Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI EXCLUSIVE: Patience Warranted as Inflation to Ease -Ex-Fed Economists

- MNI INTERVIEW: EU Debt Talks After German Vote-Italy's Letta

- FED: Plenty To Talk About On Taper

- TSY SEC YELLEN: TREASURY WILL START SPECIAL MEASURES DUE TO DEBT LIMIT, Bbg

US

FED: The prospect of softer inflation readings over coming months and into early next year, reflected in a recent plunge in long-term bond yields, will likely give Federal Reserve officials greater room to wait for stronger employment growth before tightening policy, ex-Fed board economists told MNI.

- Investors focused on a short-run spike in inflation may have missed a coming turning point, according to these staffers, whose views closely match those of Fed Chair Jerome Powell. Last week, Powell suggested policymakers need at least six more months to properly interpret data muddied by comparisons to the depths of Covid and by shifting labor market and supply chain trends.

- "Inflation went faster to where we thought it was going to peak, and if that's the case, it can come down faster than we thought," Claudia Sahm, former Fed board economist and forecaster, said in an interview. "You could get (CPI) inflation back down to 3% by the end of the year, and start settling in at 2% by the middle of next year." For more see MNI Policy main wire at 1113ET.

- The July 27-28 FOMC meeting is very unlikely to culminate in a taper announcement, but September is a distinct possibility. In any case, the debate over slowing and stopping net asset purchases will continue at the July meeting, and will be multifaceted: the timing, pace, composition, and end-point are all contentious areas.

- On timing: Multiple regional Fed presidents are advocating a reduction in asset purchases soon, but most FOMC members want to see more "substantial further progress" on the labor market front., with Chair Powell saying that is "still a ways off". Markets continue to expect a taper to begin early in 2021.

- On pace: While the prevailing consensus is that the current $120B/monthly in purchases would be tapered by an average $10B a month over the course of a year (or divided up $15B over 8 FOMC meetings), this has been one of the least openly-debated aspects among the current FOMC. But ex-Fed officials told MNI that the uncertainty in emerging from the pandemic means the Fed is likely to be open to adjusting the pace if their fundamental view of the outlook changes.

- On composition: Regional presidents and Gov Waller have suggested tapering MBS earlier or more quickly than Treasuries, in part because house price gains have been very strong. But Powell and NY Fed Pres Williams have been lukewarm about the idea, noting that MBS buys impact broader financial conditions in a manner similar to Tsy purchases. Other members have concurred, and/or see a shift on MBS as confusing the Fed's messaging and not worth the risk.

EUROPE

EU: The European Union should wait until after Germany's elections in September before launching a discussion aimed at expanding limits on national borrowing in the bloc's Stability and Growth Pact, the leader of a key party in Italy's governing coalition, former prime minister Enrico Letta, told MNI

- The head of the centre-left Democratic Party also called for the joint eurozone fiscal capacity harnessed by the EUR750 billion Next Generation EU programme to be made permanent, but added in an interview that big beneficiaries such as Italy and Spain will have to make good use of the cash in order to convince countries such as Germany to agree. For more see MNI Policy main wire at 1054ET.

OVERNIGHT DATA

- U.S. IHS MARKIT JULY SERVICES PMI AT 59.8 VS 64.6 LAST MONTH

- U.S. IHS MARKIT JULY MANUFACTURING PMI AT 63.1 VS 62.1 PRIOR

- U.S. IHS MARKIT JULY COMPOSITE PMI AT 59.7 VS 63.7 PRIOR

- CANADIAN FLASH JUNE RETAIL SALES +4.4% MOM

- CANADIAN MAY RETAIL SALES -2.1%; SALES EX-AUTOS/PARTS -2.0%

- CANADA MAY RETAIL SALES EX-AUTOS/PARTS-GASOLINE -2.4%

- CANADA FLASH JUNE WHOLESALE SALES -2.0% MOM

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 196.45 points (0.56%) at 35021.15

- S&P E-Mini Future up 40.5 points (0.93%) at 4400.25

- Nasdaq up 140 points (1%) at 14824.46

- US 10-Yr yield is up 0.5 bps at 1.283%

- US Sep 10Y are down 3/32 at 134-5

- EURUSD up 0.0002 (0.02%) at 1.1773

- USDJPY up 0.39 (0.35%) at 110.53

- Gold is down $4.99 (-0.28%) at $1801.96

European bourses closing levels:

- EuroStoxx 50 up 50.05 points (1.23%) at 4109.1

- FTSE 100 up 59.28 points (0.85%) at 7027.58

- German DAX up 154.75 points (1%) at 15669.29

- French CAC 40 up 87.23 points (1.35%) at 6568.82

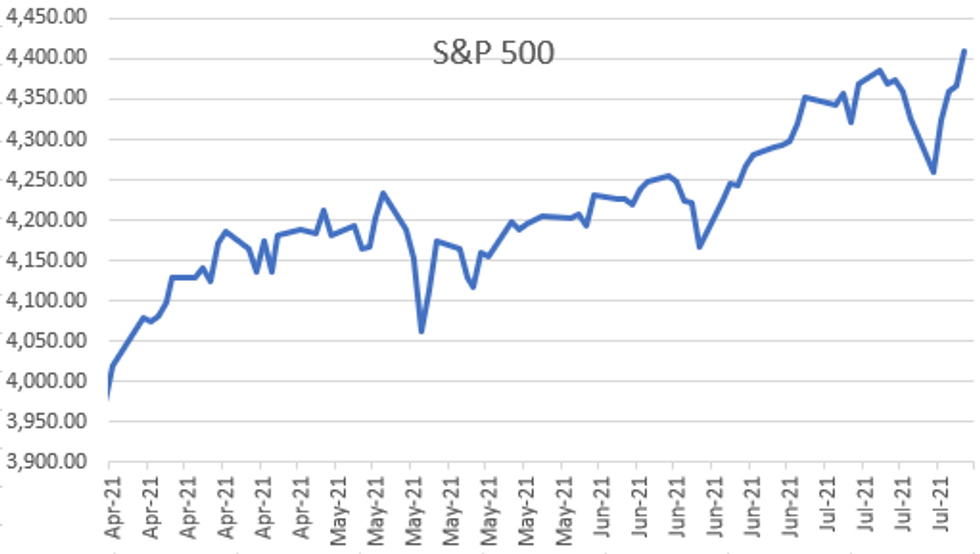

US TSY SUMMARY: What a Short, Strange Trip It's Been

After risk-off rout that sent 30YY to 1.7781% five month lows earlier in week, rates reversed in the second half of week as equities climbed to new all-time highs (ESU1 over 4406.0 after the FI close) had 30YY back to 1.9484% Friday after climbing to 1.9649% high Wed.- Sep 30Y futures (USU1) traded down to 163-14 by midmorning -- see-sawed to middle of session range at 164-00 by the close albeit on light summer volumes. Generally quiet -- sights set on next week's FOMC on Wed, Q2 GDP, Tsy supply (2-, 5- and 7Y notes), and a slew of equity earnings.

- Meanwhile, the statutory debt limit suspension expires Saturday, July 31. Tsy Sec Yellen in a note to Congress said "If Congress has not acted to suspend or increase the debt limit by Monday, August 2, 2021, Treasury will need to start taking certain additional extraordinary measures in order to prevent the United States from defaulting on its obligations."

- The 2-Yr yield is up 0bps at 0.2001%, 5-Yr is down 0.4bps at 0.715%, 10-Yr is up 0.5bps at 1.283%, and 30-Yr is up 0.4bps at 1.9203%.

MONTH-END EXTENSIONS: Preliminary Barclays/Bbg Extension Estimates for US

Preliminary forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.16Y; US Gov infl-linked 0.23Y.

| SECURITY | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.08 | 0.09 | 0.09 |

| Agencies | 0.06 | 0.04 | 0.05 |

| Credit | 0.06 | 0.12 | 0.08 |

| Govt/Credit | 0.07 | 0.1 | 0.08 |

| MBS | 0.08 | 0.07 | 0.06 |

| Aggregate | 0.07 | 0.09 | 0.08 |

| Long Gov/Cr | 0.05 | 0.09 | 0.07 |

| Iterm Credit | 0.06 | 0.1 | 0.08 |

| Interm Gov | 0.08 | 0.08 | 0.08 |

| Interm Gov/Cr | 0.07 | 0.09 | 0.08 |

| High Yield | 0.06 | 0.11 | 0.1 |

US TSY FUTURES CLOSE

- 3M10Y +0.06, 122.816 (L: 121.666 / H: 126.164)

- 2Y10Y -0.226, 107.42 (L: 106.142 / H: 110.768)

- 2Y30Y -0.106, 171.297 (L: 170.103 / H: 174.625)

- 5Y30Y +0.691, 120.169 (L: 118.746 / H: 122.073)

- Current futures levels:

- Sep 2Y steady at at 110-8.875 (L: 110-08.5 / H: 110-09.375)

- Sep 5Y down 1/32 at 124-9.25 (L: 124-06.25 / H: 124-11.25)

- Sep 10Y down 3.5/32 at 134-4.5 (L: 133-30 / H: 134-07)

- Sep 30Y down 15/32 at 164-1 (L: 163-14 / H: 164-12)

- Sep Ultra 30Y down 30/32 at 198-11 (L: 197-12 / H: 199-01)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.005 at 99.870

- Dec 21 +0.005 at 99.815

- Mar 22 steady at 99.825

- Jun 22 steady at 99.775

- Red Pack (Sep 22-Jun 23) -0.005 to steady

- Green Pack (Sep 23-Jun 24) -0.01 to -0.005

- Blue Pack (Sep 24-Jun 25) -0.015 to -0.01

- Gold Pack (Sep 25-Jun 26) -0.015

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00325 at 0.08013% (-0.00562/wk)

- 1 Month -0.00312 to 0.08613% (+0.00250/wk)

- 3 Month +0.00363 to 0.12888% (-0.00537/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00125 to 0.15850% (+0.00637/wk)

- 1 Year -0.00262 to 0.24138% (-0.00075/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $71B

- Daily Overnight Bank Funding Rate: 0.08% volume: $255B

- Secured Overnight Financing Rate (SOFR): 0.05%, $849B

- Broad General Collateral Rate (BGCR): 0.05%, $371B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $339B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $6.001B accepted vs. $18.151B submission

- Next scheduled purchases

- Mon 7/26 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Tue 7/27 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Wed 7/28 No buy-operation scheduled due to FOMC

- Thu 7/29 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 7/30 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

FED: Reverse Repo Operation

NY Fed reverse repo usage dips to $877.251B from 76 counterparties vs. $898.197B on Thursday (compares to June 30 record high of $991.939B).

PIPELINE: $3.75B Chile 3Pt Lead Thu's Issuance

- Date $MM Issuer (Priced *, Launch #)

- 07/23 No new issuance Friday after $30.65B priced Mon-Thu

- $9.45B Priced Thursday

- 07/22 $3.75B *Rep of Chile $2.25B 12Y +130, $1B 20Y +130, $500M 40Y +140

- 07/22 $2.3B *DirecTV 6NC2 5.875%

- 07/22 $2B *JP Morgan PerpNC5 4.2%

- 07/22 $900M *World Bank 2031 tap FRN/SOFR +34

- 07/22 $500M *Ukraine 6.876% 2029 Tap 6.3%

EGBs-GILTS CASH CLOSE: Peripheries Impress As ECB Hawks Explain Dissents

The German and UK curves finished a busy week on a fairly flat note, though notably yields ended well below intraday highs. Periphery spreads narrowed, with risk appetite gaining (equities stronger).

- Friday's ECB talk was all about the hawkish dissenting voices: Weidmann and Wunsch explaining why they objected to the new policy guidance.

- Flash July PMI data were mixed, while still pointing to a sustained expansion in economic activity. Germany surprised higher, France was a touch weaker than expected and the UK posted a significant miss. Earlier, UK retail sales figures were broadly better than expected.

- The German PMI beat sent Bunds much lower initially, but the move soon reversed.

- After hours Friday sees ratings reviews: Moody's on Cyprus and DBRS on EFSF, ESM.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at -0.726%, 5-Yr is down 0.2bps at -0.704%, 10-Yr is up 0.6bps at -0.42%, and 30-Yr is up 0.8bps at 0.061%.

- UK: The 2-Yr yield is up 1bps at 0.079%, 5-Yr is up 1.3bps at 0.279%, 10-Yr is up 1.8bps at 0.584%, and 30-Yr is up 0.3bps at 1.005%.

- Italian BTP spread down 2.5bps at 103.8bps / Spanish down 2.1bps at 69.1bps

FOREX: JPY Weakness Continues As Equities Extend Recovery

- G10 FX held extremely narrow ranges on Friday as markets continued to recover from Monday's bout of risk-off sentiment that prompted a volatile burst for currency markets to start the week.

- The Japanese Yen posted the biggest retreat in the final session of the week, with USDJPY (+0.35) edging higher above 110.50. Spot trades just shy of the July 14 highs at 110.70 which is considered firm resistance following the recent bearish technical developments for the pair.

- The New Zealand Dollar was a relative outperformer, marginally firming +0.14%, whereas small losses were exhibited in GBP, AUD and CAD resulting in the dollar index a touch higher on the day.

- The biggest move came in the South African Rand (-1.03%) following an extension of yesterday's weakness after the central bank meeting. The statement included a reduction of 2021 growth and 2022 average CPI forecasts, weighing on ZAR.

- The Dollar index rise marks the seventh weekly gain over the past 9 weeks, likely to post the second highest close for 2021. The year's highs reside at 93.44 and become the next logical reference point for the index.

- EURUSD closes less than 20 pips above the week's lows of 1.1752. Despite underwhelming markets, the first ECB meeting since the strategy review marked a slight dovish shift. Markets will place focus on the 1.1704 April lows which may potentially trigger a deeper pullback for the pair.

- A fairly quiet start to kick off next week with Monday featuring German IFO data and a speech from Bank of England's Vlieghe on demographics, debt, and distribution of income.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.