Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US

FED: The Federal Reserve boosted interest rates by a quarter percentage point Wednesday as many investors expected and said more increases are likely, but the FOMC also indicated it is watching for signs the recent banking crisis will tighten credit conditions.

- The Fed raised the federal funds rate target range to 4.75% to 5%, the highest since 2007, but indicated future hikes might depend on the effects of the recent financial turmoil on the economic outlook.

- "Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation,” the Fed said in its statement. "The extent of these effects is uncertain."

- “The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time.” For more see MNI Policy main wire at 1400ET.

FED: Federal Reserve Chair Jerome Powell told reporters Wednesday the FOMC considered stopping its rate hikes this week but decided on another quarter point hike instead.

- “We did consider that in the days running up to the meeting. So our decision was to move ahead with the 25-basis point hike and change our guidance as I mentioned from ongoing hikes to some additional hikes maybe -- policy firming may be appropriate," he said.

FED: The inflation fight is far from over because price pressures are too elevated for the Federal Reserve’s liking, Chair Jerome Powell said Wednesday.

- “The process of getting inflation back down to 2% has a long way to go and is likely to be bumpy,” Powell said. “Inflation has moderated somewhat since the middle of last year, but the strength of these recent readings indicates that inflation pressures continue to run high.” (See MNI INTERVIEW: Americans' Top Concern Remains Inflation-Umich)

CANADA

BOC: Bank of Canada officials worried about sticky price and wage gains and elevated inflation expectations even while pausing interest-rate hikes without actively debating a ninth straight increase, the March 8 decision minutes published Wednesday showed.

- Officials "remain concerned about the risk that inflation could get stuck materially above the 2% target" and the press release should stress "the conditionality of the pause" with upside risks more concerning, the minutes showed. Governor Tiff Macklem and his deputies agreed their outlook for slowing growth and inflation remained on track, justifying a pause to assess how rate hikes would bring demand back in line with supply.

- "Short-term inflation expectations are higher than in the Bank’s own inflation forecast. If they do not come down, high inflation will be stickier than expected," the minutes showed. Wage growth between 4% and 5% was also too hot and must moderate through some combination of slower gains and a turnaround of weak productivity, Governing Council members found. For more see MNI Policy main wire at 1331ET.

US TSYS: Bonds Near Highs After Fed Delivers Expected 25Bp Hike

- Treasury futures extending highs after the bell, yield curves steeper as short end rates outpace bonds after the Federal Reserve delivered a second consecutive and widely anticipated 25bp hike. Though signaling additional hikes, the Fed statement was largely deemed dovish in it's efforts to stem inflation.

- After an initial knee-jerk rally and price pull-back, Tsys rebounded as Chairman Powell stressed the Fed is "no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation. Instead, we now anticipate some additional policy firming may be appropriate."

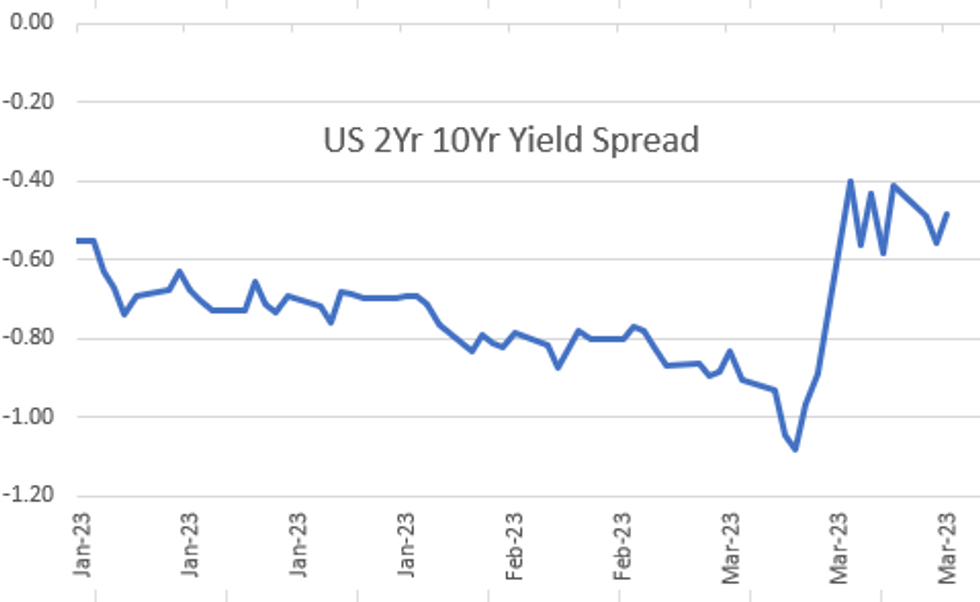

- Yield curves forged steeper with 2s10s hitting -45.799 high before settling back to around -50.164 with short end outperforming, TUM3 +15 at 103-18.

- Implied hikes evaporate despite the Fed flagging additional 25bp hikes. Snapshot of current levels after the second consecutive 25bp hike:

- Fed funds implied hike for May'23 11.1, Jun'23 cumulative 0.3bp to 4.815%, Jul'23 slips to -20.0bp to 4.623%. Fed Terminal currently at 4.925% in May'23. Implied rate cuts accelerate by year end with Dec'23 cumulative -66.2 at 4.150.

OVERNIGHT DATA

- US MBA: REFIS +5% SA; PURCH INDEX +2% SA THRU MARCH 17 WK

- US MBA: UNADJ PURCHASE INDEX -36% VS YEAR-EARLIER LEVEL

- US MBA: 30-YR CONFORMING MORTGAGE RATE 6.48% VS 6.71% PREV

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 191.34 points (-0.59%) at 32365.61

- S&P E-Mini Future down 16.75 points (-0.42%) at 4019

- Nasdaq down 26 points (-0.2%) at 11832.58

- US 10-Yr yield is down 13.6 bps at 3.4734%

- US Jun 10-Yr futures are up 36.5/32 at 115-8.5

- EURUSD up 0.0105 (0.98%) at 1.0873

- USDJPY down 1.17 (-0.88%) at 131.33

- Gold is up $27.36 (1.41%) at $1967.43

- EuroStoxx 50 up 14.1 points (0.34%) at 4195.7

- FTSE 100 up 30.62 points (0.41%) at 7566.84

- German DAX up 20.85 points (0.14%) at 15216.19

- French CAC 40 up 18.21 points (0.26%) at 7131.12

US TREASURY FUTURES CLOSE

- 3M10Y -19.242, -130.503 (L: -131.585 / H: -112.044)

- 2Y10Y +7.496, -48.844 (L: -63.725 / H: -45.799)

- 2Y30Y +15.476, -28.593 (L: -51.578 / H: -24.139)

- 5Y30Y +15.301, 13.361 (L: -5.114 / H: 15.593)

- Current futures levels:

- Jun 2-Yr futures up 14.25/32 at 103-17.25 (L: 102-29.75 / H: 103-19.625)

- Jun 5-Yr futures up 30.75/32 at 109-27.75 (L: 108-21.25 / H: 109-31.25)

- Jun 10-Yr futures up 1-07/32 at 115-09 (L: 113-26 / H: 115-14.5)

- Jun 30-Yr futures up 1-07/32 at 131-07 (L: 129-08 / H: 131-14)

- Jun Ultra futures up 1-11/32 at 141-19 (L: 139-08 / H: 142-06)

US 10YR FUTURE TECHS: Pulls Lower Pre-Fed

- RES 4: 117-14+ High Aug 29 / 30 2022 (cont)

- RES 3: 117-00 61.8% of the Aug - Oct 2022 bear leg (cont)

- RES 2: 116-28+ High Jan 19 and key resistance

- RES 1: 115-14+/116-24 High Mar 21 / 20

- PRICE: 114-08 @ 16:29 GMT Mar 22

- SUP 1: 113-26 Low Mar 22

- SUP 2: 113-13 50-day EMA

- SUP 3: 112-21 Low Mar 13

- SUP 4: 111-28+ 76.4% retracement of the Mar 2 - 20 rally

Treasury futures printed a lower low at 113-26 ahead of the Wednesday Fed decision, putting prices briefly below 114-01+, the Mar 17 low, although firmer support is seen into 113-13, the 50-day EMA. A break of this average is required to signal a stronger reversal. For bulls, a move higher higher would once again refocus attention on the key resistance zone between 116-24, Monday’s high and 116-28+, the Jan 19 high. This zone is a bull trigger.

EURODOLLAR FUTURES CLOSE

- Jun 23 +0.020 at 94.835

- Sep 23 +0.125 at 95.265

- Dec 23 +0.205 at 95.595

- Mar 24 +0.285 at 96.020

- Red Pack (Jun 24-Mar 25) +0.275 to +0.320

- Green Pack (Jun 25-Mar 26) +0.230 to +0.260

- Blue Pack (Jun 26-Mar 27) +0.150 to +0.215

- Gold Pack (Jun 27-Mar 28) +0.080 to +0.130

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00200 to 4.55857% (-0.00229/wk)

- 1M +0.01771 to 4.79700% (+0.01929/wk)

- 3M +0.06229 to 5.08000% (+0.08157/wk)*/**

- 6M +0.10857 to 5.11514% (+0.06285/wk)

- 12M +0.18258 to 5.17929% (+0.14515/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.15371% on 3/9/23

- Daily Effective Fed Funds Rate: 4.58% volume: $92B

- Daily Overnight Bank Funding Rate: 4.57% volume: $278B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.247T

- Broad General Collateral Rate (BGCR): 4.52%, $515B

- Tri-Party General Collateral Rate (TGCR): 4.52%, $502B

- (rate, volume levels reflect prior session)

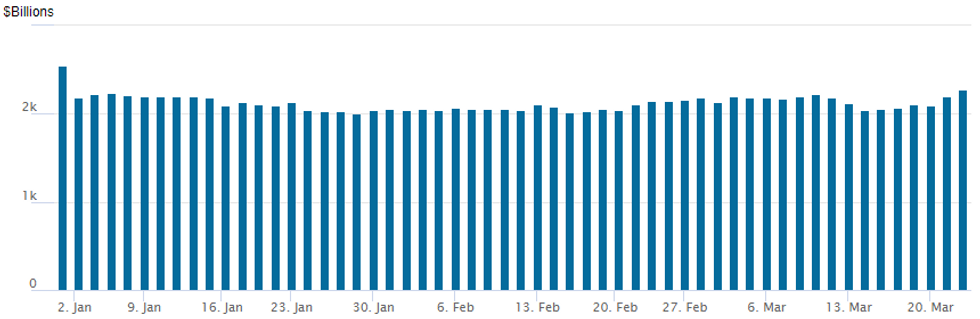

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to new 2023 high of $2,279.608B w/ 104 counterparties vs. prior session's $2,.194.631B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

PIPELINE: Issuers Back on Sidelines

Issuers back on the sidelines to await the FOMC after issuing $7.1B Tuesday- Date $MM Issuer (Priced *, Launch #)

- 03/21 $1.8B *Republic of Panama $800M 2035 tap +255.5, $1B 31Y +312.5

- 03/21 $1.2B *Republic Services $400M 6Y +120, $800M 11Y +145

- 03/21 $1B *Metropolitan Life 10Y +158

- 03/21 $750M *NiSource 5Y +155

- 03/21 $650M *Brown-Forman 10Y +120

- 03/21 $500M *Extra Space Storage5Y +200

- 03/21 $500M *Duke Energy Indiana WNG 30Y +170

- 03/21 $500M *Indiana Michigan Power WNG 30Y +190

EGBs-GILTS CASH CLOSE: Strong UK CPI Boosts BoE Hike Prospects

The UK curve bear flattened sharply Wednesday as a stronger-than-expected February CPI reading boosted implied BoE tightening.

- A jump in February services inflation was the highlight of the CPI beat, and led BoE terminal hike pricing jumped over 30bp, with around 68bp of further increases seen to a September peak. A 25bp hike Thursday is now 92% priced.

- Despite closing 5bp below session highs, 2Y UK yields increased by the most in a single session since September on the higher BoE rate pricing.

- The German curve also bear flattened, mirroring the UK move but by a lesser degree (unsurprising given Tues saw the biggest Schatz selloff in 15 years).

- The bearish moves peaked by early afternoon trade, pulling back thereafter with the Federal Reserve rate decision awaited an hour after the cash close.

- EGB periphery spreads were mixed on the session, with BTPs underperforming.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 9bps at 2.707%, 5-Yr is up 6bps at 2.372%, 10-Yr is up 3.6bps at 2.328%, and 30-Yr is up 0.4bps at 2.323%.

- UK: The 2-Yr yield is up 21.6bps at 3.494%, 5-Yr is up 15.8bps at 3.374%, 10-Yr is up 8.4bps at 3.451%, and 30-Yr is up 4.4bps at 3.886%.

- Italian BTP spread up 1.8bps at 184.2bps / Spanish down 0.1bps at 103.9bps

FOREX: Greenback Extends Weakness Following FOMC Decision

- A dovishly perceived hike from the Federal Reserve was enough to build the momentum for a weaker dollar on Wednesday, with the USD index (-0.85%) extending to the lowest level since February 03.

- With the Fed statement and the latest summary of economic projections leaning dovish, the greenback came under immediate pressure, from which it did not recover.

- EURUSD is the strongest performing major in G10, currently up 1.02% as we approach the APAC crossover. An immediate spike above the 1.08 handle sparked a wave of demand that saw the pair trade as high as 1.0912.

- This closely tied with noted resistance at 1.0911, the 76.4% retracement of the Feb 2 - Mar 15 bear leg, holding well during the press conference with Powell’s reiteration that the Fed are prepared to hike above expectations then aiding the brief bounce for the greenback.

- However, after dipping to 1.0853, EURUSD continues to trade buoyantly and is approaching the 1.09 handle once more. Further greenback weakness overnight will pave the way for a move to 1.1033, the Feb 2 high and key resistance for the pair.

- The initial bounce in equities saw the likes of AUD and NZD extend gains well over 1% on the session. However, with major indices sliding back into the red, Antipodean FX surrendered a portion of these gains into the close. USDJPY (-0.96%) is also trading heavily as we approach the end of the US session, narrowing the gap with the week's lows at 130.54.

- More central bank fun on Thursday as the SNB and Norges Bank kick proceedings off. Focus then turns to the Bank of England, who is widely expected to hike rates after the above expectation CPI data earlier today.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/03/2023 | 0830/0930 |  | CH | SNB interest rate decision | |

| 23/03/2023 | 0900/1000 | *** |  | NO | Norges Bank Rate Decision |

| 23/03/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 23/03/2023 | 1200/1200 | *** |  | UK | Bank Of England Interest Rate |

| 23/03/2023 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 23/03/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 23/03/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 23/03/2023 | 1230/0830 | * | | US | Current Account Balance |

| 23/03/2023 | 1400/1000 | *** | | US | New Home Sales |

| 23/03/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 23/03/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 23/03/2023 | 1500/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 23/03/2023 | 1500/1600 | | EU | ECB Lane Panels Peterson Institute Conference | |

| 23/03/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 23/03/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 23/03/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 24/03/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.