Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED'S BULLARD: 4 RATE RISES IN 2022 NOW APPEAR LIKELY: DJ

- MNI: Fed Could Give Nod to March Hike This Month-Ex-Officials

- US DATA: Core Goods Pick Up Steam, While Shelter Restrains Service Gains

- US DATA: Pandemic Reopening CPI Categories Remain Volatile

- MNI BRIEF: US Economy Grew Modestly At End Of '21-Beige Book

US TSYS: CPI As Exp; Bullard Cites Inflation For Likely Mar Hike, Four in '22

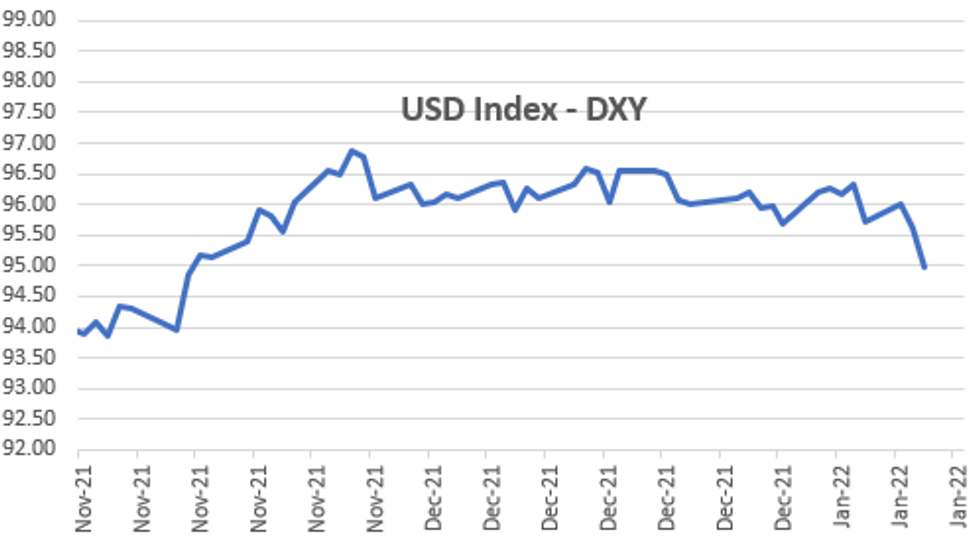

Support in rates evaporated late Wednesday after StL Fed Bullard said four hikes in 2022 are likely in a Wall Street Journal interview, citing rising inflation with the first coming in March. Still an inside range session with levels off early session lows by the close (30YY 2.0861% vs 2.0883H; 10YY 1.7357% vs. 1.7517%H.- Not much fanfare to largely in-line Dec CPI: CPI 0.5%, CORE 0.6%; CPI Y/Y 7.0%, CORE Y/Y 5.5%. Markets had priced in higher inflation metrics already, delayed rally in rates and equities as measure not much worse than expected. US$ to two-month lows, however (DXY -.685 to 94.939).

- Cross asset inflation observations -- CRUDE OIL INVENTORIES FELL 4.55 MLN BARRELS, EIA vs. exp decline of 1.85 million barrels. West Texas crude surged to near 83.0 (82.94H).

- Tsy futures pare gains after $36B 10Y note auction re-open (91282CDJ7) tailed slightly again: 1.723% high yield vs. 1.719% WI; 2.43x bid-to-cover better than last month's 2.43x but still shy a 2.51x 5-month average

- Indirect take-up falls to 65.53% (lowest since July) vs. Dec's 68.84%; direct bidder take-up highest since June at 17.86% while primary dealer take-up bounces to 16.61% vs. 13.37% prior.

- The 2-Yr yield is up 2.6bps at 0.9089%, 5-Yr is up 0.2bps at 1.5007%, 10-Yr is down 0.2bps at 1.734%, and 30-Yr is up 2bps at 2.0817%.

US

FED: The Federal Reserve could signal a March liftoff of interest rates from near-zero as soon as this month's meeting as the labor market verges on full employment amid a persistent shortage of workers and inflation continues to soar, several former Fed officials and staffers told MNI.

- "The stars will be well aligned for liftoff. The economy has strong momentum, the labor situation is close to full employment, and a policy rate hike would come as no surprise to markets," said former Federal Reserve Bank of Atlanta president Dennis Lockhart. " Unless we see a stark reversal of inflation trends or much worse real economy impacts of Omicron, I think it is highly likely the Fed will move in March, and will begin signaling such coming out of the January meeting."

- Former Fed Board of Governors research director David Wilcox reckoned that while the FOMC may not commit to hike in March, the committee this month "will create room to have that option available to them if they decide it’s needed." For more see MNI Policy main wire at 1444ET.

US DATA: December saw the hottest core goods CPI print (+1.24% M/M) since June, though core services slipped to a 3-month low (+0.30% M/M).

- Core goods, new and used vehicle gains led the uptick; we also saw decent contributions from other categories including Apparel (fastest growth since Jan 2021) and household furnishings.

- Core services, the story is largely about shelter prices pulling back a bit: OER and rent of primary residence saw the slowest increases since August (+0.40% M/M and +0.39% M/M, respectively), though it's basically steadied out at +0.4% growth for the past few months. A variety of services areas made flat/negative contributions in December (Communication, recreation, education, motor vehicle insurance).

- Plenty of volatility still in the closely-watched pandemic reopening categories - airfares and lodging growth slowed a bit but still hot; used car prices accelerated to the fastest pace of growth since June (in line with some expectations of a pickup), while new cars saw similar growth to November. Car/Truck rental firmly negative M/M.

- "Growth continued to be constrained by ongoing supply chain disruptions and labor shortages," the report said. "Despite the modest pace of growth, demand for materials and inputs, and demand for workers, remained elevated among businesses."

- The Fed signaled at its December meeting that it was likely to raise interest rates three times this year, and officials are now actively debating balance sheet runoffs.

- On inflation, the report said "contacts from most Federal Reserve Districts reported solid growth in prices charged to customers, but some also noted that price increases had decelerated a bit from the robust pace experienced in recent months."

OVERNIGHT DATA

- US DEC CPI 0.5%, CORE 0.6%; CPI Y/Y 7.0%, CORE Y/Y 5.5%

- US DEC ENERGY PRICES -0.4%

- US DEC OWNERS' EQUIVALENT RENT PRICES 0.4%

- Dec CPI Unrounded % M/M figures: Headline 0.47%; Core: 0.55%

- Dec CPI Unrounded % Y/Y figures: Headline 7.036%; Core: 5.453%

MARKETS SNAPSHOT

Key late session market levels

- DJIA down 4.75 points (-0.01%) at 36258.73

- S&P E-Mini Future up 6.75 points (0.14%) at 4714.25

- Nasdaq up 25.4 points (0.2%) at 15199.15

- US 10-Yr yield is down 0.2 bps at 1.734%

- US Mar 10Y are up 4/32 at 128-16.5

- EURUSD up 0.0079 (0.7%) at 1.1448

- USDJPY down 0.76 (-0.66%) at 114.41

- WTI Crude Oil (front-month) up $1.41 (1.74%) at $82.60

- Gold is up $5.18 (0.28%) at $1827.81

- EuroStoxx 50 up 34.85 points (0.81%) at 4316.39

- FTSE 100 up 60.35 points (0.81%) at 7551.72

- German DAX up 68.51 points (0.43%) at 16010.32

- French CAC 40 up 53.81 points (0.75%) at 7237.19

US TSY FUTURES CLOSE

- 3M10Y -0.167, 160.974 (L: 158.505 / H: 162.388)

- 2Y10Y -2.604, 82.311 (L: 80.597 / H: 85.219)

- 2Y30Y -0.352, 117.012 (L: 114.941 / H: 119.132)

- 5Y30Y +2.035, 58.025 (L: 54.264 / H: 58.863)

- Current futures levels:

- Mar 2Y down 0.75/32 at 108-23.25 (L: 108-22.75 / H: 108-25.25)

- Mar 5Y up 1/32 at 119-23.5 (L: 119-19.25 / H: 119-28)

- Mar 10Y up 3.5/32 at 128-16 (L: 128-10.5 / H: 128-22.5)

- Mar 30Y down 2/32 at 155-28 (L: 155-22 / H: 156-17)

- Mar Ultra 30Y down 13/32 at 189-26 (L: 189-21 / H: 191-06)

US TSY FUTURES: TECH (H2) Bearish Threat Still Present

- RES 4: 131-19 High Dec 20 and key resistance

- RES 3: 130-18+/28+ High Dec 31 / High Dec 22

- RES 2: 129-31 Low Dec 8 and a recent breakout level

- RES 1: 129-00/18 High Jan 6 / 20-day EMA

- PRICE: 128-15 @ 16:32 GMT Jan 12

- SUP 1: 127-30 1.764 proj of the Dec 20 - 29 - 31 price swing

- SUP 2: 127-18+ 2.00 proj of the Dec 20 - 29 - 31 price swing

- SUP 3: 127-07 2.236 proj of the Dec 20 - 29 - 31 price swing

- SUP 4: 127-00 Round number support

Treasuries are trading above Monday’s lows. The contract remains vulnerable though. A clear bearish price sequence of lower lows and lower highs continues to reinforce current sentiment and signals scope for further weakness. The moving average set-up is in bear mode and this also highlights a bearish condition. Initial resistance is seen at 129-00, the Jan 6 high. The focus is on 127-18+ next, a Fibonacci projection.

US EURODOLLAR FUTURES CLOSE

- Mar 22 steady at 99.590

- Jun 22 -0.010 at 99.295

- Sep 22 -0.010 at 99.050

- Dec 22 -0.005 at 98.785

- Red Pack (Mar 23-Dec 23) steady to +0.015

- Green Pack (Mar 24-Dec 24) +0.020 to +0.030

- Blue Pack (Mar 25-Dec 25) +0.030

- Gold Pack (Mar 26-Dec 26) +0.030 to +0.035

SHORT TERM RATES

US DOLLAR LIBOR: Settlement resumes:

- O/N -0.00014 at 0.07729% (+0.00458/wk)

- 1 Month -0.00286 to 0.11014% (+0.00485/wk)

- 3 Month +0.00614 to 0.24443% (+0.00829/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00243 to 0.38371% (+0.00728/wk)

- 1 Year +0.00357 to 0.69914% (+0.03743/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $260B

- Secured Overnight Financing Rate (SOFR): 0.05%, $935B

- Broad General Collateral Rate (BGCR): 0.05%, $358B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $338B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $1.799B accepted vs. $3.364B submission

- Next scheduled purchases:

- Thu 01/13 1010-1030ET: Tsy 2.25Y-4.5Y, appr $6.325B

- Thu 01/13 1500ET: Updated NY Fed Operational Purchase Schedule

FED Reverse Repo Operation

NY Fed reverse repo usage bounces to $1,536.981B (78 counterparties) vs. $1,527.020B on Tuesday.

Remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE: $2.2B RBC 4Pt Launched

$12.45B to Price Wednesday, puts total issuance over $53B tis week so far- Date $MM Issuer (Priced *, Launch #)

- 01/12 $3B #BNP Paribas $1.75B 6NC5 +110, $1.25B 11NC10 +140

- 01/12 $3B *World Bank $1B WNG 4Y SOFR+18, $2B 7Y SOFR+30

- 01/12 $2.5B #Florida Power & Light $1B 2NC.5 SOFR+38, $1.5B 10Y +73

- 01/12 $2.2B #Royal Bank of Canada $1B 3Y +42, $400M 3Y SOFR+44, $500M 5Y +57, $300M 5Y SOFR+71

- 01/12 $1.25B *Kommunalbanken Norway 5Y SOFR+27

- 01/12 $500M *JBIC WNG 5Y Green +33

- 01/12 $Benchmark Hyundai 3Y, 5Y investor calls

- Expected Thursday:

- 01/12 $Benchmark Province of Ontario 10Y +60a

EGBs-GILTS CASH CLOSE: Mixed Curve Movements Amid Broader Rally

Gilts and Bunds strengthened Wednesday, with mixed curve movements on display (German bull flattening, UK bull steepening).

- Little thematically to tie the moves together, though an in-line US CPI reading out in the afternoon led to a "buy the rumour, sell the fact" style rally across global core FI.

- The strength defied equity and oil price gains.

- German Bund auction (E1.3bln allotted) was the supply highlight this morning, with no top tier European data.

- Little on the data front Thursday either, though we get Irish and Italian supply.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.9bps at -0.587%, 5-Yr is down 2.4bps at -0.377%, 10-Yr is down 3.2bps at -0.059%, and 30-Yr is down 4bps at 0.251%.

- UK: The 2-Yr yield is down 3.4bps at 0.807%, 5-Yr is down 2.5bps at 0.978%, 10-Yr is down 3bps at 1.14%, and 30-Yr is down 2.4bps at 1.243%.

- Italian BTP spread down 1.2bps at 132.2bps / Spanish up 0.7bps at 68.6bps

FOREX: US Dollar Substantially Lower, Technicals Deteriorate

- Broadly in line US CPI data was not enough to support a struggling US dollar. Shortly after the release, the greenback significantly weakened with the Dollar index (DXY) reaching near two-month lows as we approach the NY close.

- The weakness has solidified the break below its 50-day moving average that had been underpinning price action of the index since October. Furthermore, and adding weight to the technical deterioration, the Bloomberg dollar index has recently breached its 100-day MA, an indicator that had not been intersected since June 2021.

- The softer greenback resulted in very strong one percent gains for the likes of CHF, AUD and NZD.

- Close on their heels was EURUSD which has broken some notable levelsat 1.1383/86, Nov 30 and Dec 31 highs. Clearance has prompted a stronger short-term recovery to the initial touted target of 1.1437, the top of a bear channel drawn from the Jun 1 high. The next notable resistance point resides at 1.1514, low Nov 5.

- CAD also picked up steam, following on from a stellar session on Tuesday. Oil prices continue to support the Canadian dollar recovery as well as multiple firms now forecasting rate lift-off as soon as the January meeting. USDCAD is close to support seen at 1.2493 (Nov 16 low) after which it would open 1.2448 (76.4% retracement of the Oct-Dec rally). Firm short-term resistance is 1.2726 (20-day EMA).

- The dollar weakness also exacerbated some recent strength in EMFX, with the South African Rand rallying 1.5% and TRY seen back in the limelight, advancing 4.5% throughout US trading.

- US PPI headlines Thursday’s data docket before potential comments from Fed’s Brainard - due to testify on the nomination of Vice Chair of the Federal Reserve Board of Governors before the Senate Banking Committee.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/01/2022 | 0101/0101 | ** |  | UK | IHS Markit/REC Jobs Report |

| 13/01/2022 | 0845/0845 | | UK | BOE Mann at EIB Conference | |

| 13/01/2022 | 0900/1000 | * |  | IT | industrial orders |

| 13/01/2022 | 1030/1130 |  | EU | ECB de Guindos at UBS Q&A | |

| 13/01/2022 | 1300/0800 |  | US | Philadelphia Fed's Patrick Harker | |

| 13/01/2022 | 1330/0830 | ** | | US | Jobless Claims |

| 13/01/2022 | 1330/0830 | *** | | US | PPI |

| 13/01/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 13/01/2022 | 1430/1530 | | EU | ECB Elderson at Climate Change Seminar | |

| 13/01/2022 | 1500/1000 | | US | Fed Brainard's Senate Nomination Hearing | |

| 13/01/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 13/01/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 13/01/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 13/01/2022 | 1700/1200 | | US | Richmond Fed's Tom Barkin | |

| 13/01/2022 | 1800/1300 | | US | Chicago Fed's Charles Evans | |

| 13/01/2022 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.