Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

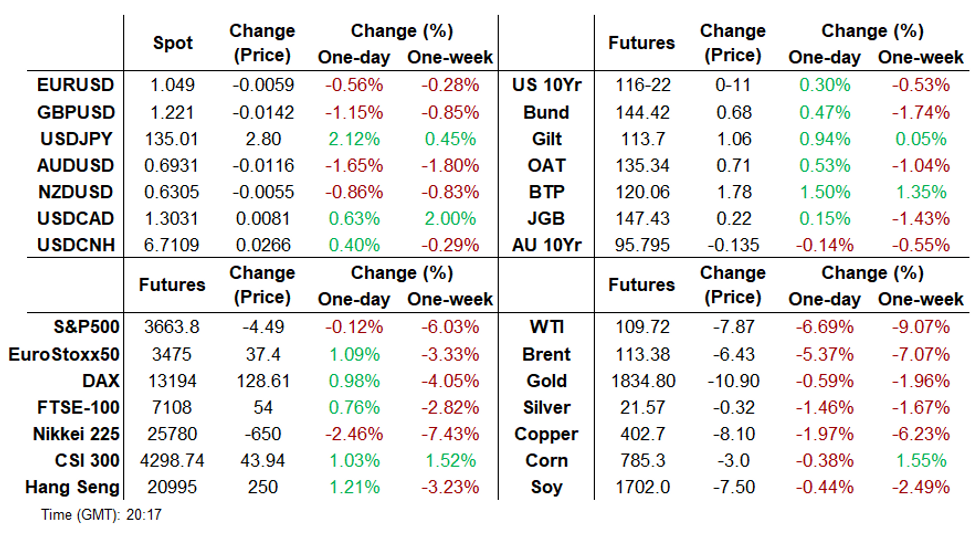

- USD Index Rises 1%, Recovering Thursday's Retreat

- Crude Futures Extend Decline Amid Demand Concerns

- Japanese Yen Plummets As BOJ Stay Easy

US TSYS: Falling Breakevens Help Cap Yield Gains

Treasuries traded weaker Friday, with a renewed rise in short-end yields bear flattening the curve.

- In a week dominated by big swings in Treasury yields and big equity declines, oil stole the show Friday, with WTI dropping 6.8% on the session.

- This helped 5Y and 10Y TIPS-implied breakevens fall to the lowest levels since February. In turn, that helped cap yield gains in an otherwise risk-on session, with the Nasdaq rallying in the afternoon.

- The 2-Yr yield is up 5.8bps at 3.1512%, 5-Yr is up 4.2bps at 3.326%, 10-Yr is up 2.9bps at 3.2237%, and 30-Yr is up 3.4bps at 3.2812%.

- Fed communications (George, Bullard, Kashkari) generally leaned hawkish where they leaned at all (nothing new from Chair Powell), helping pull short-end yields off session lows.

- Data (industrial production, leading index) added to the recent string of concerning reports but didn't draw any market reaction.

- With a market holiday Monday, attention will swiftly turn to Powell's congressional testimony next Weds and Thurs.

EGBs-GILTS CASH CLOSE: BTP Spreads Narrow As Volatility Pulls Back

EGBs saw fairly wide swings through Friday trade, though were ultimately bound within Thursday's ranges and with less volatility than in the prior two sessions.

- Core FI yields were directionless for most of the session, ultimately resolving lower toward the weekly close as equities and oil prices dropped along a strengthening USD.

- Periphery EGB spreads held their early narrowing on overnight comments by Lagarde nodded to the ECB containing spreads. Bunds bull steepened and outperformed Gilts.

- The UK curve twist flattened, with more BoE hike bets boosting 2Y yields.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 7.3bps at 1.094%, 5-Yr is down 8.6bps at 1.457%, 10-Yr is down 5.3bps at 1.661%, and 30-Yr is up 0.2bps at 1.851%.

- UK: The 2-Yr yield is up 8.9bps at 2.204%, 5-Yr is up 3.5bps at 2.207%, 10-Yr is down 1.9bps at 2.498%, and 30-Yr is down 0.8bps at 2.667%.

- Italian BTP spread down 9.7bps at 193.7bps / Greek down 18.6bps at 237bps

OPTIONS: Bobl Downside Profit Taking And Strangle Selling Feature Friday

Friday's Europe rates / bond options flow included:

- DUQ2 108.10/107.50 put spread vs 108.80 call bought for 7.5 in 3.5k

- RXQ2 152/154cs, bought for 11.5 in 2.5k

- RXU2 146/150/154 c fly, bought for 75 in 10k

- OEQ2 121.00p, sold from 100 to 87 in 12.5k (profit taking)

- OEQ2 118.5/124.5^^, sold from 83 to 65 in 12.5k

- SFIQ2 97.85/98.05/98.25 call fly bought for 2.25 in 4k

MNI BOE Review: 60% probability of a 50bp hike in August

- The forward-looking language was strengthened in four main ways, we discuss these in the full document.

- Markets are going even further by fully pricing a 50bp August hike with around a 25% probability of a 75bp hike. We think the debate for the MPC will be between 25bp and 50bp, and see very little chance of a larger than 50bp hike, irrespective of what other central banks do. Relative to the Fed and the ECB, the BOE’s position is different. These reasons are also discussed in the full report.

- Markets are going even further by fully pricing a 50bp August hike with around a 25% probability of a 75bp hike. We think the debate for the MPC will be between 25bp and 50bp, and see very little chance of a larger than 50bp hike, irrespective of what other central banks do. Relative to the Fed and the ECB, the BOE’s position is different.

- For the full document including the summaries of 22 sell-side analyst views see the full document here.

FOREX: USD Index Recovers 1%, JPY Continues Post-BOJ Selling

- The greenback traded on a much surer footing on Friday, with the USD Index reversing the majority of the dollar downtick seen Thursday.

- Initial weakness in equities extended the supportive USD price action during NY trade, weighing on the likes of the Euro and GBP. EURUSD faded to 1.0445 during this period, however, caught a bid as equities regained their poise approaching the close and looks to settle just south of 1.05.

- On the tech front – indicators remain bearish and the recent reversal lower signals a resumption of the primary downtrend with attention remaining on 1.0350, May 13 low.

- Following the BoJ rate decision overnight, JPY is the weakest currency in G10 as the central bank doubled down on their easy policy stance, effectively allowing markets to resume the selling pressure on the JPY. USDJPY printed 135.43, nearly 400 points above Thursday’s lows, before pulling back slightly into the close around the 135.00 mark.

- This week reinforces the bull trend and maintains the positive price sequence of higher highs and higher lows. Moving average studies also point north, reinforcing bullish conditions. The focus is on the 136.04, a Fibonacci projection.

- Risk sentiment remained shaky with initial downward pressure on global equity futures and a persistent grind lower in crude futures amid oil demand concerns. As a result, AUD (-1.62%) continues to slide, putting AUD/USD firmly below the $0.7000 handle. Additionally, AUDNZD has broken a couple of previous lows at 1.1033 exacerbating the relative AUD underperformance.

- On Monday, US holiday for Juneteenth National Independence Day. Despite a quiet data calendar, there may be potential comments from ECB’s Lagarde and Lane. Additionally, BOE’s Mann Panels an MNI Connect Event. Also Fed’s Bullard is due to discuss inflation and interest rates.

COMMODITIES: Oil Sharply Lower Amid Ongoing Demand Concerns

- Crude futures came under significant selling pressure on Friday amid weeklong concerns for demand outweigh the limited spare supply capacity.

- Other sources citing news of possible US restrictions on fuel exports and an upcoming trip to Saudi Arabia by President Biden may be adding to the selling pressure.

- Furthermore, this will be the first negative week for Brent prices in five, with potential profit taking dynamics in play amid ongoing recession fears heightening risk-off sentiment across global markets.

- WTI Crude down $8.55 or -7.27% at $111.63

- Natural Gas down $0.5 or -6.69% at $7.275

- Gold spot down $17.8 or -0.96% at $1846.59

- Copper down $8.65 or -2.1% at $403.8

- Silver down $0.31 or -1.4% at $21.6516

- Platinum down $21.69 or -2.27% at $937.75

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/06/2022 | 0100/0900 |  | CN | PBOC LPR announcement | |

| 20/06/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/06/2022 | 0800/0900 |  | UK | BOE Haskel Opening TechUK Policy Leadership Conference | |

| 20/06/2022 | 0900/1100 | ** |  | EU | Construction Production |

| 20/06/2022 | 1300/1500 | | EU | ECB Lagarde Intro at European Parliament | |

| 20/06/2022 | 1300/1400 | | UK | BOE Mann Panels MNI Connect Event | |

| 20/06/2022 | 1500/1700 | | EU | ECB Lagarde Intro as ESRB Chair at European Parliament | |

| 20/06/2022 | 1645/1245 |  | US | St. Louis Fed's James Bullard | |

| 20/06/2022 | 1700/1900 | | EU | ECB Panetta Interview with Federico Fubini at Nonfiction Festival | |

| 20/06/2022 | 1930/2130 | | EU | ECB Lane Speech at Society of Professional Economists |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok