Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed Sees July Rate Hike Of 75BPS Or 50 BPS, Minutes Show

- FED OFFICIALS AGREE OUTLOOK WARRANTS RESTRICTIVE STANCE

- FED: POSSIBILITY EVEN MORE RESTRICTIVE STANCE APPROPRIATE

- MNI INTERVIEW: US Service Prices May Have Peaked - ISM Chief

- IMF MANAGING DIRECTOR GEORGIEVA SAYS CAN'T RULE OUT POSSIBLE GLOBAL RECESSION IN 2023 - REUTERS INTERVIEW- Reuters

US

FED: Federal Reserve officials agreed at their June meeting, when they decided to raise interest rates by an unusually sharp 75 basis points, that another rate hike of either 75 basis points or 50 basis points was likely at the upcoming July meeting, minutes released Wednesday showed.

- "Participants judged that an increase of 50 or 75 basis points would likely be appropriate at the next meeting," the minutes said.

- The report offered no indication that officials see inflation as having peaked, and made no mention of recession prospects despite growing fears that one might be looming -- although it did acknowledge risks to growth. For more see MNI Policy main wire at 1401ET.

US: U.S. service sector prices could be past their peak as commodity and diesel costs fall and critical transportation price pressures ease, Institute for Supply Management services survey chief Anthony Nieves told MNI Wednesday, adding he expects growth to moderate through the year.

- "All indications are that we are easing on the inflation side," he said. "From what I'm seeing and from what respondents are telling us, we're seeing that inflation has maybe peaked."

- Prices in the June survey of service sector purchasing managers dipped to 80.1, down 2.0 points from May. The survey showed 66% of service firms reporting higher prices, down from 75% in April, while 2% registered lower prices. For more see MNI Policy main wire at 1217ET.

US TSYS: Stocks Gain, Little New Gleaned From June FOMC Minutes

Wide range for rates Wednesday, 30Y Bonds extended session lows ahead midday after blowing past early overnight highs after the NY open. Rates reacted to positive (non-recessionary) data, as 30YY fell below 3.0% briefly to 2.9926% low and have climbed steadily ever since to 3.1223% high.

- Underlying rate futures started to sell-off prior to final June services PMI (52.7 (FLSH 51.6; MAY 53.4), accelerated the sell-off after ISM June services composite Index came in stronger than expected as it only dipped to 55.3 (cons 54.0) from 55.9, contrary to the large miss in last week's manufacturing index, building on the upward revision seen in the final PMI just earlier.

- Little initial reaction to to June FOMC minutes release: "Participants judged that an increase of 50 or 75 basis points would likely be appropriate at the next meeting," the minutes said.

- Some see as potential for pause by year end helped stocks bounce: “Participants noted that, with the federal funds rate expected to be near or above estimates of its longer-run level later this year, the Committee would then be well positioned to determine the appropriate pace of further policy firming and the extent to which economic developments warranted policy adjustments.”

OVERNIGHT DATA

- US REDBOOK: JUN STORE SALES +12.3% V YR AGO MO

- US REDBOOK: STORE SALES +13.1% WK ENDED JUL 02 V YR AGO WK

- US FINAL JUN SERVICES PMI 52.7 (FLSH 51.6); MAY 53.4

- US ISM JUN SERVICES COMPOSITE INDEX 55.3

- US ISM JUN SERVICES BUSINESS INDEX 56.1

- US ISM JUN SERVICES PRICES 80.1

- US ISM JUN SERVICES EMPLOYMENT INDEX 47.4

- US ISM JUN SERVICES NEW ORDERS 55.6

- US BLS: JOLTS QUITS RATE 2.8% IN MAY

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 162.5 points (0.52%) at 31086.19

- S&P E-Mini Future up 26 points (0.68%) at 3856.5

- Nasdaq up 71.6 points (0.6%) at 11395.93

- US 10-Yr yield is up 11.9 bps at 2.9243%

- US Sep 10Y are down 31/32 at 118-30.5

- EURUSD down 0.0084 (-0.82%) at 1.0182

- USDJPY up 0.06 (0.04%) at 135.98

- WTI Crude Oil (front-month) down $0.92 (-0.92%) at $98.36

- Gold is down $23.35 (-1.32%) at $1738.25

- EuroStoxx 50 up 62.01 points (1.85%) at 3421.84

- FTSE 100 up 82.3 points (1.17%) at 7107.77

- German DAX up 193.32 points (1.56%) at 12594.52

- French CAC 40 up 117.42 points (2.03) at 5912.38

US TSY FUTURES CLOSE

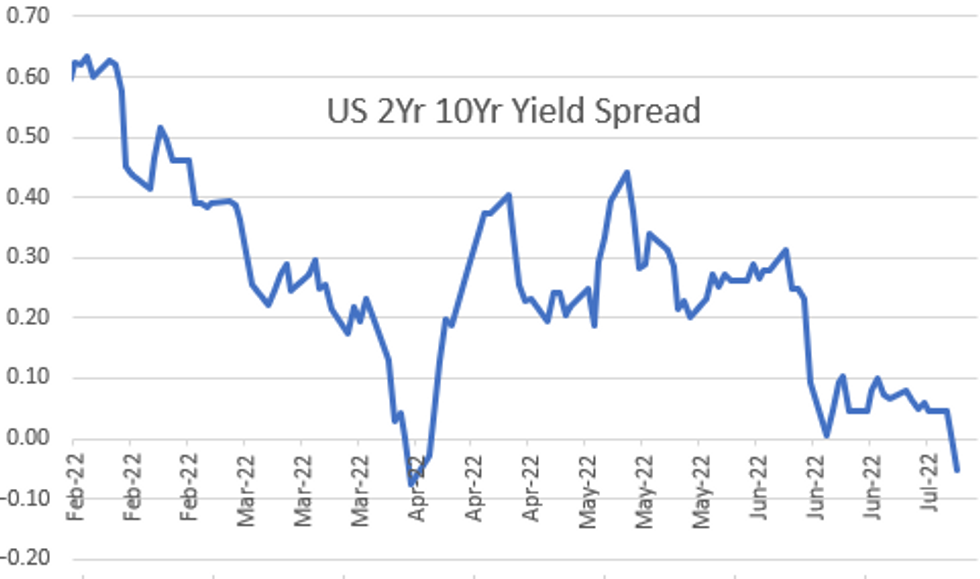

- 3M10Y -8.514, 101.271 (L: 82.595 / H: 108.428)

- 2Y10Y -3.898, -5.807 (L: -6.965 / H: 0.423)

- 2Y30Y -6.619, 14.898 (L: 14.239 / H: 23.619)

- 5Y30Y -5.905, 16.031 (L: 15.612 / H: 25.904)

- Current futures levels:

- Sep 2Y down 9.25/32 at 104-31.25 (L: 104-31.125 / H: 105-12.75)

- Sep 5Y down 22.75/32 at 112-16 (L: 112-16 / H: 113-19.25)

- Sep 10Y down 1-00.5/32 at 118-29 (L: 118-28.5 / H: 120-16.5)

- Sep 30Y down 1-22/32 at 139-15 (L: 139-13 / H: 142-06)

- Sep Ultra 30Y down 3-7/32 at 153-10 (L: 153-09 / H: 157-16)

US 10YR FUTURES TECHS: (U2) Bullish Outlook

- RES 4: 121-28+ 1.382 proj of the 14 - 23 - 28 price swing

- RES 3: 121-10 1.236 proj of the 14 - 23 - 28 price swing

- RES 2: 120-19+ High May 26 and a key resistance

- RES 1: 120-07 High Jul 5

- PRICE: 119-12 @ 15:47 BST Jul 6

- SUP 1: 118-19 50-day EMA

- SUP 2: 117-23+ 20-day EMA

- SUP 3: 116-11 Low Jun 28 and a key near-term support

- SUP 4: 115-20 Low Jun 17

Treasuries traded modestly lower into the Wednesday close, in a minor slowing of the recent bullish short-term cycle. A bullish theme remains in play following last week’s gains and resumption of the uptrend that started Jun 14. Price is also through the 50-day EMA. This signals scope for a continuation higher and attention is on 120-19+, the May 26 high. Key short-term support has been defined at 116-11, Jun 28 low. A break would highlight a bearish reversal.

US EURODOLLAR FUTURES CLOSE

- Sep 22 -0.060 at 96.755

- Dec 22 -0.10 at 96.305

- Mar 23 -0.140 at 96.40

- Jun 23 -0.180 at 96.580

- Red Pack (Sep 23-Jun 24) -0.21 to -0.20

- Green Pack (Sep 24-Jun 25) -0.20 to -0.165

- Blue Pack (Sep 25-Jun 26) -0.145 to -0.105

- Gold Pack (Sep 26-Jun 27) -0.10 to -0.085

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00100 to 1.56243% (-0.00486/wk)

- 1M +0.01586 to 1.80686% (+0.00929/wk)

- 3M +0.04228 to 2.39057% (+0.09771/wk) * / **

- 6M +0.03229 to 2.99886% (+.09957/wk)

- 12M -0.03829 to 3.55400% (-0.01029/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3Y high: 2.39057% on 7/6/22

- Daily Effective Fed Funds Rate: 1.58% volume: $94B

- Daily Overnight Bank Funding Rate: 1.57% volume: $262B

- Secured Overnight Financing Rate (SOFR): 1.54%, $1.042T

- Broad General Collateral Rate (BGCR): 1.51%, $362B

- Tri-Party General Collateral Rate (TGCR): 1.50%, $349B

- (rate, volume levels reflect prior session)

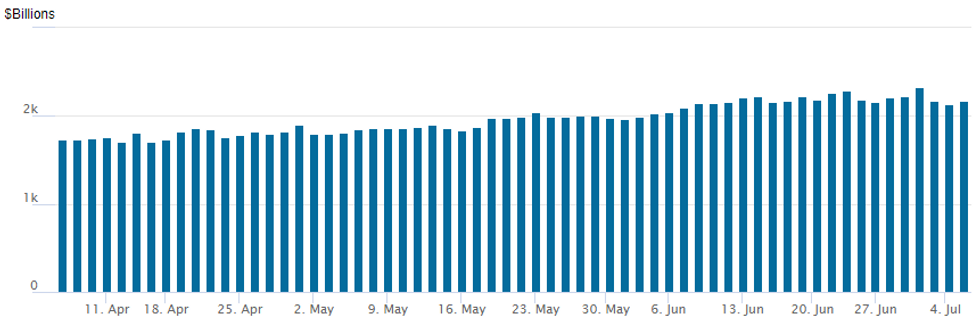

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,168.026B w/ 96 counterparties vs. $2,138.280B prior session. Record high stands at $2,329.743B from Thursday June 30.

EGBs-GILTS CASH CLOSE: Gilts Underperform Amid Political Drama

Wednesday saw a fresh bout of recessionary-fear-fuelled rallies in core FI for most of the session, though yields reversed higher from mid-afternoon onward.

- It was a day of high drama in UK politics with PM Johnson seemingly under pressure to resign as we headed to the cash close, though political risk was very much a sideshow to global macro considerations.

- UK yields ended higher, with bear flattening in the curve: BoE's Pill and Cunliffe suggested they'd be willing to pursue faster rate hikes.

- German bonds outperformed with the curve twist steepening; periphery EGB spreads finished a little tighter after early widening.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 3.9bps at 0.393%, 5-Yr is down 4.8bps at 0.822%, 10-Yr is up 2.9bps at 1.208%, and 30-Yr is up 2.8bps at 1.525%.

- UK: The 2-Yr yield is up 7.4bps at 1.757%, 5-Yr is up 3.8bps at 1.75%, 10-Yr is up 4.7bps at 2.096%, and 30-Yr is up 7.7bps at 2.541%.

- Italian BTP spread down 3.1bps at 194.6bps / Spanish down 3.4bps at 107.3bps

FOREX: Power Prices Continue to Drill EUR Lower

- The power crunch across Europe continues to send recession jitters throughout Eurozone assets, with EUR/USD respecting the deep-seated downtrend channel drawn off the February highs to print a new cycle low Wednesday. Continued upheaval in gas and oil markets put German energy futures at fresh record levels, prompting a further pullback in year-end ECB policy rate expectations, which now imply a deposit rate of less than 0.75% - a near 50bps reversal off the levels seen in mid-June. EUR/USD's new low at 1.0162 marks the weakest level since 2002 for the pair.

- Political tumult continued to roil UK markets, with GBP/USD weaker as traders watch for what seems like the imminent resignation of the Prime Minister. That said, GBP fared generally well against the likes of the EUR, AUD and NZD - indicating that uncertainty surrounding UK governmental policy has been well priced in after a volatile few weeks for Boris Johnson. GBP/USD printed a new YTD low at 1.1876, but traded at the week's best levels against the EUR during the Wednesday session.

- JPY was the main beneficiary of the risk-off backdrop, rising against all others in G10. AUD/JPY eyes support at last week's lows of Y91.43 ahead of the 100-dma of Y90.72.

- Focus Thursday turns to the weekly US jobless claims releases as well as German industrial production and Canada's Ivey PMI. Central bank events include the release of the ECB's meeting accounts as well as speeches from ECB's Lane, Stournaras and Centeno as well as Fed's Waller and Bullard.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/07/2022 | 0130/1130 | ** |  | AU | Trade Balance |

| 07/07/2022 | 0545/0745 | ** |  | CH | unemployment |

| 07/07/2022 | 0600/0800 | ** |  | DE | Industrial Production |

| 07/07/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 07/07/2022 | 0945/1145 |  | EU | ECB Lane on Green Transition at OECD Forum | |

| 07/07/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 07/07/2022 | 1230/0830 | ** | | US | Trade Balance |

| 07/07/2022 | 1300/1400 |  | UK | BOE Mann Speaks at LC-MA Forum | |

| 07/07/2022 | 1400/1000 | * |  | CA | Ivey PMI |

| 07/07/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 07/07/2022 | 1500/1100 | ** | | US | DOE weekly crude oil stocks |

| 07/07/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 07/07/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/07/2022 | 1605/1705 | | UK | BOE Pill Speaks at Sheffield Hallam University | |

| 07/07/2022 | 1700/1300 | | US | Fed Governor Christopher Waller | |

| 07/07/2022 | 1700/1300 | | US | St. Louis Fed's James Bullard |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.