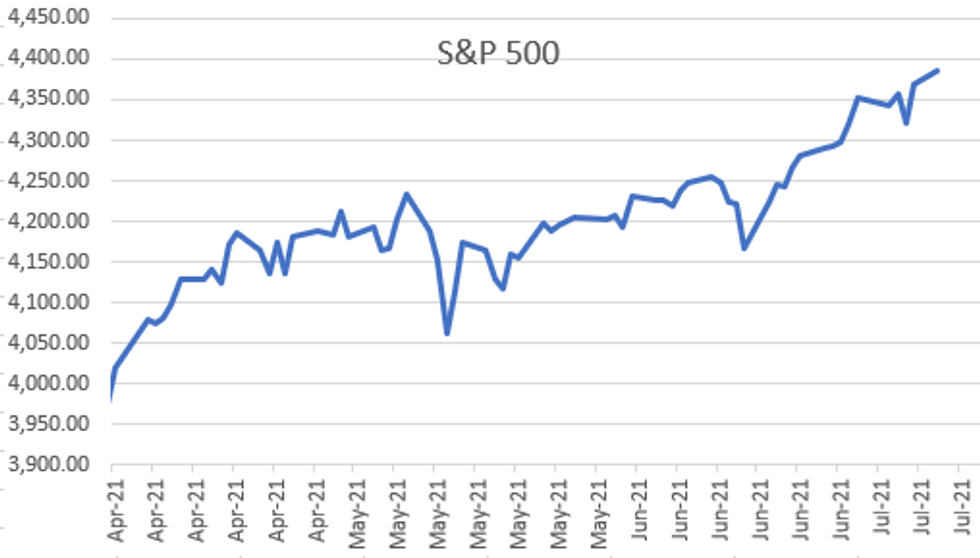

- S&P E-Mini Future up 15.5 points (0.36%) at 4375.25

- Nasdaq up 26.8 points (0.2%) at 14728.5

- US 10-Yr yield is up 0.8 bps at 1.3678%

- US Sep 10Y are down 2/32 at 133-11.5

- EURUSD down 0.0019 (-0.16%) at 1.1857

- USDJPY up 0.22 (0.2%) at 110.36

- WTI Crude Oil (front-month) down $0.31 (-0.42%) at $74.25

- Gold is down $2.2 (-0.12%) at $1806.22

European bourses closing levels:

- EuroStoxx 50 up 25.29 points (0.62%) at 4093.38

- FTSE 100 up 3.54 points (0.05%) at 7125.42

- German DAX up 102.58 points (0.65%) at 15790.51

- French CAC 40 up 29.83 points (0.46%) at 6559.25

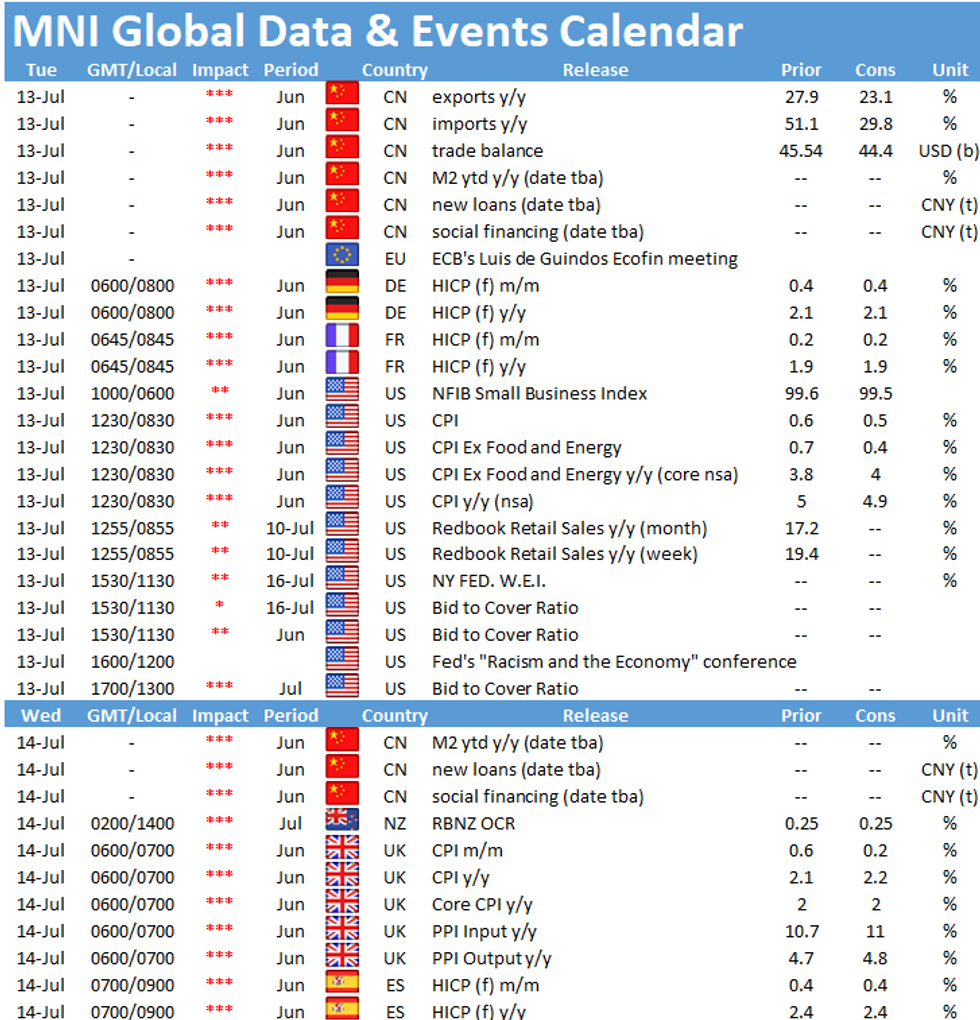

US TSY SUMMARY: FI Support Evaporates, Focus on Tue' CPI

Markets grew quiet over the last hour into the NY FI close, reversing opening levels w/ equities near session highs, Tsys mildly weaker after the bell. No data Monday,

focus on Tue' June CPI: MoM (0.6%, 0.5%); Ex Food and Energy MoM (0.7%, 0.4%).

- Markets did have comments from NY Fed Williams and MN Fed Kashkari to digest. Williams' straightforward "view is the simplest, natural way is to first do a taper or finish that then think about liftoff." Kashkari sees current inflation metrics as transitory.

- Mirroring EGBs, Tsys opened moderately firmer/off late overnight highs, support evaporating by midday. Sources reported carry-over selling in intermediates to long end from Asian real$ accts, pre-auction short sets ahead todays 3Y and 10Y R/O note auctions. US Tsy auction's $24B 30Y Bond re-open Tuesday.

- 3Y note auction tailed: Tsys inched lower after $58B 3Y note auction (91282CCL3) tails: 0.426% high yield vs. 0.422% WI; 2.41x bid-to-cover off 2.46x 5 auction avg. Tsys bounce off lows after $38B 10Y note auction re-open (91282CCB5) trades through: 1.371% high yield vs. 1.375% WI; 2.39x bid-to-cover off 2.43x 5 auction avg.

- Dealers waited until after the Tsy 10Y R/O to launch larger than some had anticipated $6B MUFG 3-parter.

- The 2-Yr yield is up 1.8bps at 0.2307%, 5-Yr is up 1.4bps at 0.7994%, 10-Yr is up 0.8bps at 1.3678%, and 30-Yr is up 0.9bps at 1.9982%.

US TSY FUTURES CLOSE

- 3M10Y +0.58, 131.714 (L: 126.846 / H: 132.386)

- 2Y10Y -0.777, 113.516 (L: 111.718 / H: 114.324)

- 2Y30Y -0.684, 176.551 (L: 174.263 / H: 177.369)

- 5Y30Y -0.513, 119.718 (L: 117.915 / H: 120.392)

- Current futures levels:

- Sep 2Y down 1.25/32 at 110-6.5 (L: 110-06.25 / H: 110-08.5)

- Sep 5Y down 2.25/32 at 123-27.5 (L: 123-25.5 / H: 124-01.25)

- Sep 10Y down 2/32 at 133-11.5 (L: 133-08.5 / H: 133-20.5)

- Sep 30Y down 9/32 at 162-11 (L: 162-09 / H: 163-07)

- Sep Ultra 30Y down 22/32 at 195-11 (L: 195-08 / H: 197-05)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.005 at 99.875

- Dec 21 -0.005 at 99.80

- Mar 22 -0.005 at 99.810

- Jun 22 -0.010 at 99.745

- Red Pack (Sep 22-Jun 23) -0.02 to -0.015

- Green Pack (Sep 23-Jun 24) -0.015

- Blue Pack (Sep 24-Jun 25) -0.01 to -0.005

- Gold Pack (Sep 25-Jun 26) -0.005

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00012 at 0.08675% (+0.00613 total last wk)

- 1 Month -0.00438 to 0.09575% (-0.00275 total last wk)

- 3 Month +0.00425 to 0.13288% (-0.00925 total last wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00338 to 0.15438% (-0.01200 total last wk)

- 1 Year +0.00562 to 0.24450% (-0.00563 total last wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $75B

- Daily Overnight Bank Funding Rate: 0.08% volume: $257B

- Secured Overnight Financing Rate (SOFR): 0.05%, $911B

- Broad General Collateral Rate (BGCR): 0.05%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $330B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.001B accepted vs. $3.931B submission

- Next scheduled purchases:

- Tue 7/13 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Wed 7/14 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Wed 7/14 1500ET Update NY Fed Operational Purchase Schedule

FED: Reverse Repo Operations

NY Fed reverse repo usage recedes to $776.472B from 70 counterparties vs. $780.596B on Friday. Compares to June 30 record high of $991.939B.

PIPELINE: $6B MUFG 3Pt Launched

Dealers waited until after the Tsy 10Y R/O to launch larger than some had anticipated $6B MUFG 3-parter. Note, BC and IADB expected to launch Tuesday.- Date $MM Issuer (Priced *, Launch #)

- 07/12 $6B #MUFG (Mitsubishi UFF Fncl Grp) $2.1B 4NC3 +55, $2.1B 6NC5 +75, $1.8B 11NC10 +95

- On tap:

- 07/13 $Benchmark Province of British Columbia 5Y +6a

- 07/13 $Benchmark IADB 7Y sustainable development bond

- 07/?? $870M Uzbekistan 10Y 4.25%a (includes UZS 3Y)

EGBs-GILTS CASH CLOSE: Rally Fades With Supply Eyed

The Bund and Gilt curves bull flattened Monday, but yields ended well above the session's lowest levels as equities rebounded. Large supply and US CPI Tuesday also presenting some near-term risk.

- Tuesday will see big issuance: E30bln in euro-denominated supply (including EU syndication), and GBP6bln in 2039 Gilt syndication. Not to mention large US supply today/Tuesday.

- Periphery spreads tightened; Italy 10-Yr spreads have retraced most of last week's widening.

- As expected, the UK authorities announced they were going ahead with plans to end COVID-19 restrictions in England on 19 July.

- Otherwise, no bond supply today and nothing new from ECB speakers.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.4bps at -0.672%, 5-Yr is down 0.2bps at -0.598%, 10-Yr is down 0.2bps at -0.295%, and 30-Yr is down 0.1bps at 0.205%.

- UK: The 2-Yr yield is up 0.7bps at 0.094%, 5-Yr is up 0.1bps at 0.296%, 10-Yr is down 0.4bps at 0.651%, and 30-Yr is down 1.5bps at 1.158%.

- Italian BTP spread down 2.3bps at 103.3bps / Spanish down 1.1bps at 63.6bps

FOREX: G10 FX Holds Narrow Ranges Ahead Of US CPI Data

- Major currency pairs lacked conviction on Monday, as the dollar index made marginal gains, up 0.15%, heading into important US inflation data on Tuesday.

- Despite equity indices resuming their incline, NZD was the Monday laggard, falling 0.3%. Greater weakness had been seen during the European session, with NZDUSD reaching 0.6948 before recovering to 0.6980 as of writing.

- Smaller losses were also seen in EUR, JPY, GBP, AUD and CAD of around 0.15%.

- USDJPY printed a high of 110.40 which was the notable breakdown level last week. What appeared to be strong follow through on July 8th (low of 109.53) has been gradually unwound over the past two trading days. Despite the 110.40 level capping price action today, USDJPY remains well bid, hovering just six pips shy of those best levels.

- More notable moves in the EM space, with strong divergence between high beta currencies. BRL firmed 1.5% following a strong period of weakness, whereas ZAR came under significant pressure following a rapid escalation of pro-Zuma protests and violence.

- The focus tomorrow is firmly on the US June CPI data where the annual headline is expected to dip to 4.9% from 5.0% in May. Later on Tuesday, Fed's Bostic (2021 voter) is due to deliver opening remarks at a webinar presented by all 12 District Banks of the Federal Reserve System.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.