Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI DATA BRIEF: US Jobless Claims Hit Pandemic Low of 348,000

- MNI REALITY CHECK: UK Summer Season To Underpin Retail Sales

- MNI INTERVIEW: Eurozone Debt Reform Essential, But Treaty Stays

US TSY SUMMARY: Heavy Year-End Positioning Eurodollar Trade

Rates trading firmer after the bell, off early session highs on moderate overall volumes. Not much of a reaction to early session data, futures firmer but remain off pre-open highs after weekly claims (348k/-29k vs. 364k est), continuing claims (2.820M vs. 2.800M est) and fourth consecutive Philly Fed read (19.4 vs. 23.1).- No data Friday, markets do have Dallas Fed Kaplan to listen to at 1100ET.

- Heavy Eurodlr volumes in front end, EDU1-EDH2 >1.1M. Year-end theme:

- Near 40k EDZ1/EDH2 spds sold -0.035 late overnight, largely driven by nod towards Fed tapering before yr end Wed's July FOMC minutes. Traders also posit general funding worries in the event of a stock rout contributing to the sell interest.

- Over 350k EDZ1 sold from 99.81 to 99.79 (-0.020-0.030) in late trade, total volume near 650,000; appr 50,000 EDU1 sold as well from 99.87 to .865.

- Tsy announced offering amounts for next wk's 2-, 5- and 7Y note auctions -- as expected: $60B, $61B and $62B respectively. New addition: 67D-Bill CMB (Cash Management Bill): $40B with Nov 1 maturity -- "suggesting confidence that they will have room through Nov 1 for those concerned about the debt ceiling" one desk posited. Whether the 119D-Bill CMB that is annc'd one day prior, remains to be seen.

- Strong $8B 30Y TIPS auction re-open: stops through -0.292% vs. -0.285% WI.

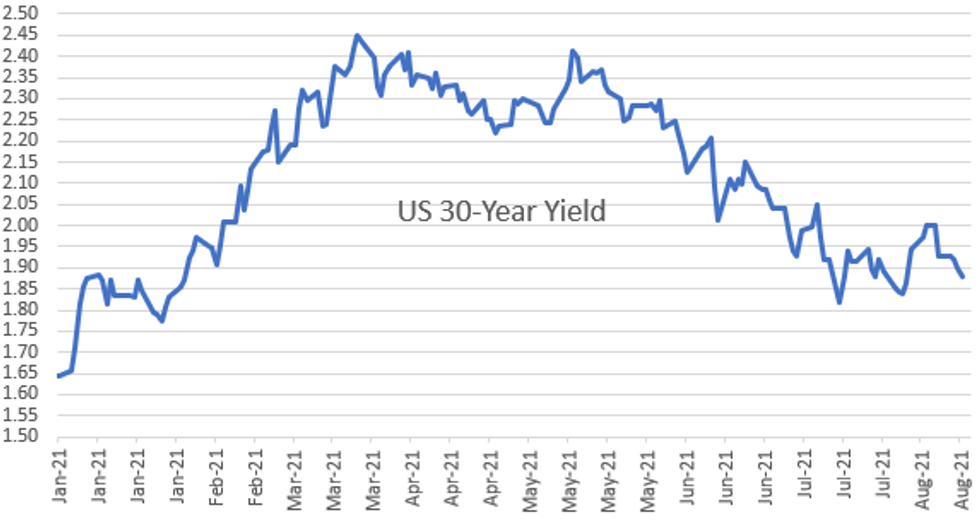

- The 2-Yr yield is up 0.2bps at 0.2176%, 5-Yr is down 0.5bps at 0.7637%, 10-Yr is down 1.7bps at 1.2417%, and 30-Yr is down 2bps at 1.8776%.

US

US: U.S. workers' claims for first-time jobless benefits dropped by 29,000 to a post-Covid low of 348,000 in the latest week, the Labor Department said Thursday, suggesting the labor market is still improving gradually despite a surge in the Delta variant.

- MNI reported this week Federal Reserve economists are increasingly pessimistic about the prospect of a fall surge in the workforce as supply chain issues, labor mismatches and pandemic-related factors slow expectations for improvement.

EUROPE

EU: The eurozone should reform strict rules on borrowing but changing European treaties is too hard and key provisions including a 60% debt-to-GDP limit cannot be ignored, a senior German member of the European Parliament's biggest conservative force told MNI.

- In the latest sign of an evolving consensus on the need to overhaul the European Union's Stability and Growth Pact, Markus Ferber, spokesman for the EPP group in the European Parliament's Economic and Monetary Affairs Committee, said some countries' debt levels "could quickly turn out to be unsustainable once the European Central Bank tightens monetary policy. For more see MNI Policy main wire at 1138ET.

- Helen Dickinson, the CEO at the British Retail Consortium said July continues to see strong sales, albeit at a slower pace as lifting restrictions didn't bring an anticipated in-store boost. However, "with social events back on for the summer calendar, formalwear and beauty all began to see notable improvement," she said. For more see MNI Policy main wire at 1017ET.

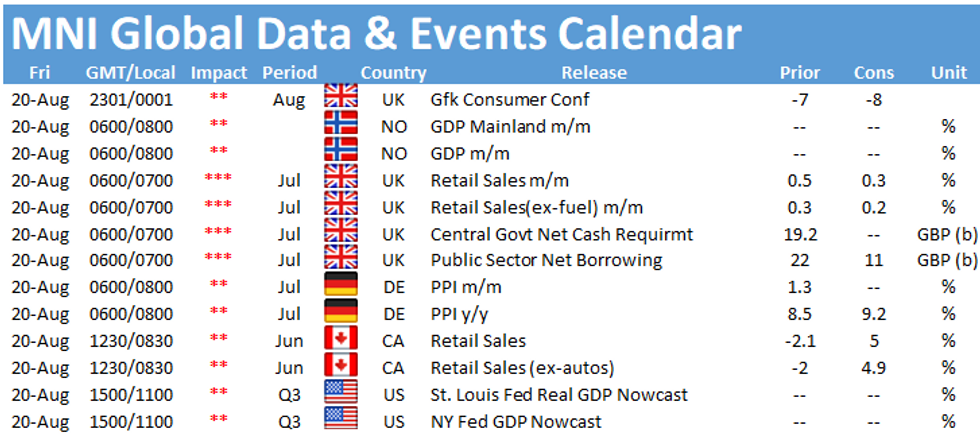

OVERNIGHT DATA

- US JOBLESS CLAIMS -29K TO 348K IN AUG 14 WK

- US PREV JOBLESS CLAIMS REVISED TO 377K IN AUG 07 WK

- US CONTINUING CLAIMS -0.079M to 2.820M IN AUG 07 WK

- US AUG PHILADELPHIA FED MFG INDEX 19.4

MARKET SNAPSHOT

Key late session market levels:- DJIA down 84.29 points (-0.24%) at 34849.74

- S&P E-Mini Future up 5.75 points (0.13%) at 4396.75

- Nasdaq up 17.8 points (0.1%) at 14536.5

- US 10-Yr yield is down 1.7 bps at 1.2417%

- US Sep 10Y are up 6/32 at 134-10.5

- EURUSD down 0.0035 (-0.3%) at 1.1676

- USDJPY up 0.03 (0.03%) at 109.79

- WTI Crude Oil (front-month) down $1.72 (-2.63%) at $63.72

- Gold is down $7.09 (-0.4%) at $1780.13

- EuroStoxx 50 down 64.71 points (-1.54%) at 4124.71

- FTSE 100 down 110.46 points (-1.54%) at 7058.86

- German DAX down 200.16 points (-1.25%) at 15765.81

- French CAC 40 down 164.22 points (-2.43%) at 6605.89

US TSY FUTURES CLOSE

- 3M10Y -0.568, 118.675 (L: 114.901 / H: 119.756)

- 2Y10Y -2.05, 102.037 (L: 101.414 / H: 104.756)

- 2Y30Y -2.439, 165.529 (L: 164.26 / H: 168.713)

- 5Y30Y -1.91, 110.636 (L: 110.262 / H: 113.29)

- Current futures levels:

- Sep 2Y up 0.125/32 at 110-8.375 (L: 110-08.25 / H: 110-09.375)

- Sep 5Y up 0.75/32 at 124-3.25 (L: 124-02 / H: 124-08.25)

- Sep 10Y up 5.5/32 at 134-10 (L: 134-05.5 / H: 134-17)

- Sep 30Y up 24/32 at 165-26 (L: 165-04 / H: 166-06)

- Sep Ultra 30Y up 1-11/32 at 200-30 (L: 199-27 / H: 201-31)

US EURODOLLAR FUTURES CLOSE

- Sep 21 -0.008 at 99.865

- Dec 21 -0.020 at 99.80

- Mar 22 -0.010 at 99.840

- Jun 22 -0.005 at 99.80

- Red Pack (Sep 22-Jun 23) steady to +0.005

- Green Pack (Sep 23-Jun 24) +0.005 to +0.010

- Blue Pack (Sep 24-Jun 25) +0.015 to +0.025

- Gold Pack (Sep 25-Jun 26) +0.025 to +0.040

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N -0.00013 at 0.07850% (+0.00088/wk)

- 1 Month -0.00050 to 0.08788% (-0.00388/wk)

- 3 Month -0.00013 to 0.13075% (+0.00650/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00375 to 0.15463% (-0.00200/wk)

- 1 Year +0.00025 to 0.23525% (-0.00350/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $65B

- Daily Overnight Bank Funding Rate: 0.08% volume: $255B

- Secured Overnight Financing Rate (SOFR): 0.05%, $935B

- Broad General Collateral Rate (BGCR): 0.05%, $375B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $357B

- (rate, volume levels reflect prior session)

- TSY 4.5Y-7Y, $6.001B accepted vs. $21.522B submission

- Next scheduled purchase

- Fri 8/20 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

FED: REVERSE REPO OPERATION, New Record High

NY Fed reverse repo usage slips to 1,109.938B from 78 counter-parties vs. Wed's new record high of $1,115.656B. Prior record of $1,087.342B from Thursday, Aug 12.

PIPELINE: ADB Priced

- Date $MM Issuer (Priced *, Launch #)

- 08/19 $1B *ADB 5Y FRN/SOFR +18

- 08/19 $750M Pilgrims Pride 10.5NC5

EGBs-GILTS CASH CLOSE: Strong But Underwhelming Rally

Bund and Gilt yields fell Thursday, but the magnitude of the drop was relatively tame considering the broader risk-off context.

- 10Y Bund yields tested -0.50% for the 2nd time this week as a safe haven bid built up over the morning, but finished above -0.49%. Gilts outperformed.

- European stock indices fell by more than 2% at one point and oil prices more than 3%, amid renewed concerns over global growth/COVID, but ended up off the lows.

- Periphery spreads widened (Italy underperformed) amid the risk asset sell-off.

- Supply this morning came from France (OATs, EUR6.997bn, & OATi/OATei, EUR991mn).

- Quiet schedule Friday: no bond supply; German PPI and UK Retail Sales data feature.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at -0.747%, 5-Yr is down 0.6bps at -0.744%, 10-Yr is down 0.7bps at -0.489%, and 30-Yr is down 1.7bps at -0.051%.

- UK: The 2-Yr yield is down 2.5bps at 0.116%, 5-Yr is down 3bps at 0.262%, 10-Yr is down 2.7bps at 0.538%, and 30-Yr is down 2bps at 0.941%.

- Italian BTP spread up 1.8bps at 105.1bps / Spanish up 0.8bps at 70.8bps

FOREX: Dollar Index Extends To Fresh 2021 Highs

- The greenback extended past the March peak to fresh nine-month highs amid concerns over global growth that weighed heavily on risk and most other G10 currencies.

- The additional slump in commodities prices placed commodity-tied currencies under particular pressure, with both AUD(-1.13%) and NZD (-0.89%) extending their recent downtrends.

- Specific weakness in oil prices heavily affected the Norwegian Krone and Canadian dollar, the biggest laggards in G10 FX, both retreating well over 1% against the US dollar. USDCAD has taken out the July highs at 1.2807 and the next point of focus will be the year's highs residing at 1.2881.

- GBP also performed poorly losing 0.8%, however EURUSD, while still below the 1.1704 breakout, held a more contained range as potential expiries at 1.1700 for the NY cut appeared to cap the price action. As such, EURGBP squeezed higher back above 0.85, rising half a percent.

- Despite the demand for the US dollar, other haven currencies such as JPY and CHF held firm on Thursday and were the notable outperformers, broadly unchanged for the session.

- Moves in emerging market currency indices were inversely correlated with the dollar index, however, there was notable underperformance in the South African Rand, sliding 1.75%.

- Possible comments from RBA Assistant Governor Christopher Kent expected overnight, before UK retail sales and public sector borrowing data headline the European docket. Canadian retail sales data will close off the weekly data schedule with potential comments from Dallas Fed's Kaplan.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.