Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: Fed Jackson Hole Conference To Take Place Virtually

- MNI BRIEF: Fed's Kaplan Says Delta Covid Could Push Back Taper

- KAPLAN: GOOD TO WEAN OFF ASSET BUYS AS SOON AS WE ARE ABLE TO, Bbg

- KAPLAN: DON'T KNOW IF ASSET BUYS ARE HELPING LABOR MARKET, Bbg

- KAPLAN: EXTREME INFLATION MOVES LIKELY TO MODERATE, Bbg

- KAPLAN SAYS IF DELTA IS HAVING A MORE NEGATIVE EFFECT ON GDP GROWTH COULD CAUSE ME TO ADJUST MY VIEWS - RTRS

US

FED: Dallas Federal Reserve President Robert Kaplan said on Friday he was watching carefully for any economic impact from the Delta variant of the coronavirus and might need to adjust his views on tapering should it slow economic growth.

- The "big caveat" is the Delta variant and if it turns out to be persistent enough or unfold differently as it has in some countries to affect demand, in which case it could impact the decision when to taper, he said. "I've got to take that into account, and will adjust my views accordingly. We've got a month between now and the next FOMC meeting, and it's a good thing we've got a month to see how this all unfolds because I don't know. I've got to be open minded and I will be." For more see MNI Policy main wire at 1156ET.

- "While we are disappointed that health conditions will prevent us from being able to gather in person at the Jackson Lake Lodge this year as we had planned, the safety of our guests and the Teton County community is our priority," said Kansas City Fed president Esther George, in a statement.

- The Kansas City Fed will release the program's full agenda Thursday, August 26 at 8 p.m. ET. Fed Chair Jerome Powell is scheduled to give livestreamed remarks on Friday at 10 a.m. ET.

OVERNIGHT DATA

No economic data released Friday.

- SEES BROADENING IN PRICE PRESSURES, 2.5% PCE 2022, Bbg

- SEES PCE INFLATION RATE ENDING 2021 AT 3.8%-3.9%, bbg

- SEES JOBLESS RATE DRIFTING DOWN TO 4.5% BY YEAR-END, bbg

- WATCHING IMPACT OF DELTA VARIANT ON GDP CAREFULLY, bbg

MARKET SNAPSHOT

Key late session market levels:- DJIA up 183.76 points (0.53%) at 35077.62

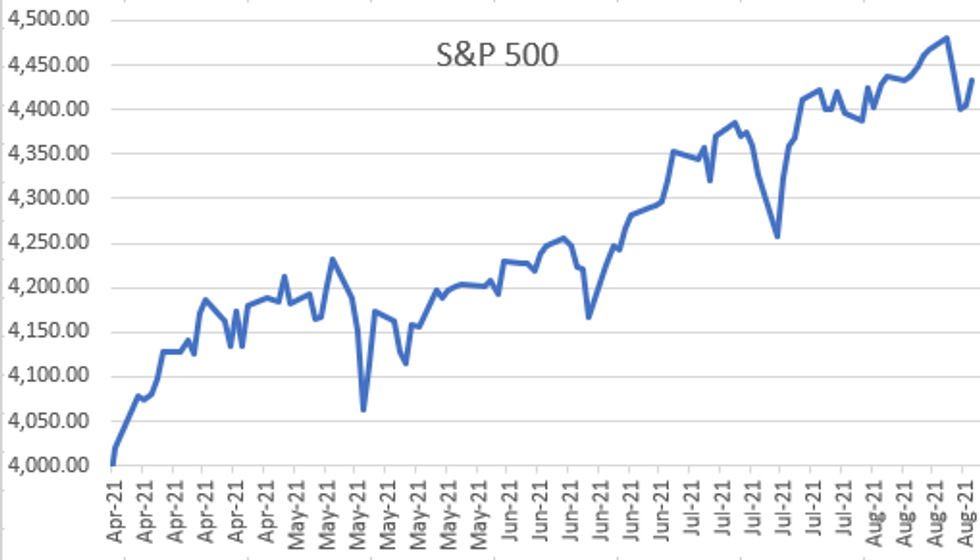

- S&P E-Mini Future up 28.25 points (0.64%) at 4430.25

- Nasdaq up 138.3 points (1%) at 14679.66

- US 10-Yr yield is up 1.7 bps at 1.26%

- US Sep 10Y are down 7/32 at 134-3.5

- EURUSD up 0.0021 (0.18%) at 1.1696

- USDJPY up 0.07 (0.06%) at 109.81

- WTI Crude Oil (front-month) down $1.37 (-2.15%) at $62.32

- Gold is up $2.08 (0.12%) at $1782.46

- EuroStoxx 50 up 22.79 points (0.55%) at 4147.5

- FTSE 100 up 29.04 points (0.41%) at 7087.9

- German DAX up 42.23 points (0.27%) at 15808.04

- French CAC 40 up 20.22 points (0.31%) at 6626.11

US TSY SUMMARY: Cautious Risk-On Ahead Weekend, Dallas Fed Kaplan Eyes Delta

Rates traded higher briefly early Friday, pared gains into the equity open and continued to trade weaker into the close. Dearth of economic data with no obvious headline driver or block posts, two-way positioning and option-tied hedging noted ahead Dallas Fed Pres Kaplan event at Texas Tech business college.

- After calling for taper annc in Sep/begin in Oct last week, Kaplan (noted hawk, voter in 2022) offered caveats based on Covid-Delta variant: A MORE NEGATIVE EFFECT ON GDP GROWTH COULD CAUSE ME TO ADJUST MY VIEWS - RTRS.

- US Pres Biden's brief on Afghanistan evacuation deemed underwhelming but not market moving. Latest weekly approval rating from Ipsos shows President Biden's disapproval rating higher than his approval rating for the first time in his presidency. Biden's disapproval rating rose to 49%, from 43% last week. His approval rating fell to 46%, from 50% previously.

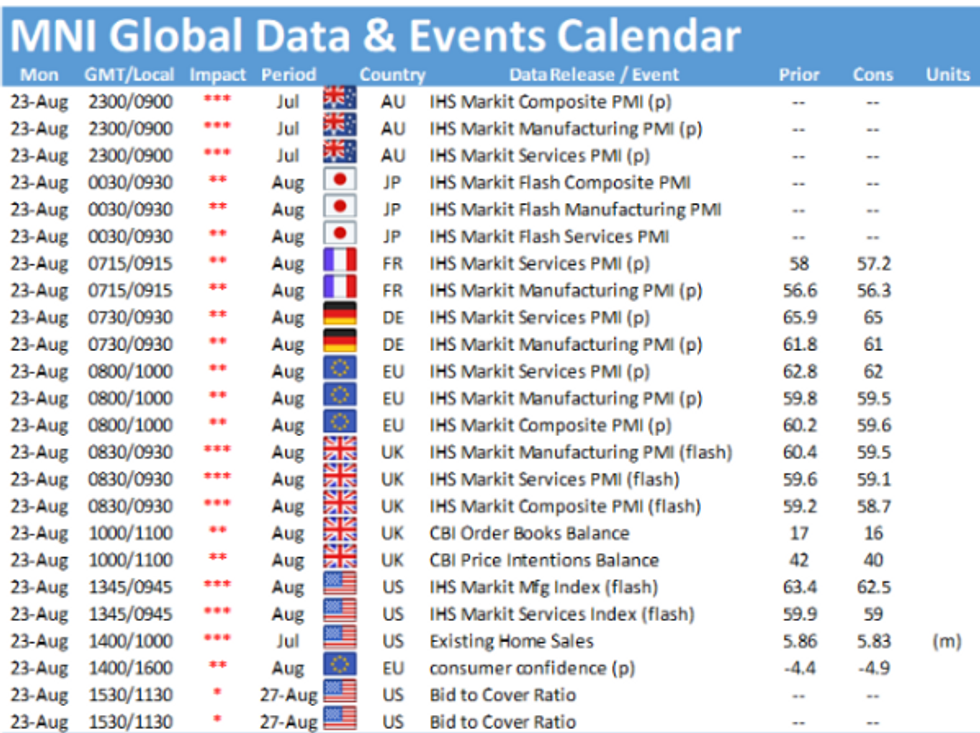

- Focus on next week's Markit PMIs (Mon), New Home Sales (Tue), Durables (Wed) and of course the KC Fed's annual economic symposium in Jackson Hole WY next Friday. Scheduled events/speakers expected to be released appr 1900ET Thursday evening.

- Expect volumes to surge as Tsy Sep/Dec quarterly futures continues, first notice Tuesday, Aug 31 when Dec takes lead quarterly position. Sep Tsy optyions expire next Friday as well.

- The 2-Yr yield is up 0.5bps at 0.2241%, 5-Yr is up 1.8bps at 0.785%, 10-Yr is up 1.7bps at 1.26%, and 30-Yr is up 0.3bps at 1.8735%.

US TSY FUTURES CLOSE

- 3M10Y +1.757, 120.765 (L: 117.173 / H: 121.434)

- 2Y10Y +1.058, 103.227 (L: 100.662 / H: 103.931)

- 2Y30Y -0.449, 164.61 (L: 163.475 / H: 166.024)

- 5Y30Y -1.42, 108.719 (L: 108.422 / H: 110.627)

- Current futures levels:

- Sep 2Y down 0.125/32 at 110-8.125 (L: 110-08 / H: 110-08.75)

- Sep 5Y down 3/32 at 124-0.5 (L: 123-31.5 / H: 124-05.5)

- Sep 10Y down 6.5/32 at 134-4 (L: 134-02 / H: 134-14)

- Sep 30Y down 2/32 at 165-24 (L: 165-18 / H: 166-06)

- Sep Ultra 30Y up 1/32 at 200-31 (L: 200-23 / H: 201-27)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.007 at 99.873

- Dec 21 +0.010 at 99.810

- Mar 22 +0.005 at 99.845

- Jun 22 +0.005 at 99.805

- Red Pack (Sep 22-Jun 23) -0.01 to steady

- Green Pack (Sep 23-Jun 24) -0.02 to -0.01

- Blue Pack (Sep 24-Jun 25) -0.02

- Gold Pack (Sep 25-Jun 26) -0.025 to -0.02

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N -0.00112 at 0.07738% (-0.00025/wk)

- 1 Month -0.00200 to 0.08588% (-0.00588/wk)

- 3 Month -0.00237 to 0.12838% (+0.00413/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00200 to 0.15263% (-0.00400/wk)

- 1 Year +0.00138 to 0.23663% (-0.00212/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $67B

- Daily Overnight Bank Funding Rate: 0.08% volume: $250B

- Secured Overnight Financing Rate (SOFR): 0.05%, $925B

- Broad General Collateral Rate (BGCR): 0.05%, $384B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $360B

- (rate, volume levels reflect prior session)

- TSY 22.5Y-30Y, $1.999B accepted vs. $3.284B submission

- Next scheduled purchases

- Mon 8/23 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Tue 8/24 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Wed 8/25 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Thu 8/26 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Fri 8/27 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

FED: REVERSE REPO OPERATION, Holding above $1T

NY Fed reverse repo usage climbs to 1,111.908B from 78 counter-parties vs. $1,109.938B on Thursday. Record high of $1,115.656B set Wednesday, Aug 18.

PIPELINE: Corporate Debt Recap

Well off last week's $40B total issuance- Date $MM Issuer (Priced *, Launch #)

- 08/20 No new issuance on tap Friday

- $1.9B Priced Thursday; $10.6B/wk

- 08/19 $1B *ADB 5Y FRN/SOFR +18

- 08/19 $900M *Pilgrims Pride 10.5NC5 3.5%, upsized from $750M

FOREX: Dollar Index Set For Highest Weekly Close Since November 2020

- Broad dollar indices traded in a narrow range on Friday, posting a small loss as a recovery in equity indices stalled the strong dollar rally on the week.

- The Dollar index (DXY) will close at its best weekly level since November 2020 amid concerns over global growth and rising geopolitical risks that weighed heavily on sentiment and saw commodity prices slump and investors flock to haven currencies.

- Without any significant data/event risk, Friday acted as a consolidation day for most G10 currencies. However, with EURUSD edging back towards 1.17, euro crosses saw some further support with EURAUD and EURNZD rising around 0.3%.

- USDCAD had a notable spike above the year's best levels, printing fresh highs at 1.2949, before falling a big figure throughout the US session to close around 1.2850. The break of 1.2807 earlier in the week confirmed the resumption of the uptrend and today's rally fell just short of 1.2957, the high from Dec 21, 2020 and a Fibonacci projection at 1.2976. These levels remain firm short-term resistance.

- In emerging markets, further weakness in the South African rand (down 1%) was trumped by a 1.4% move lower in the Mexican peso. The deterioration in technical conditions for the peso has seen solid follow through on the break above 20.25 in USDMXN.

- Flash PMIs will kick off next week's data calendar before markets will eagerly anticipate Fed's Jerome Powell at the Jackson Hole Symposium later in the week. On Friday, markets will also receive US Core PCE price data.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.