Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- University of Michigan Consumer Sentiment Aug 70.2 (81.2 Exp, 81.2 Prior)

- MNI BRIEF: Higher Prices to Stay for Years - Philly Fed Survey

- MNI: Trudeau Calls Snap Canada Election For Sept 20

US

FED: The Philadelphia Fed's Survey of Professional Forecasters predicts PCE inflation at 4.1% and core at 3.7% in 2021, while lifting estimates for 10-year annual-average PCE inflation to 2.2% from 2.1%.

- The survey's 36 forecasters have upgraded headline and core CPI and PCE inflation at most forecast horizons compared with three months ago, with 5-year annual-average headline PCE inflation raised to 2.4% from 2.2%. Fed Presidents Robert Kaplan and Raphael Bostic have also raised their near-term outlook for prices, pushing up their preferred timeline for a taper.

- In a special question done annually, forecasters dropped their median estimate of the natural rate of unemployment by a third of a percentage point to 3.78%, the lowest estimate in the history of the series. The forecasters predict the American unemployment rate will decline to 3.6% in 2024 from 5.4% currently.

CANADA

CANADA: Canada Prime Minister Justin Trudeau called a snap election for Sept. 20, seeking to turn his minority Liberal government into a majority on support for record deficit spending through the pandemic and the vaccine rollout.

- The Liberals were reduced to a minority during the last election in October 2019 and held 155 of 338 seats in the House of Commons at dissolution, followed by Conservatives at 119 and a combined 56 seats for the Bloc Quebecois and NDP.

- Minority governments often last less than two years instead of the regular four-year term and Trudeau had signaled an early campaign for weeks. Conservatives led by Erin O'Toole have lagged the Liberals in recent public opinion polls, though it's unclear if Trudeau can win a majority needed to avoid votes of confidence on budgets and other key bills.

- "Canadians need to have their say" on managing the pandemic and recovery, Trudeau told reporters Sunday, just days after the chief health officer said the country has entered a fourth wave. Trudeau said a new Liberal government would work on affordable housing and daycare, fighting climate change and curbing Covid. For more see MNI Policy main wire at 1303ET.

OVERNIGHT DATA

- MNI: US JUL IMPORT PRICES +0.3%; EXPORT PRICES +1.3%; NON-AG +1.6%; AGRICULTURE -1.7%

- US University of Michigan Consumer Sentiment Aug 70.2 (81.2 Exp, 81.2 Prior)

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 15.53 points (0.04%) at 35515.38

- S&P E-Mini Future up 6.75 points (0.15%) at 4460.75

- Nasdaq up 6.6 points (0%) at 14822.9

- US 10-Yr yield is down 7.4 bps at 1.2851%

- US Sep 10Y are up 19/32 at 134-1.5

- EURUSD up 0.0065 (0.55%) at 1.1796

- USDJPY down 0.84 (-0.76%) at 109.57

- WTI Crude Oil (front-month) down $1.11 (-1.61%) at $67.99

- Gold is up $25.56 (1.46%) at $1778.53

- EuroStoxx 50 up 3.37 points (0.08%) at 4229.7

- FTSE 100 up 25.48 points (0.35%) at 7218.71

- German DAX up 39.93 points (0.25%) at 15977.44

- French CAC 40 up 13.57 points (0.2%) at 6896.04

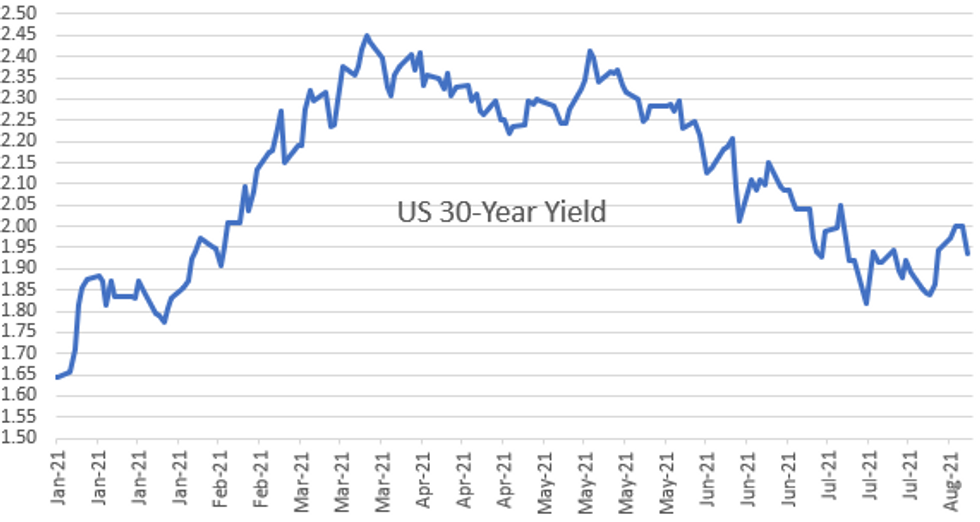

US TSY SUMMARY: Drop In Consumer Sentiment Triggers Bull Flattening

Following an initially quiet start, US TSYS rallied sharply following the release of the University of Michigan Consumer Sentiment survey for August, which reported an abrupt deterioration in confidence.

- The preliminary read came in at 70.2, well below the 81.2 expected print.

- TSY cash yields are now 1-6bp lower on the day with the curve bull flattening.

- Last yields: 2-year 0.2151%, 5-year 0.7892%, 10-year 1.2951%, 30-year 1.9448%

- TYU1 has traded up towards the highs of the day and last printed 133-30+ (L: 133-15 / 133-31+).

- Equities have taken a leg lower with the S&P500 trading down to 4463.32, from an afternoon high of 4467.03.

- Focus next week shifts to Advance Retail Sales on Tuesday, while Fed Chair Powell scheduled to take part in a town hall discussion on the same day.

US TSY FUTURES CLOSE

- 3M10Y -7.979, 122.596 (L: 122.429 / H: 130.407)

- 2Y10Y -6.164, 107.266 (L: 106.899 / H: 113.43)

- 2Y30Y -5.202, 172.206 (L: 172.006 / H: 178.534)

- 5Y30Y -1.778, 115.482 (L: 115.177 / H: 118.558)

- Current futures levels:

- Sep 2Y up 1/32 at 110-8.5 (L: 110-07.375 / H: 110-08.625)

- Sep 5Y up 8.75/32 at 124-2.25 (L: 123-25.75 / H: 124-02.5)

- Sep 10Y up 19.5/32 at 134-2 (L: 133-15 / H: 134-02.5)

- Sep 30Y up 1-26/32 at 164-23 (L: 163-00 / H: 164-24)

- Sep Ultra 30Y up 3-15/32 at 198-27 (L: 195-22 / H: 198-30)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.005 at 99.875

- Dec 21 +0.010 at 99.825

- Mar 22 +0.010 at 99.850

- Jun 22 +0.015 at 99.805

- Red Pack (Sep 22-Jun 23) +0.015 to +0.040

- Green Pack (Sep 23-Jun 24) +0.050 to +0.080

- Blue Pack (Sep 24-Jun 25) +0.090 to +0.095

- Gold Pack (Sep 25-Jun 26) +0.10 to +0.105

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N -0.00037 at 0.07763% (-0.00087/wk)

- 1 Month -0.00275 to 0.09275% (-0.00250/wk)

- 3 Month -0.00050 to 0.12425% (-0.00413/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00075 to 0.15663% (+0.00613/wk)

- 1 Year -0.00113 to 0.23875% (+0.00138/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $68B

- Daily Overnight Bank Funding Rate: 0.08% volume: $247B

- Secured Overnight Financing Rate (SOFR): 0.05%, $909B

- Broad General Collateral Rate (BGCR): 0.05%, $380B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $363B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $12.401B accepted vs. $34.314B submission

- Next scheduled purchases

- Mon 8/16 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Tue 8/17 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 8/18 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

- Thu 8/19 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Fri 8/20 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

Reverse Repo Operations, New High

NY Fed reverse repo usage climbs to new record high of $1.1T from 70 counterparties vs. Thursday's record of $1,087.342B.

System reserves continue to climb, rising by $81.4B in the week to Weds Aug 11, and $182.6B over the past 4 weeks. Fed net asset purchases have totaled $100B over the past 4 weeks, but the vast majority of the reserves created have been withdrawn into reverse repo (total $85B).

- The other big contributor to reserve growth has been the drawdown in the Treasury General Account, amounting to $57.7B last week, and $270.0B over the past four weeks.

EGBs-GILTS CASH CLOSE: BTPs Can't Quite Break Through

Core FI rallied strongly in the afternoon for the 2nd time this week after softer than expected US data - Wednesday it was CPI, today a very weak UMichigan consumer sentiment survey.

- Bunds and Gilts had been strengthening with bull flattening going into the 1500BST release, but yields extended to session lows following, and closed not far off.

- Outside of that, the main source of price intrigue was in Italian 10Y BTP spreads, which tested 100bp vs Bunds (99.5bp session low - Jun 17 low of 98.1bp would be next up).

- Relatively light volumes befit a nearly blank events calendar. French and Spanish Jul CPI final readings came in more or less unchanged from flash, and only supply was UK bills. No ECB/BoE speakers either.

- Tonight sees ratings reviews of Ireland (Moody's) and Belgium (DBRS), but a limited slate early next week (no major data, supply or speakers Monday).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at -0.739%, 5-Yr is down 0.6bps at -0.73%, 10-Yr is down 0.7bps at -0.467%, and 30-Yr is down 1.5bps at -0.022%.

- UK: The 2-Yr yield is down 1.9bps at 0.136%, 5-Yr is down 1.8bps at 0.295%, 10-Yr is down 2.8bps at 0.573%, and 30-Yr is down 2.6bps at 0.961%.

- Italian BTP spread up 0.9bps at 101.3bps /Spanish spread up 0.4bps at 68.6bps

FOREX: Greenback Under Pressure, JPY and CHF Outperform

- Broad dollar indices lost ground on Friday on the back of weaker import price index data and a sharp drop in University of Michigan sentiment data.

- The dollar index (-0.56% as of writing) had been on the backfoot, approaching the post CPI lows before the data, however the releases exacerbated the weakness, with the index sharply extending to the lowest levels of the week.

- Notable advances were seen in historically safe haven currencies with the Japanese Yen and Swiss Franc seeing particular strength.

- USDJPY (-0.72%) continued to trade with a heavy tone, extending losses for the week sub 110.00, hovering just above 109.50. Initial support not seen until 108.72, before more significant support at 108.47, a Fibonacci retracement.

- USDCHF (-0.86%) reversed aggressively almost back to unchanged on the week after a strong breakout, initiated last Friday following the payrolls data. The pair may look to 0.9120 previous lows for some short-term support.

- Elsewhere gains in line with the magnitude of DXY weakness were seen for GBP, AUD, NZD and NOK.

- The laggards were the Chinese Yuan and the Canadian Dollar, unable to benefit from the USD weakness.

- Attention will likely turn towards next week's US retail sales report as well as the latest set of FOMC minutes. The RBNZ will also meet where they are expected to raise the official cash rate to 0.5%. Additionally, the UK and Canada will report July CPI data.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.