Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US: Yellen: "US Economy On Path To Soft Landing"

- MNI EU: Hungary Willing To Drop Ukraine Funding Veto If All EU Funds Released

- MNI Ukrainian President Volodymyr Zelenskyy Petitions Congress For Support

- MNI SECURITY: NSA Sullivan: Biden Won't Accept GOP Holding Ukraine Aid "Hostage"

- MNI US-ISRAEL: Biden: "Netanyahu Has To Change His Government"

- Alphabet Falls as Google Loses Antitrust Battle: Street Wrap, Bbg

US TSYS Ylds Lower Ahead FOMC, Bond Sale Stops Through, Core CPI Accelerates

- Currently, March'24 30Y futures trading at 119-15 (+15) -- still off this morning's post-CPI high of 120-09; March'24 10Y futures +7.5 at 110-18 vs 110-31.5 high. Initial technical resistance of 111-09+ (High Dec 7 and bull trigger) still intact.

- Curves holding flatter profiles (2Y10Y -4.955 at -52.848) with bonds outperforming since the $21B 30Y reopen sale stopped .3bp through: 4.344% vs. 4.347% WI.

- Trading desks had reported leveraged$ selling of CT30, real$ accounts selling off-the-run 30s into the post data rally, while unwinds of pre-auction short sets contributing to the post-auction bounce.

- Focus turns to Wednesday morning's PPI: MoM (-0.5%, 0.0%), YoY (1.3%, 1.0%), and of course the FOMC rate annc and SEP at 1300ET followed by Chairman Powell's presser at 1430ET.

- The Fed will likely lower its median "dot plot" estimate for policy interest rates at the end of 2024 to around 4.9%, former officials and staffers told MNI, as expectations build for the first rate cut to come as early as the first half of the year.

- "My expectation is that the median will probably show two 25-basis-point cuts next year," said ex-Boston Fed chief Eric Rosengren, whose own forecast is for two to three cuts starting as early as the second quarter.

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00505 to 5.36483 (+0.00480/wk)

- 3M +0.00689 to 5.38606 (+0.02002/wk)

- 6M +0.01714 to 5.32936 (+0.05439/wk)

- 12M +0.03258 to 5.13074 (+0.11062/wk)

- Secured Overnight Financing Rate (SOFR): 5.32% (+0.00), volume: $1.577T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $614B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $600B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $102B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $258B

FED: RRP Usage Near Unchanged Despite Jump In Counterparties

- RRP usage was near unchanged today at $838B (-$1B) for still close to last week’s average of $829B.The recent low still stands at $769B on Dec 1.

- The mostly flat move on the day is despite the number of counterparties jumping from 82 (a joint low that was last lower in Apr-2022) to 97 (highest since Nov 22).

SOFR/TREASURY OPTION SUMMARY

Mixed trade on modest volumes overnight, active desks close to the sidelines ahead of this morning's CPI, PPI and FOMC tomorrow. Underlying futures stronger, nearing pre-NFP levels with TYH4 tapping 110-22 recently (10YY 4.1834% low). Curves flatter with short end lagging. Projected rate cuts for early 2024 mostly steady: December still flat at 5.333%, January 2024 cumulative -.7bp at 5.323%, March 2024 chance of rate cut at -48.4% vs. -44.5% late Monday w/ cumulative of -12.8bp at 5.202%, May 2024 -63.8% vs. -63.5% late Monday, cumulative -28.7bp at 5.042%. Fed terminal at 5.335% in Feb'24.

- SOFR Options: Reminder, Dec'24 SOFR options expire Friday

- Block, 10,000 SFRU4 96.50/98.00 call spds 5.5 over 2QU4 97.00/97.37 call spds

- 2,000 SFRM4 94.50/94.62/94.68/94.81 put condors ref 95.14

- 3,000 SFRM4 97.50/98.00 call spds ref 95.145

- 3,600 0QZ3 95.75 puts ref 95.825

- 4,000 SFRF4 94.81/94.93/95.06 call flys ref 94.815

- Treasury Options:

- over -6,000 TYH4 110.5 straddles from 2-60 to 2-54

- 10,000 wk5 TY 109 puts, 17 ref 110-21 (expire Dec 29)

- 5,700 TYF4 112 calls, 12-14

- 5,000 TYF4 109.5 puts, 16-18

- 2,000 wk3 TY 109/109.5/110 put flys, 1 ref 110-20

EGBs-GILTS CASH CLOSE: Gilts Outperform Ahead Of Fed/ECB/BoE

EGBs and Gilts strengthened Tuesday, ahead of multiple key central bank decisions in the coming two days.

- Core FI started the session on the front foot, with softer-than-expected UK wage data setting the stage for Gilt outperformance throughout the day. German/Eurozone ZEW surveys showed improved investor expectations, but the reading was shrugged off.

- The knee-jerk reaction from largely in-line US inflation data saw Bunds and Gilts touch session highs in early afternoon trade, but the move swiftly reversed as increasing attention was put on a robust "supercore" CPI reading ahead of Wednesday's Federal Reserve decision.

- Both the German and UK curves leaned bull steeper on the day.

- Periphery EGB spreads closed mostly tighter to Bunds, with Greece lagging.

- With little on the European docket Wednesday, all attention will be on US data and the Fed decision after the European close - ahead of the ECB (MNI preview here) and BoE (MNI preview here) decisions on Thursday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 2.709%, 5-Yr is down 2.5bps at 2.21%, 10-Yr is down 4.4bps at 2.226%, and 30-Yr is down 5.9bps at 2.401%.

- UK: The 2-Yr yield is down 8.5bps at 4.529%, 5-Yr is down 10.7bps at 4.04%, 10-Yr is down 11.1bps at 3.967%, and 30-Yr is down 7.4bps at 4.474%.

- Italian BTP spread down 1.6bps at 177.8bps / Spanish down 1.4bps at 101.5bps

EGB Options: Quiet In Rate/Bond Options Ahead Of Fed/ECB/BoE

Tuesday's Europe rates/bond options flow included:

- OEG4 118/116.75ps 1x2 with OEH4 117.5/116ps 1x2 bought the strip for 44 in 1k

- RXG4 131.00/128.50ps, bought for 19.5 in 4k.

- ERZ4 96.75/98.50 combo bought for 8.25 in 2.5k (buys put), (vs 97.34)

- ERU4 97.25/98.25 call spread sold at 19.25 in 10k (vs 97.07)

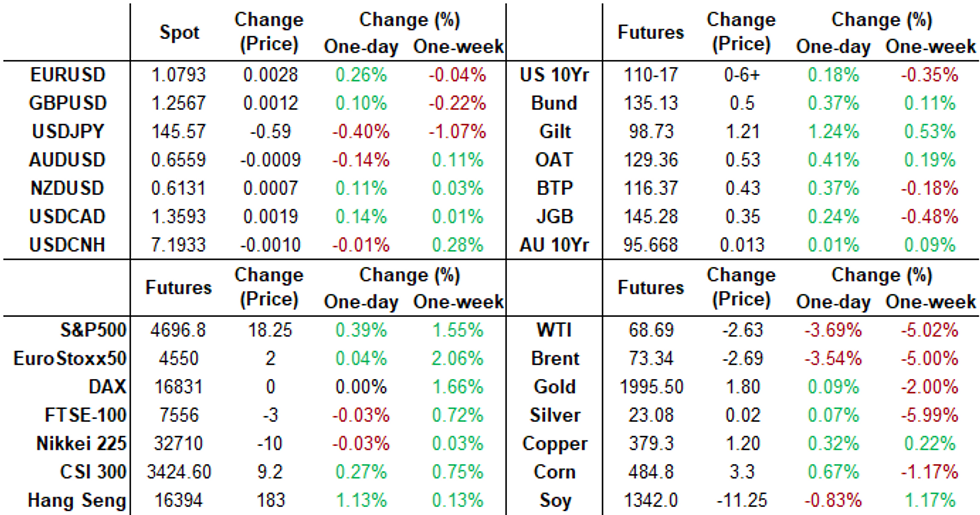

FOREX Greenback Consolidates Moderate Weakness Ahead of December FOMC

- Despite some volatile price action over the US inflation data, the USD index sits just 0.20% lower on the session as we approach the APAC crossover. Potential profit-taking evident as resistance at 104.26 failed to give way across the Friday/Monday sessions and as markets await tomorrows FOMC meeting.

- US headline data surprised very moderately to the upside and appears to have supported early greenback weakness across, however, a more benign unrounded core figure did initially prompt the USD to come under a brief bout of additional weakness. Price action saw USDJPY briefly print a low of 144.74 from an earlier 146.18 high, although the pair has since consolidated around 145.65.

- G10 currency adjustments remain small on the day, given the fact that the data is unlikely to alter the FOMC’s thinking before tomorrow’s decision and the release of its latest set of projections.

- Both the Euro and the Swiss Franc are among the best performers amid the softer dollar, with both the ECB and SNB meetings also this week.

- More broadly, however, EURUSD maintains a softer tone and is trading just above its recent lows. Price has recently pierced support at the 50-day EMA - at 1.0774 and a sustained break of this average would strengthen a bearish theme and open 1.0693, the Nov 14 low. On the upside, initial resistance is at 1.0820, the 20-day EMA.

- UK GDP and US PPI data will precede tomorrow’s Fed meeting/presser, where the FOMC will hold rates in December for a 3rd consecutive meeting, further cementing expectations that the hiking cycle is over.

FX Expiries for Dec13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0775-90(E1.9bln), $1.0840-50(E1.6bln)

- USD/JPY: Y145.00-15($1.6bln), Y146.00($1.2bln), Y147.00($969mln)

- USD/CAD: C$1.3690-00($558mln), C$1.3750($841mln)

Equities Roundup: Near Late Highs, Materials, IT Sectors Outperform

- Stocks gained traction in the second half, trading near late session highs as focus turns to tomorrow's PPI and the FOMC policy announcement. Currently, DJIA trades is up 178.96 points (0.49%) at 36583.68, S&P E-Mini future up 18 points (0.38%) at 4696.25, Nasdaq up 89.5 points (0.6%) at 14521.16.

- Leading gainers: Materials, Information Technology and Financial sectors outperform in late trade, industrial gasses and construction material makers led the former: Linde +4.20%, Martin Marietta Materials +1.83%, Vulcan Materials +0.96%. Semiconductor shares led IT as AI demand gains traction again: Broadcom +4.68%, AMD +2.14%, Nvidia +1.6%. Insurance companies continued to support Financials: Everest Grp +1.86%, AIG +1.59%, Aflac +1.35%.

- Laggers: Energy, Utilities and Communication Services sectors underperformed, oil and gas shares weighed on the former as crude prices marked new six month lows (WTI -2.65 at 68.67): Occidental Petroleum -2.91%, Marathon Oil -2.79%, Devon Energy -2.44%. Electricity providers weighed on Utilites: Constellation Energy -1.69%, Pinnacle West -1.61%, Southern Co -1.32%. Meanwhile, wireless services weighed on the communication services: AT&T -1.41%, Verizon -1.19%.

E-MINI S&P TECHS: (H4) Northbound

- RES 4: 4808.25 High Jan 4 2022

- RES 3: 4738.50 High Jul 27 and key resistance

- RES 2: 4700.00 Round number resistance

- RES 1: 4697.75 Intraday high

- PRICE: 4696.25 @ 15:30 ET Dec 12

- SUP 1: 4592.23 20-day EMA

- SUP 2: 4523.54 50-day EMA

- SUP 3: 4420.25.25 Low Nov 14

- SUP 4: 4354.25 Low Nov 10

A bullish theme in S&P e-minis remains intact and the contract has traded to a fresh high today. The break higher confirms once again a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting positive market sentiment. Sights are on the 4700.00 handle next. Initial support lies at 4592.23, the 20-day EMA.

COMMODITIES: Oil Slides Towards Late June Lows, Gold Still Tests 50-day EMA Support

- Crude prices are heading for their lowest levels since late June, amid signs of further bolstered US production, continued scepticism towards OPEC+ output cuts, and a continued weak economic outlook.

- Elsewhere, the EIA Short Term Energy Outlook has revised its estimate for global oil supply in 2024 to 102.19m b/d, down from 102.55m b/d in November’s report.

- A biofuel tanker was struck by a missile in the Red Sea Monday, launched from Houthi controlled territory in Yemen. The tanker was bound for Italy.

- Chevron has increased its crude production in Venezuela to 150kbpd, from 50kbpd prior to the US sanction relief in October.

- WTI is -3.7% at $68.65 off a low of $68.22, pushing through support at $68.80 (Dec 7 low) to open $67.28 (June 23 low).

- Brent is -3.6% at $73.31 off a low of $72.86, through $73.50 (Jul 6 low) to open $71.45 (Jun 23 low) after which lies key support at $69.86 (May 4 low).

- Gold is -0.1% at $1979.95, consolidating yesterday’s slide. It’s off an earlier low of $1977.46 that just about held above yesterday’s low of $1975.93, although some support is seen at the 50-day EMA of $1978.4.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/12/2023 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 13/12/2023 | 0700/0700 | ** | | UK | Index of Services |

| 13/12/2023 | 0700/0700 | *** | | UK | Index of Production |

| 13/12/2023 | 0700/0700 | ** | | UK | Trade Balance |

| 13/12/2023 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 13/12/2023 | 1000/1100 | ** |  | EU | Industrial Production |

| 13/12/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 13/12/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 13/12/2023 | 1330/0830 | * |  | CA | Household debt-to-income |

| 13/12/2023 | 1330/0830 | *** | | US | PPI |

| 13/12/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 13/12/2023 | 1900/1400 | *** | | US | FOMC Statement |

| 14/12/2023 | 2145/1045 | *** |  | NZ | GDP |

| 14/12/2023 | 2350/0850 | * |  | JP | Machinery orders |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.