Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI STATE OF PLAY: BOE Hikes, Two Doves Dissent From Guidance

- ECB TO DISCUSS RATE HIKE AT JULY MEETING, HOLZMANN SAYS, Bbg

- BIDEN ADMIN WILL SEEK TO BUY 60M BARRELS OF CRUDE OIL: CNN

UK

BOE: The Bank of England raised its benchmark rate by 25 basis points as expected at its May meeting, but the Monetary Policy Committee split three ways as forecasts showed inflation continuing to rise even as growth falters, with two members dissenting from guidance that further tightening might be needed in coming months.

- The MPC's projections showed inflation peaking at just over 10% in October but also sliding back to 1.3% at the end of the three-year forecast for the biggest projected undershoot since the wake of the financial crisis. Output is expected to be nearly flat next year, assuming rates follow the market path.

- Such a divergence between the outlooks for near-term inflation and output divided the Committee even as it hiked Bank Rate to 1%.

US TSYS: The Fed is Not Dovish

FI markets broadly weaker after the bell, off second half lows after 30YY tapped 3.2066% high, 10YY comfortably above 3.0% to 3.1057%; yield curves bear steepening -- are off highs 2s10s +4.882 at33.703 vs. 37.390 high; 5s30s off inversion at 3.730 (+1.896).

- Little react to rise in weekly claims (+19k to 200Kk), modest drop in continuing claims (-0.019M to 1.384M), today's sell-off more in rates and stocks simply an unwind of the view the Fed is not less hawkish for choosing to not hike 75bs or provide guidance to that effect.

- With the FOMC and Tsy Refunding out of the way, markets have some clarity on the non-private sector's involvement in the long end and traders can focus on the still bearish fundamentals: duration risk / inflation etc. with the understanding the Fed is not coming to the rescue.

- Bear curve steepening is an interesting move since it implies confidence that the economy and the Fed will power through this cycle. While the 10Y move is driven mainly by real rates (new cycle high), NOT higher inflation expectations. Further steepening ahead w/ relatively few hikes and QT starting.

- That said, some focus on Friday's April employment data: +380k est vs. +431k prior and Average Hourly Earnings MoM (0.4% est); YoY (5.5% est).

OVERNIGHT DATA

US JOBLESS CLAIMS +19K TO 200K IN APR 30 WK

US PREV JOBLESS CLAIMS REVISED TO 181K IN APR 23 WK

US CONTINUING CLAIMS -0.019M to 1.384M IN APR 23 WK

US Q1 PREL UNIT LABOR COSTS +11.6% VS Q4 +1.0%; Y/Y +7.2%

US Q1 PREL NONFARM PRODUCTIVITY -7.5% VS Q4 +6.3%; Y/Y -0.6%

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 1059.73 points (-3.11%) at 33001.33

- S&P E-Mini Future down 148.25 points (-3.45%) at 4149

- Nasdaq down 647.2 points (-5%) at 12317.69

- US 10-Yr yield is up 10.4 bps at 3.0385%

- US Jun 10Y are down 29/32 at 118-8

- EURUSD down 0.0074 (-0.7%) at 1.0548

- USDJPY up 0.96 (0.74%) at 130.05

- WTI Crude Oil (front-month) up $0.43 (0.4%) at $108.29

- Gold is down $3.38 (-0.18%) at $1877.57

- EuroStoxx 50 down 28.36 points (-0.76%) at 3696.63

- FTSE 100 up 9.82 points (0.13%) at 7503.27

- German DAX down 68.3 points (-0.49%) at 13902.52

- French CAC 40 down 27.28 points (-0.43%) at 6368.4

US TSY FUTURES CLOSE

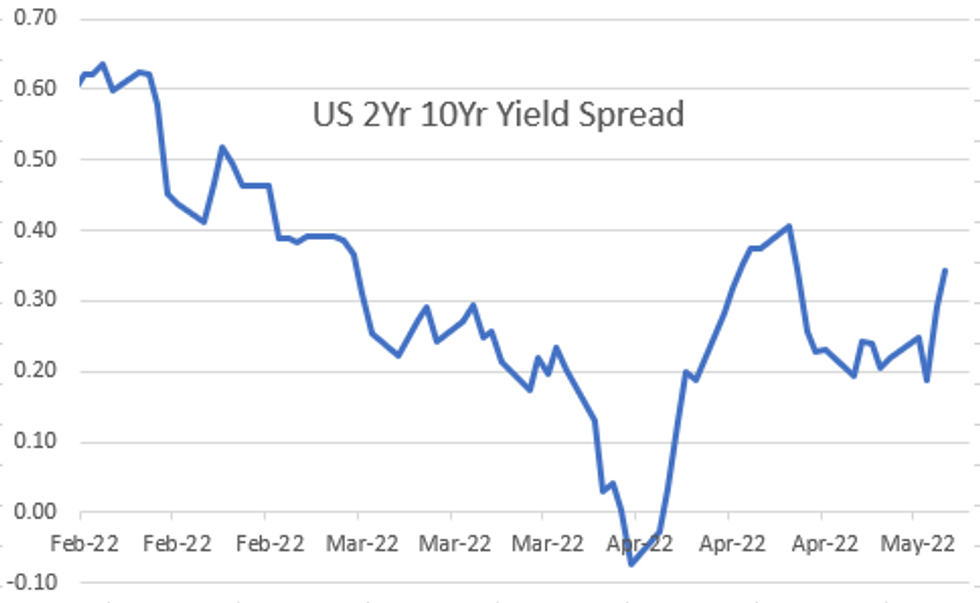

- 3M10Y +15.251, 219.522 (L: 203.222 / H: 224.825)

- 2Y10Y +4.073, 32.894 (L: 23.839 / H: 37.39)

- 2Y30Y +2.301, 41.051 (L: 31.394 / H: 47.714)

- 5Y30Y -0.415, 11.348 (L: 6.221 / H: 15.314)

- Current futures levels:

- Jun 2Y down 6.125/32 at 105-12.625 (L: 105-10.75 / H: 105-18.75)

- Jun 5Y down 17.25/32 at 112-10.5 (L: 112-03.75 / H: 112-30.5)

- Jun 10Y down 29.5/32 at 118-7.5 (L: 117-26 / H: 119-09.5)

- Jun 30Y down 2-14/32 at 137-23 (L: 136-19 / H: 140-03)

- Jun Ultra 30Y down 4-04/32 at 154-10 (L: 152-19 / H: 158-08)

US 10Y FUTURES TECH: (M2) Trend Conditions Remain Bearish

- RES 4: 122-02 50-day EMA

- RES 3: 122-12+ High Apr 4

- RES 2: 121-09 High Apr 14 and a reversal point

- RES 1: 119-28/120-18+ 20-day EMA / High Apr 27

- PRICE: 118-00@ 1430ET May 5

- SUP 1: 117-30+ Low May 5

- SUP 2: 117-29 1.0% 10-dma envelope

- SUP 3: 117-22+ Low Nov 8 2018 (cont)

- SUP 4: 116-28 0.764 proj of the Mar 7 - 28 - 31 price swing

Treasuries remain bearish. The contract traded lower Tuesday to probe support at 118-08, Apr 22 low and the bear trigger. This signals a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs. MA studies remain in a bear mode. Potential is seen for weakness towards 118-02+ next, a Fibonacci projection and 117-22+, the Nov 8 2018 low (cont). Key short-term resistance is unchanged at 120-18+.

US EURODOLLAR FUTURES CLOSE

- Jun 22 -0.005 at 98.145

- Sep 22 -0.010 at 97.315

- Dec 22 -0.060 at 96.795

- Mar 23 -0.090 at 96.535

- Red Pack (Jun 23-Mar 24) -0.115 to -0.105

- Green Pack (Jun 24-Mar 25) -0.105 to -0.09

- Blue Pack (Jun 25-Mar 26) -0.095 to -0.09

- Gold Pack (Jun 26-Mar 27) -0.105 to -0.10

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.48485 to 0.81514% (+0.48514/wk)

- 1M -0.00028 to 0.84486% (+0.04157/wk)

- 3M -0.03543 to 1.37071% (+0.03585/wk) ** Record Low 0.11413% on 9/12/21

- 6M -0.04743 to 1.97214% (+0.06143/wk)

- 12M -0.07629 to 2.67214% (+0.04357/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $77B

- Daily Overnight Bank Funding Rate: 0.32% volume: $273B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.30%, $947B

- Broad General Collateral Rate (BGCR): 0.30%, $359B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $344B

- (rate, volume levels reflect prior session)

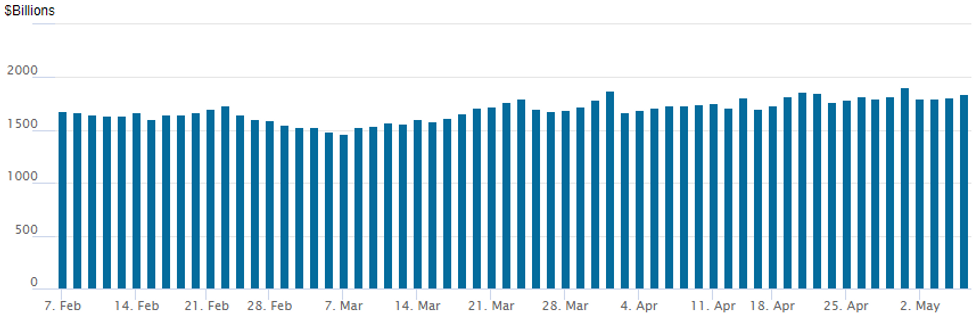

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage at 1,844.762B w/ 86 counterparties vs. prior session's 1,815.656B (all-time high of $1,906.802B on Friday, March 29, 2022).

PIPELINE: $4B Capital One 4Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 05/05 $4B #Capital One $1B 3NC2 +145, $350M 3NC2 SOFR+135, $1.55B 6NC5 +190, $1.1B 11NC10 +220

- 05/05 $1.725B #Southern Co $862.5M WNG 2Y +155, $862.5M WNG 5Y +200

- 05/05 $1.5B #Qualcomm $500M 10Y +120, $1B 30Y +145

- 05/05 $1.1B *Clorox $00M 7Y +138, $600M 10Y +158

- 05/05 $1B #Northern Trust 5Y +100

EGBs-GILTS CASH CLOSE: Dovish BoE Spurs UK Steepening

A dovish Bank of England meeting spurred a strong steepening in the UK yield curve as short-end yields fell sharply Thursday.

- But long-end yields underperformed in both the UK and Germany, defying a stock-selloff. One factor seen was ECB's Rehn saying the bank should hike rates in July and continue to raise gradually after that.

- With equities reversing sharply in the afternoon, peripheral spreads mostly widened: BTP 10Y / Bund closed just shy of 200bp for the 2nd straight day.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.4bps at 0.285%, 5-Yr is up 5.1bps at 0.766%, 10-Yr is up 7.3bps at 1.044%, and 30-Yr is up 9.1bps at 1.171%.

- UK: The 2-Yr yield is down 9.1bps at 1.547%, 5-Yr is down 5.7bps at 1.67%, 10-Yr is down 0.2bps at 1.964%, and 30-Yr is up 4.7bps at 2.125%.

- Italian BTP spread up 0.9bps at 199.5bps / Greek down 3.7bps at 240.8bps

FOREX: GBP Confirms Status as EM Currency

- Global risk off environment combined with renewed geopolitical risk have been weighing on 'risk-on' assets, including GBP.

- Historically, the British pound has been the weakest performing currency in high-volatility regime among the G10 world, averaging -30bps in monthly returns when VIX is trading above 20.

- The top chart shows the average monthly performance of the G9 currencies (vs. USD) when the VIX rises above 20 since January 1990 (VIX inception); the choice is arbitrary but a VIX higher than 20 has generally been defined as a 'high-volatility regime'.

- In addition, we have seen that GBP/USD has shown a strong co-movement with EM equities since the EU referendum in June 2016 (bottom chart).

- Therefore, the underperformance of theUK economy (relative to the US), rising recession risks (BoE raised flag today that UK is heading for a recession), vulnerable EM equities and persistent USD strength could continue to weigh on Sterling in the near to medium term.

- Cable broke back below its 1.25 support in today's trading session, which corresponds to the 61.8% Fibo retracement of the 1.1410 - 1.4250 range.

- Next support to watch on the downside stands at 1.2260 (June 2020 low).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/05/2022 | 2350/0850 | ** |  | JP | Tokyo CPI |

| 06/05/2022 | 0130/1130 |  | AU | RBA May SoMP | |

| 06/05/2022 | 0545/0745 | ** |  | CH | unemployment |

| 06/05/2022 | 0600/0800 | ** |  | DE | Industrial Production |

| 06/05/2022 | 0600/0700 | * |  | UK | Halifax House Price Index |

| 06/05/2022 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/05/2022 | 0730/0930 |  | SE | Riksbank Minutes April meet | |

| 06/05/2022 | 0800/1000 | * |  | IT | Retail Sales |

| 06/05/2022 | 0830/0930 | ** | | UK | IHS Markit/CIPS Construction PMI |

| 06/05/2022 | 1115/1215 | | UK | BOE Pill Monetary Policy Report National Agency briefing | |

| 06/05/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 06/05/2022 | 1230/0830 | *** |  | US | Employment Report |

| 06/05/2022 | 1315/0915 | | US | New York Fed's John Williams | |

| 06/05/2022 | 1400/1000 | * | | CA | Ivey PMI |

| 06/05/2022 | 1500/1600 | | UK | BOE Tenreyro Lecture at Irish Economic Association | |

| 06/05/2022 | 1500/1100 | | US | Minneapolis Fed's Neel Kashkari | |

| 06/05/2022 | 1900/1500 | * | | US | Consumer Credit |

| 06/05/2022 | 1920/1520 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.