Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Executive Summary:

- Fed's Daly indicates openness to accelerating a taper

- FOMC minutes discussed faster QE taper

- Shallow Fed Hiking Path Seen Likely, Could Turn Higher, according to former Fed economists

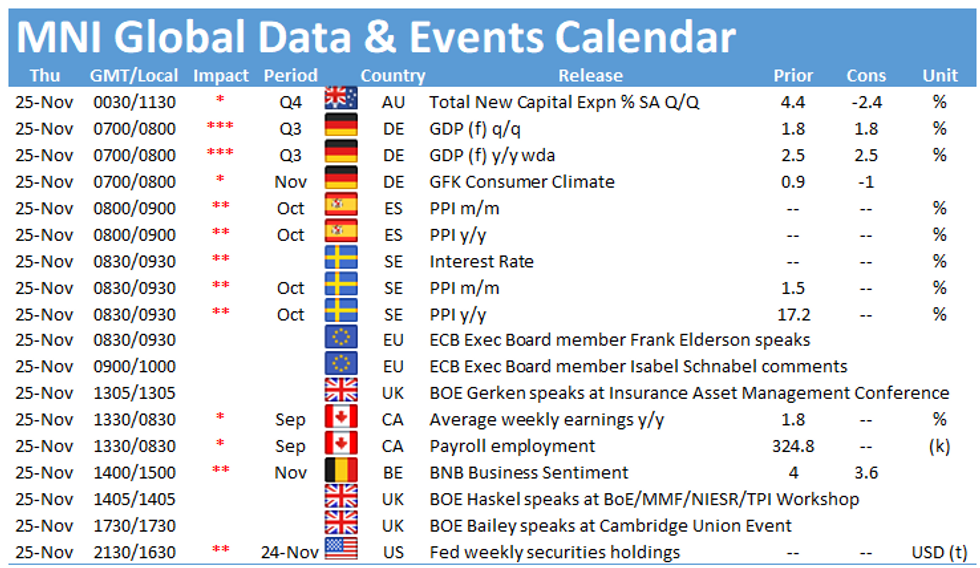

- Thanksgiving holidays see sporadic market opens Thursday

Figure 1: US 2y30y Spread drops to new post-pandemic low

AMERICAS

US (MNI): Fed Discussed Faster QE Taper in Nov Meeting Minutes

The Federal Reserve debated speeding up tapering asset purchases at its November meeting as policymakers considered how soon they may need to raise interest rates to combat rising inflation, minutes from the meeting showed. "Some participants preferred a somewhat faster pace of reductions that would result in an earlier conclusion to net purchases," the report said. "Some participants suggested that reducing the pace of net asset purchases by more than $15 billion each month could be warranted so that the Committee would be in a better position to make adjustments to the target range for the federal funds rate, particularly in light of inflation pressures." Since then, several Fed officials have come out in favor of a faster taper.

US (MNI): Shallow Fed Hiking Path Seen Likely, Could Turn Higher

The Federal Reserve is likely to begin its rate hiking cycle next year with the assumption that only a couple of increases are needed to break inflation momentum, but there are risks it may need to tighten further in order to cement price credibility with markets and consumers, former Fed economists told MNI.

US (Bloomberg): Daly Says She'd Support Faster Fed Tapering If Data Stay Strong

It will be hard to argue the Federal Reserve shouldn't speed up the process of scaling back its bond-buying if reports on the labor market and consumer prices due out early next month show continued strength, San Francisco Fed President Mary Daly said. "It looks like the jobs market is really continuing to fire on all the cylinders for hiring," Daly said in a Yahoo! Finance interview published Wednesday. "The inflation numbers, after coming down for a few months on the monthly basis, the CPI monthly numbers were high again," she said, referring to the Labor Department's consumer price index reading for the month of October.

EUROPE

EUROPE (MNI) Average M/T Eurozone Infl May Be Above 2%: Weidmann

Flexibility, a key feature of the ECB's pandemic emergency purchase programme, should not to transferred to the central bank's other bond-buying programmes, Bundesbank chairman Jens Weidmann said in a speech Wednesday, with headline German inflation to hit 6% and 3% by the end of next year.

EUROPE (MNI) ECB Needs Limited,Flexible PEPP Successor-Kazaks

The successor to the European Central Bank's Pandemic Emergency Purchase Programme should be limited in size and duration but used flexibly, Bank of Latvia Governor Martins Kazaks told MNI. The PEPP's active phase can end as planned in March 2022, Kazaks said in an interview, with the worst of the economic impact of the Covid-19 pandemic beginning to fade and GDP growth set to continue at a decent rate at least over the medium-term forecast horizon, barring sudden macroeconomic shocks.

EUROPE (MNI): Covid Pandemic May Not Be Over - ECB's Panetta

Europe's Covid-19 pandemic may not be over yet, ECB Executive Board member Fabio Panetta said in a speech Wednesday, as he urged monetary policymakers to remain patient, while staying vigilant to both upside and downside risk to the recovery and to the medium-term inflation outlook.

UK (MNI): BOE Tenreyro Sees Bank Rate At Pre-Crisis Level

Bank of England Monetary Policy Committee member Silvana Tenreyro said Wednesday that she envisaged that Bank Rate, currently at 0.1%, would at some point return to its pre-Covid crisis level. Bank Rate was at 0.75% before Covid struck but markets have been pricing in a move by the autumn to just above 1.0%. Speaking at an Oxford University Economic Society event Tenreyro said "Directionally ... I would expect a modest tightening to restore inflation to target," adding that there were "pros and cons" over whether the first hike should come in December or February.

DATA

MNI: US OCT PERSONAL INCOME +0.5%; NOM PCE +1.3%

US OCT PCE PRICE INDEX +0.6%; +5.0% Y/Y

US OCT CORE PCE PRICE INDEX +0.4%; +4.1% Y/Y

US OCT UNROUNDED PCE PRICE INDEX +0.632%; CORE +0.425%

US JOBLESS CLAIMS -71K TO 199K IN NOV 20 WK

US PREV JOBLESS CLAIMS REVISED TO 270K IN NOV 13 WK

US CONTINUING CLAIMS -0.060M to 2.049M IN NOV 13 WK

US OCT DURABLE NEW ORDERS -0.5%; EX-TRANSPORTATION +0.5%

US SEP DURABLE GDS NEW ORDERS REV TO -0.4%

US OCT NONDEF CAP GDS ORDERS EX-AIR +0.6% V SEP +1.3%

US Q3 GDP +2.1%

US TSYS SUMMARY: Daly Taper Comments Dominate, Not Minutes

Tysy saw minimal reaction to the Fed minutes, with moves instead coming earlier in the day after a hawkish surprise from one of the more dovish Fed members, Daly.

- Tsys had very little reaction to the Fed minutes, as the fact that some members supported faster tapering was usurped by Daly earlier indicating her bar for accelerating taper is low.

- This saw a twist flattening after the earlier sell-off into US data. 2Y yield is +2.6bps at 0.640%, 5Y is +0.2bps at 1.341%, 10Y is -2.1bps at 1.644% and the 30% is -5.1bps at 1.972%.

- TYZ1 has picked up from earlier session/month lows and is back at 129-27 on low volumes. It steered clear of any test of nearby support at 129-03 (50% of the Oct'18 - Mar'20 bull cycle) but equally is some way from the key short-term resistance level of 131-08.

- Demand for the Fed's o/n reverse repo facility fell by the most since Nov 1, to $1.453T from $1.572T yesterday, more than the $50B flagged beforehand by Wrightson ICAP from GSEs exiting the market.

- It's Thanksgiving tomorrow with no US data/auctions for the rest of the week. Cash Tsys will close early on Friday at 1315ET/1815GMT.

FOREX: US Dollar Rally Extends, NZDUSD Sinks To 3-Month Low

- Gradual and persistent dollar buying was the order of the day on Wednesday ahead of the FOMC minutes and the US Thanksgiving holiday tomorrow. The dollar index rose another 0.4%, extending the week's gains to just shy of 1%. The minutes from the November Fed meeting had little impact on currency markets following the release.

- EURUSD continued its downward trajectory, falling below 1.12 for the first time since July 2020 and meeting a minor support at 1.1185. The move lower continues to cement the downtrend and price is trading below the base of the bear channel drawn from the Jun 1 high.

- Conversely, USDJPY climbed to fresh highs above the March 2017 highs of 115.51. The next target would be 116.09, the 1.764 proj of Apr 23 - Jul 2 - Aug 4 price swing.

- A 25bp rate hike and updated RBNZ guidance fell below market expectations, prompting a fourth consecutive day of losses for the New Zealand dollar. Kiwi was bottom of the G10 pile on Wednesday with greenback strength exacerbating the move lower. NZDUSD trades down 1.15%, briefly reaching a three-month low.

- In emerging markets, the Turkish Lira came roaring back following Tuesday's collapse. There was another huge range for USDTRY (11.5871-13.1667) amid continued poor liquidity, however, Wednesday saw the Lira recover and settle around 7% in the green. MXN was the notable underperformer, losing nearly 2% amid a new central bank governor announcement. USDMXN came within touching distance of the years highs before settling around +1% for the session.

- With the US out tomorrow for Thanksgiving, markets are expected to have a subdued tone. The focus should fall on the ECB Minutes and any commentary from scheduled speakers - ECB's LaGarde and BOE's Bailey.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.