Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- JEFFERIES CEO DOES NOT FORSEE RETURN TO OFFICE UNTIL JAN. 31, Bbg

- Goldman Sachs Tells US Staff to Work From Home Until Jan. 18 as Omicron Cases Rise, MTN

- FDA AUTHORIZES PFIZER BOOSTER FOR PEOPLE 12-15 YEARS OLD, Bbg (UK approved last wk)

US TSYS: Strong Risk-On Start To 2022

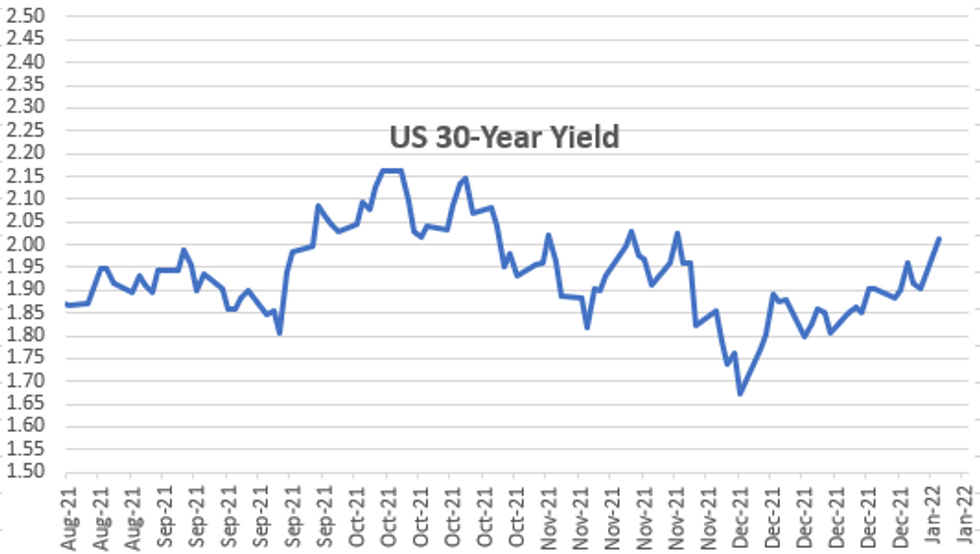

Rates open 2022 sharply lower with a decidedly risk-on tone with equities strong (ESH2 +25.0 at 4783.5) but slightly off all-time highs set last Thu (4797.75). 30YY topped 2.0% with 2.0233% high, 10YY hit 1.6332% high. TYH2 tapped first support of 129-12.5, 76.4% retracement of the Nov 24 - Dec 20 rally.- Gold -27.46 at 1801.74; West Texas Crude +0.84 at 76.05; US$ index DXY +.547 at 96.217.

- Rates started off weaker, albeit on very light volumes as NZ, Australia, Japan, London and Canada out for New Years holiday. Best volumes in weeks as sell-off accelerated into midday, TYH2 over 1.2M after the bell.

- Nevertheless, market depth remained thin, trade whippy. Contributing to steeper curves, trading desks reporting domestic real$ buying 2s, foreign real$ selling 10s, sporadic deal-tied selling and flattener unwinds in intermediates vs. long end. Some stops triggered in rates on way down, technical selling.

- Early flow included prop, fast$ and deal-tied selling in 2s-10s, Real$ selling 30s.

- Resumption of corporate issuance ($11.75B total Monday) absent since around Dec 10 contributed marginally to selling.

- The 2-Yr yield is up 4.4bps at 0.7758%, 5-Yr is up 9.6bps at 1.3589%, 10-Yr is up 11.1bps at 1.621%, and 30-Yr is up 10.7bps at 2.0105%.

OVERNIGHT DATA

- US NOV CONSTRUCT SPENDING +0.4%

- US NOV PRIVATE CONSTRUCT SPENDING +0.6%

- US NOV PUBLIC CONSTRUCT SPENDING -0.2%

- IHS MARKIT MEXICO DEC. MANUFACTURING PMI 49.4 VS 49.4 PRIOR

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 191.15 points (0.53%) at 36529.36

- S&P E-Mini Future up 23.25 points (0.49%) at 4782

- Nasdaq up 165.7 points (1.1%) at 15813.46

- US 10-Yr yield is up 11.1 bps at 1.621%

- US Jun 10Y are down 32/32 at 129-11.5

- EURUSD down 0.0072 (-0.63%) at 1.1299

- USDJPY up 0.21 (0.18%) at 115.28

- WTI Crude Oil (front-month) up $0.85 (1.13%) at $76.08

- Gold is down $26.54 (-1.45%) at $1802.47

- EuroStoxx 50 up 33.41 points (0.78%) at 4331.82

- German DAX up 135.87 points (0.86%) at 16020.73

- French CAC 40 up 64.19 points (0.9%)at 7217.22

US TSY FUTURES CLOSE

- 3M10Y +11.71, 156.889 (L: 146.319 / H: 156.984)

- 2Y10Y +7.008, 84.404 (L: 75.73 / H: 85.396)

- 2Y30Y +6.274, 123.047 (L: 113.691 / H: 124.681)

- 5Y30Y +0.891, 64.752 (L: 60.442 / H: 66.229)

- Current futures levels:

- Mar 2Y down 3.5/32 at 108-31.25 (L: 108-30.25 / H: 109-02.125)

- Mar 5Y down 17.25/32 at 120-14 (L: 120-13.5 / H: 120-28.5)

- Mar 10Y down 1-01.5/32 at 129-13.5 (L: 129-12.5 / H: 130-11)

- Mar 30Y down 2-19/32 at 157-27 (L: 157-25 / H: 160-05)

- Mar Ultra 30Y down 4-30/32 at 192-06 (L: 191-31 / H: 196-18)

US EURODOLLAR FUTURES CLOSE

- Mar 22 -0.010 at 99.645

- Jun 22 -0.015 at 99.390

- Sep 22 -0.030 at 99.165

- Dec 22 -0.050 at 98.905

- Red Pack (Mar 23-Dec 23) -0.105 to -0.065

- Green Pack (Mar 24-Dec 24) -0.12 to -0.11

- Blue Pack (Mar 25-Dec 25) -0.14 to -0.125

- Gold Pack (Mar 26-Dec 26) -0.165 to -0.145

SHORT TERM RATES

US DOLLAR LIBOR: No new settlements w/ London out for New Years, resume Tuesday. Last Friday's 2021 year-end settlements:

- O/N -0.00825 at 0.06438% (-0.00537/wk)

- 1 Month -0.00063 to 0.10125% (+0.00000/wk)

- 3 Month -0.00525 to 0.20913% (-0.00875/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00638 to 0.33875% (-0.00450/wk)

- 1 Year -0.00562 to 0.58313% (+0.01600/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $49B

- Daily Overnight Bank Funding Rate: 0.07% volume: $88B

- Secured Overnight Financing Rate (SOFR): 0.04%, $923B

- Broad General Collateral Rate (BGCR): 0.05%, $327B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $302B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $6.301B accepted vs. $11.995B submission

- Next scheduled purchases:

- Tue 01/04 1100-1120ET: TIPS 1Y-7.5Y, appr $1.525B

- Wed 01/05 1010-1030ET: Tsy 7Y-10Y, appr $2.425B vs. $2.825B prior

- Wed 01/05 1100-1120ET: Tsy 22.5Y-30Y, appr $1.825B

- Thu 01/06 1100-1120ET: TIPS 7.5Y-30Y, appr $0.925B

- Fri 01/07 1010-1030ET: Tsy 0Y-2.25Y, appr $9.325B

FED Reverse Repo Operation:

NY Federal Reserve/MNI

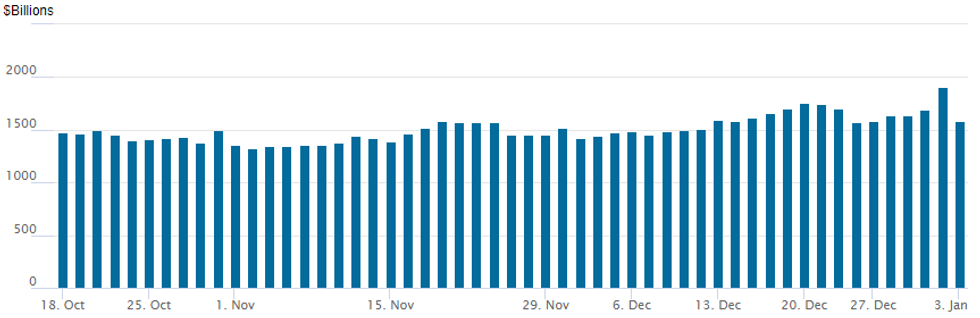

NY Fed reverse repo usage recedes to $1,579.526B from 76 counterparties from last Friday's record high of $1,904.582B (prior record high of $1,758.041B posted Monday, December 20)

PIPELINE: $11.75B High-Grade Issuance Launched

- Date $MM Issuer (Priced *, Launch #)

- 01/03 $3.25B #Scotiabank, $1.35B 3Y +45, $300M 3Y FRN/SOFR+46, $750M 5Y +60, $850M 10Y +85

- 01/03 $2B #Caterpillar $1.2B 2Y +18, $300M 2Y FRN/SOFR +17, $500M 5Y +35

- 01/03 $1.5B #Metropolitan Life Global $900M 5Y +53, +600M 10Y +78

- 01/03 $1.5B #Blackstone Holdings, $500M +10Y +95, $1B 30Y +120

- 01/03 $1.5B #Santander 6NC5 +112.5

- 01/03 $1.1B #GA Global Funding Trust $550M 5Y +90, +550M 10Y +130

- 01/03 $900M #CNO Global $400M 3Y +65, $500M 7Y +112

OUTLOOK

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/01/2022 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 04/01/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 04/01/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 04/01/2022 | 0730/0830 | *** |  | CH | CPI |

| 04/01/2022 | 0745/0845 | *** |  | FR | HICP (p) |

| 04/01/2022 | 0855/0955 | ** |  | DE | unemployment |

| 04/01/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Manufacturing PMI (Final) |

| 04/01/2022 | 0930/0930 | ** | | UK | BOE M4 |

| 04/01/2022 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 04/01/2022 | - | *** |  | US | domestic made vehicle sales |

| 04/01/2022 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 04/01/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 04/01/2022 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 04/01/2022 | 1500/1000 | ** | | US | JOLTS jobs opening level |

| 04/01/2022 | 1500/1000 | ** | | US | JOLTS quits Rate |

| 04/01/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 04/01/2022 | 1630/1130 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok