Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- MNI EXCLUSIVE: US Wages Under Pressure As Fiscal Aid Dwindles

- MNI POLICY: NY Fed: Consumer Spending Seen Fastest Since 2019

- MNI INSIGHT: December Next Step On BOE's Negative Rate Path

- MCCONNELL SAYS SENATE TO VOTE ON PPP, TARGETED FUNDING WEEK OF OCT. 19, Bbg

- SAUDI ARAMCO ARE IN TALKS WITH BLACKROCK AS WELL AS OTHER INVESTORS, REGARDING A PIPELINE DEAL WORTH OVER $10 BLN, Rtrs

US

US: U.S. wages are likely to fall faster as government support for individuals and households under the CARES Act evaporates and a faster-than-expected jobs market recovery shows signs of slowing, labor market experts told MNI.

* An added USD600 a week in federal unemployment benefits and forgivable loans for small businesses under the Paycheck Protection Program likely supported wages through the summer despite significant downward pressure on labor demand caused by the Covid-19 pandemic, economists said. For more, see 10/13 main wire at 1335ET.

DATA: U.S. consumers in September predicted the fastest spending growth since May of last year while more people were at risk of missing a bill payment, the New York Federal Reserve's latest consumer survey published on Tuesday showed.

* Median household spending growth expectations quickened to 3.4% in September from 3.0% in August, the report showed. The average probability of missing a future minimum debt payment increased 1 percentage point to 10.7% in September, but still remained below its 2019 average of 11.5%. For more, see 10/13 main wire at 1100ET.

UK

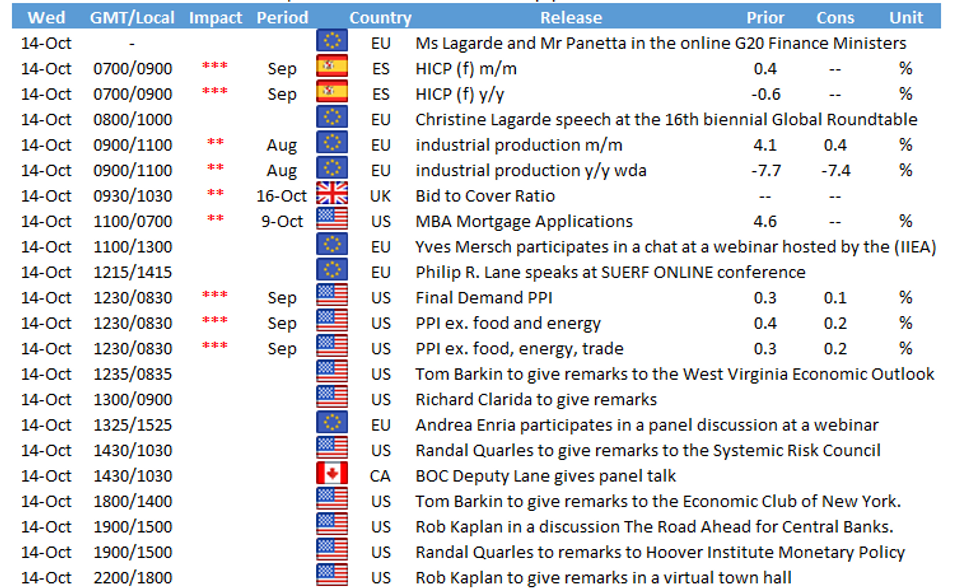

BOE: The Bank of England could provide results of its consultation into the effects of negative rates on the banking system in its Financial Stability Report due Dec. 10, setting the stage for further Monetary Policy Committee discussion of the matter the following week, MNI understands. For more, see 10/13 main wire at 1150ET.

OVERNIGHT DATA

US DATA: September CPI +0.2%; Core +0.2%

* U.S. CPI rose 0.2% in September following a 0.4% gain in August. Financial markets had expected an increase of 0.2%.

* Energy prices were up 0.8%, with September natural gas prices rising 4.2%. Gasoline prices increased 0.1% after a 2.0% gain in August.

* Food prices were unchanged in September, with a 0.6% gain in the cost of dining out weakened by a 0.4% decline in grocery prices.

* Excluding food and energy, CPI was up 0.2%, in line with market expectations. That was mainly driven by surging prices of used cars and trucks, which rose 6.7% in September, the largest monthly increase since 1969.

US REDBOOK: OCT STORE SALES +0.4% V SEP THROUGH OCT 10 WK

US REDBOOK: OCT STORE SALES +1.2% V YR AGO MO

US REDBOOK: STORE SALES +1.2% WK ENDED OCT 10 V YR AGO WK

Key Market Levels, Risk-Off Extends Ranges

Late session trading with concerted risk-on tone, Tsys near highs, albeit on light volume (TYZ<800K) while equities see-saw near modest lows after Mon's sharp rally.- DJIA down 112.76 points (-0.39%) at 28749.96

- S&P E-Mini Future down 25 points (-0.71%) at 3514.5

- Nasdaq down 1.3 points (0%) at 11907.39

- US 10-Yr yield is down 4.7 bps at 0.7272%

- US Dec 10Y are up 9.5/32 at 139-6.5

- EURUSD down 0.0075 (-0.63%) at 1.1737

- USDJPY up 0.18 (0.17%) at 105.52

- WTI Crude Oil (front-month) up $0.82 (2.08%) at $40.42

- Gold is down $31.19 (-1.62%) at $1892.62

US TSY SUMMARY: Strong Risk-Off

Stimulus, pharma and tech company related headlines remain key driver for risk-of bid in rates, weaker equities (US$/Yen bounce contributing factor (105.55H).

- Mkt on edge after House Majority Leader Hoyer on MSNBC said Speaker Pelosi and Tsy Sec Mnuchin "want to make a deal" but added Pres Trump is "erratic, impulsive on talks". Sen Majority Leader McConnell said wanted vote on $500B targeted relief package sometime next week. Latest counter offer rejected by House Speaker Pelosi and Democrats.

- Pharmaceutical co. Eli Lilly following J&J, halting antibody trial on potential safety concerns, equities falling to new session lows.

- Equities extended session lows on back of earlier Apple headline: "CHINESE PLATFORMS CANCELED APPLE LIVESTREAM, NO REASON GIVEN," Bbg, platforms: Bilibili, Iqiyi, Tencent and Weibo.

- The 2-Yr yield is down 1.4bps at 0.139%, 5-Yr is down 3.5bps at 0.3024%, 10-Yr is down 4.8bps at 0.7256%, and 30-Yr is down 6.2bps at 1.5094%.

US TSY FUTURES CLOSE: Near Highs

Broadly higher, near top end session range, yld curves flatter on moderate volumes, TYZ>920k), update:

- 3M10Y -3.887, 63.087 (L: 62.414 / H: 65.734)

- 2Y10Y -2.857, 58.625 (L: 58.26 / H: 61.45)

- 2Y30Y -3.846, 137.439 (L: 137.106 / H: 141.002)

- 5Y30Y -2.14, 121.137 (L: 120.937 / H: 123.081)

- Current futures levels:

- Dec 2Y up 0.87/32 at 110-14 (L: 110-13.12 / H: 110-14.12)

- Dec 5Y up 4.75/32 at 125-28 (L: 125-23.5 / H: 125-28.75)

- Dec 10Y up 9.5/32 at 139-6.5 (L: 138-28.5 / H: 139-08)

- Dec 30Y up 24/32 at 175-4 (L: 174-08 / H: 175-07)

- Dec Ultra 30Y up 1-22/32 at 219-17 (L: 217-15 / H: 219-22)

US TSYS/SUPPLY: Review Week's Tsy Auctions

| DATE | TIME | AMT | SECURITY | CUSIP/YIELD |

| 13-Oct | 1130ET | $54B | 13W-Bill | (9127963U1), 0.105% |

| 13-Oct | 1130ET | $51B | 26W-Bill | (9127964Y2), 0.11% |

| 13-Oct | 1300ET | $30B | 43D-Bill CMB | (9127963B3), 0.095% |

| 13-Oct | 1300ET | $30B | 119D-Bill CMB | (9127964C0), 0.110% |

| 14-Oct | 1130ET | $25B | 105D-Bill CMB | (912796B65) |

| 14-Oct | 1130ET | $30B | 154D-Bill CMB | (912796C98) |

| 15-Oct | 1130ET | $30B | 4W-Bill | (9127964S5) |

| 15-Oct | 1130ET | $30B | 8W-Bill | (9127965C9) |

US EURDLR FUTURES CLOSE: Bid Out The Strip

Steady in the short end to moderately bid out the strip. Lead quarterly holds steady since 3M LIBOR set' +0.00800 to 0.23688% (+0.01275/wk). Latest lvls:

- Dec 20 steady at 99.760

- Mar 21 steady at 99.790

- Jun 21 +0.010 at 99.805

- Sep 21 +0.015 at 99.805

- Red Pack (Dec 21-Sep 22) +0.010 to +0.020

- Green Pack (Dec 22-Sep 23) +0.025 to +0.035

- Blue Pack (Dec 23-Sep 24) +0.040 to +0.045

- Gold Pack (Dec 24-Sep 25) +0.045 to +0.050

USD LIBOR FIX

- O/N 0.08000 (-0.00175)

- 1W 0.09650 (-0.00038)

- 1M 0.14838 (0.00413)

- 2M 0.18088 (-0.00425)

- 3M 0.23688 (0.008)

- 6M 0.25450 (0.01162)

- 12M 0.34550 (-0.00213)

FED: NY Fed Operational Purchase:

- TSY 20Y-30Y, $1.733B accepted of $3.992B submission

- Next scheduled purchase:

- Wed 10/14 1010-1030ET: TIPS 7.5-30Y, appr $1.225B

- Wed 10/14 Next forward schedule release at 1500ET

PIPELINE: Toyota Motor Cr Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/13 $2.75B #Toyota Motor, $1.15B 2Y +25, $600M 2Y FRN SOFR+34, $1B 5Y +53; adds to $3B issued on May 20: $1.25B 2Y +100, $1B 3Y +115, $750M 5Y +125.

- 10/13 $1.4B Gaz Finance, inaugural US$ issuance, perp NC5.25, 4.6%a

- 10/13 $1B #Petrobras Global Finance 5.6% 2031 Tap, 4.4% yld

- 10/13 $600M #Athene Global Funding 3Y +103

- 10/12 No new issuance Monday

- Expected to issue Wednesday:

- 10/14 $1B EIB WNG 7Y +15a

- 10/14 $Benchmark Council of Europe 3Y +6a

- 10/14 $Benchmark CADES 10Y Social bond +30a

FOREX SUMMARY

A busy afternoon session for FX, as the USD led direction

- US CPI came out inline, and wasn't a driving factor.

- Stimulus related headlines remain key driver for assets: House Majority Leader Hoyer on MSNBC says Speaker Pelosi and Tsy Sec Mnuching" want to make a deal" says Pres Trump is "erratic, impulsive on talks"

- USD was bought across the board , testing high of the session versus the EUR, GBP, JPY, CHF, CAD, AUD, NOK and TRY,

- USDJPY printed a 105.63 high, still short of MNI resistance at 105.83 20-day EMA

- Cable dropped 20 pips initially, following EU Barnier noted that not enough progress has been made to enter tunnel negotiations..

- And came under renewed pressure following PM Boris spokesman, saying there's no fear in an Australian outcome.

- Cable fell to 2-day of low at 1.2922, breaking MNI tech support at 1.2939/31 20- day and 50-day EMA

- Looking ahead, Riksbank Inves, ECB de Cos and Fed Barkin are set to speak.

Equities just now extending session lows -- trader say this may be related to/catching up with recent Apple headline. - "CHINESE PLATFORMS CANCELED APPLE LIVESTREAM, NO REASON GIVEN" - Bloomberg

EGB: European govies have traded firmer through the day

Following a relatively quiet start, gilts have rallied in the afternoon session with the longer-end of the curve outperforming. Cash yields are now 2-5bp lower. BoE Governor Andrew Bailey has stated that persistent unemployment is a key measure of economic scarring brought about by the coronavirus crisis.

- Bunds similarly started to make gains early in the afternoon with the curve marginally bull flattening. BTPs have outperformed bunds with longer end yields edging down 4bp.

- Supply came from the UK (Gilts, GBP4.25bn), Italy (BTPs, EUR7.5bn), Spain (Letras, EUR0.935bn), Netherlands (DSL, EUR2bn), Belgium (TCs, EUR1.845bn), Finland (bills, EUR1.981bn) and the ESM (bills, EUR1.5bn).

- The UK government is coming under fresh pressure as it has emerged that it did not act on SAGE's advice for a two-week national circuit breaker to curb the spread of the coronavirus.

- Looking ahead, tomorrow sees the release of Spanish final CPI data for September and Eurozone industrial production data for August.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.