Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US

FED: Federal Reserve Chair Jay Powell will continue in his role as chair of the Bank of International Settlements' Global Economy Meeting as well as the Basel-based group's Economic Consultative Committee.

- In a statement Tuesday, the BIS said Powell's reappointment term would run until January 31 2026. He was first appointed on 1 February 2020. Both the GEM and the ECC are among the principal meetings held at the BIS every two months.

- The GEM is comprised of 30 BIS member central bank Governors in major advanced and emerging market economies that account for about four fifths of global GDP. The Governors of another 22 central banks attend the GEM as observers.

- High demand for other services likely added to that pressure, however, some easing in core goods prices could have been masked by the headline, as industry gauges of used car prices have fallen along with the fading of supply chain issues in that sector.

- Core prices could also decelerate ahead if supply chain improvements and the impact of past interest rate hikes on demand start to materialize.

- With inflation still set to remain elevated into 2023, the Fed will likely hike rates by another 100bps in order to contain inflation expectations and cool the labor market.

- Whilst inline with consensus for core inflation, they see headline CPI at 0.7% M/M (cons 0.6%) which limits the decline in the year-ago rate to -0.2pts at 8.0% Y/Y, as relief from higher prices at the pump ended in October post-OPEC+ supply curtailments and was combined with broad price pressures in other categories.

UK

BOE: The Bank of England is heading for a cycle peak in Bank Rate of no more than around 4%, followed by a fairly rapid switch to easing to avoid a slide in projected inflation below target, projections from its November Monetary Policy report and comments by policymakers suggest.

- The BOE’s “best view” of the peak is closer to the current 3% level of Bank Rate than the 5.25%, based on previous market assumptions of the highest point of the cycle, which the BOE used in its market-based projections, Governor Andrew Bailey told a news conference after its Nov 4 decision. While the Bank and its chief economist Huw Pill have signaled more rate rises are to come, this implies a peak of no more than roughly 4.1% at most, still well below the 4.7% priced in by investors today.

- The BOE’s Monetary Policy Report projections imply that inflation will substantially undershooting the 2% target within the forecast horizon if rates either follow the market path or remain at a constant 3%, suggesting that cuts may have to follow the hiking without much delay. For more see MNI Policy main wire at 1040ET.

- Giving evidence to the Lords Economic Affairs Committee Pill said that inflation was "the more important driver of wage growth," with wage growth of over 6% in private sector earnings incompatible with the Monetary Policy Committee's 2% inflation target.

- Pill said that he expected high vacancy rates, distorted in part by the Covid shock, would decline going forward and that unemployment rates would rise, with the weakness in demand reflected in a reduction in working hours and unemployment hitting 6%. Nevertheless, he argued that further rate hikes were needed. Asked by former BOE Governor Meryn King if Bank Rate was insufficiently high, Pill said that "I have sympathy with you that 3% is not enough."

US TSYS: Rates, Stocks, Metals Stronger, Bitcoin Rout

Treasury futures finished broadly higher Tuesday, near late session highs, yield curves bull-flattening (2s10s -1.701 at -53.145 vs. -56.297 low) after holding steeper earlier in the first half.- Skittish first-half trade: Tsys sold off ahead the NY open apparently reacting to a misinterpreted German debt headline (more than doubling debt issuance next year).

- Tsys followed Bunds off lows as it became clear Germany is not doubling net debt, just a comparison to earlier projections, as opposed to an actual figure.

- Tsys see-sawed higher from midmorning on - no obvious headline trigger for move, volumes rather modest (TYZ2<575k) while some trading desks noted stops triggered on the way up. Dec 10Y futures at 110-06 still well off first resistance of 110-25 20D DMA.

- Cross asset: Gold surged over 40.0 to 1716.75 high, while equities gaining upside support - lead by metals and mining shares. Sharp rout in Bitcoin (-15%) coincided with stocks reversing gains in late trade before staging a late rebound.

- Treasury futures helding gains after $40B 3Y note auction (91282CFW6) stops through: 4.605% high yield vs. 4.615% WI; 2.57x bid-to-cover steady to last month.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 404.09 points (1.23%) at 33235.55

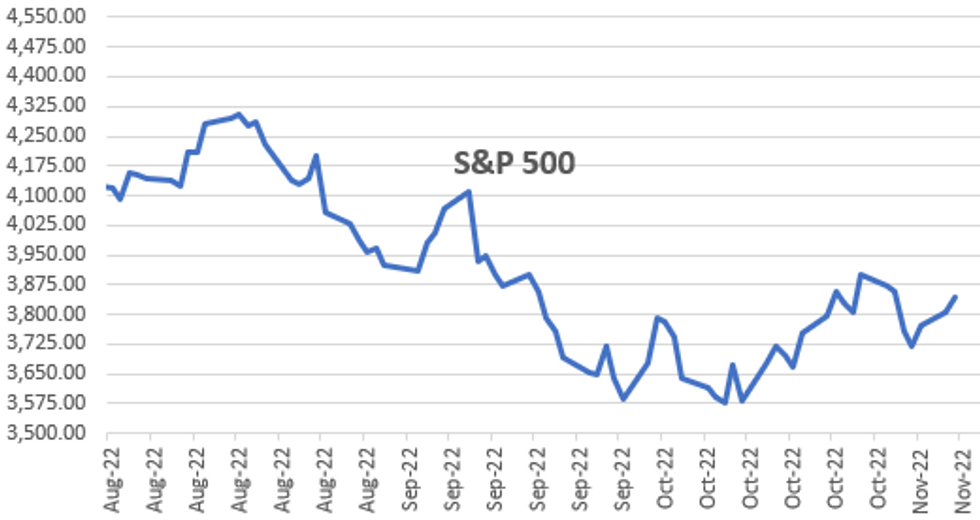

- S&P E-Mini Future up 28.5 points (0.75%) at 3844.75

- Nasdaq up 63 points (0.6%) at 10629.13

- US 10-Yr yield is down 8.8 bps at 4.1255%

- US Dec 10Y are up 20.5/32 at 110-9

- EURUSD up 0.0055 (0.55%) at 1.0075

- USDJPY down 1.1 (-0.75%) at 145.53

- WTI Crude Oil (front-month) down $2.64 (-2.88%) at $89.15

- Gold is up $36.6 (2.18%) at $1712.31

- EuroStoxx 50 up 30.48 points (0.82%) at 3739.28

- FTSE 100 up 6.15 points (0.08%) at 7306.14

- German DAX up 155.23 points (1.15%) at 13688.75

- French CAC 40 up 24.89 points (0.39%) at 6441.5

US TSY FUTURES CLOSE

- 3M10Y -19.22, -6.044 (L: -9.052 / H: 9.934)

- 2Y10Y -2.96, -54.404 (L: -56.297 / H: -49.122)

- 2Y30Y -0.202, -41.099 (L: -45.36 / H: -38.086)

- 5Y30Y +2.311, -4.909 (L: -9.054 / H: -4.344)

- Current futures levels:

- Dec 2Y up 4.125/32 at 101-26.875 (L: 101-21.75 / H: 101-27.625)

- Dec 5Y up 11.75/32 at 106-8.75 (L: 105-25.5 / H: 106-09.75)

- Dec 10Y up 20/32 at 110-08.5 (L: 109-14 / H: 110-10.5)

- Dec 30Y up 1-12/32 at 119-29 (L: 118-03 / H: 120-01)

- Dec Ultra 30Y up 1-07/32 at 126-14 (L: 124-16 / H: 126-30)

US 10YR FUTURE TECH: (Z2) Support Remains Exposed

- RES 4: 113-27+ High Sep 21

- RES 3: 113-30 High Oct 4 and a key resistance

- RES 2: 112-18 50-day EMA

- RES 1: 110-25/111-31 20-day EMA / High Oct 27

- PRICE: 109-24+ @ 11:31 GMT Nov 8

- SUP 1: 109-10+ Low Nov 04

- SUP 2: 108-26+ Low Oct 21 and the bear trigger

- SUP 3: 108-06+ Low Oct 2007 (cont)

- SUP 4: 107.09 3.0% 10-dma envelope

Treasuries maintain a softer tone and continue to trade below 111-31, the Oct 27 high and a key short-term resistance. Clearance of this hurdle is required to signal scope for a stronger short-term rally. This would open the 50-day EMA at 112-18. The primary trend direction is down and recent weakness has exposed the key support and bear trigger at 108-26+, the Oct 21 low. A breach of this level would confirm a resumption of the trend.

US EURODOLLAR FUTURES CLOSE

- Dec 22 +0.010 at 94.890

- Mar 23 +0.025 at 94.655

- Jun 23 +0.040 at 94.630

- Sep 23 +0.070 at 94.80

- Red Pack (Dec 23-Sep 24) +0.080 to +0.085

- Green Pack (Dec 24-Sep 25) +0.080 to +0.085

- Blue Pack (Dec 25-Sep 26) +0.090 to +0.095

- Gold Pack (Dec 26-Sep 27) +0.105 to +0.110

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00243 to 3.81557% (-0.00072/wk)

- 1M +0.00357 to 3.85571% (+0.00057/wk)

- 3M +0.03471 to 4.59200% (+0.04171/wk) * / **

- 6M +0.11157 to 5.13443% (+0.12314/wk)

- 12M +0.02815 to 5.64029% (-0.02614/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.59200% on 11/8/22

- Daily Effective Fed Funds Rate: 3.83% volume: $99B

- Daily Overnight Bank Funding Rate: 3.82% volume: $291B

- Secured Overnight Financing Rate (SOFR): 3.78%, $981B

- Broad General Collateral Rate (BGCR): 3.76%, $405B

- Tri-Party General Collateral Rate (TGCR): 3.75%, $393B

- (rate, volume levels reflect prior session)

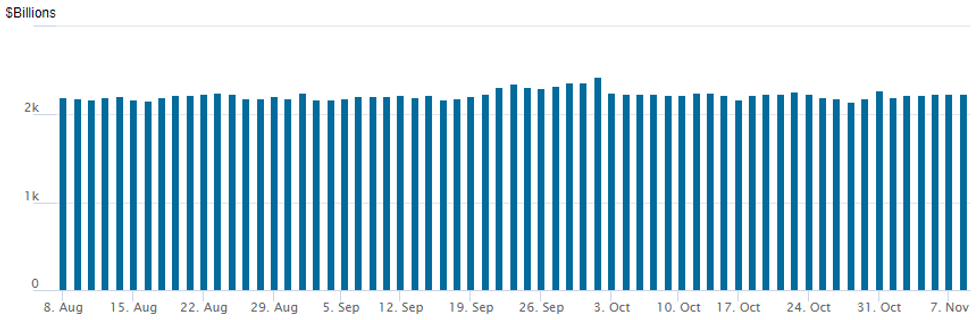

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,232.555B w/ 101 counterparties vs. $2,241.317B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

PIPELINE: Republic of Poland 5Y, 10Y on Tap

- Date $MM Issuer (Priced *, Launch #)

- 11/08 $3B #Rep of Poland $1.5B 5Y +130, $1.5B 10Y +175

- 11/08 $2B #Standard Chartered $3NC2 +310, $1B 6NC5 +345B

- 11/08 $1.35B #Zoetis $600M 3Y +85, $750M 10Y +150

- 11/08 $Benchmark GE Healthcare investor calls

- $23.75B Priced Monday, Oracle's $7B kickstarted November issuance:

- 11/07 $7B *Oracle $1B 3Y +120, $1.25B 7Y +185, $2.25B 10Y +205, $2.5B 30Y +255

- 11/07 $2B *Bank of America 6NC5 +182

- 11/07 $2B *Dish Network 5MC2.5 12.25%

- 11/07 $1.9B *Qualcomm $700M 10Y +120, $1.2B 30Y +170

- 11/07 $1.5B *Turkey 5Y 10%

- 11/07 $1.35B *Toyota Motor Cr $650M 3Y +80, $700M 5Y +110

- 11/07 $1.25B *Humana $500M 5Y +143, $750M 10Y +173

- 11/07 $1.15B EBay $425B 3Y +130, $300M 5Y +160, $425M 10Y +210

- 11/07 $1B *Nutrien $500M 2Y +120, $500M 3Y +135

- 11/07 $1B *Lloyds 11NC10 +375

- Under $1B: $750M Ally Financial 5Y +295; $750M Boston Properties 5Y +237.5; $600M *Southern California Gas 30Y +205; $500M *Ecolab 5Y +100; $550M *Edison Int 7Y +280; $500M *Duke Energy 30Y +167;

EGBs-GILTS CASH CLOSE: Squaring Higher Pre-US Elections

After starting the session on the back foot, an afternoon rally left Gilts and Bunds stronger by Tuesday's close.

- Both the UK and German curves flattened, with long-end yields falling sharply in the afternoon. While there was no particular catalyst, some contacts suggested that desks were squaring positions ahead of US elections later.

- A BBG report that the UK and EU were close to a "breakthrough" on N Ireland helped boost risk appetite, with GBP jumping and Bund and Gilt futures extending session highs.

- BoE's Pill commented on potential de-anchoring of inflation expectations, though hike pricing was largely unchanged on the day.

- Periphery spreads tightened in a risk-on session, with equities rallying and the US dollar weakening - with all attention on overnight US election results.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 11.5bps at 2.324% (reflecting new Schatz becoming benchmark), 5-Yr is down 3.7bps at 2.199%, 10-Yr is down 6.2bps at 2.281%, and 30-Yr is down 8.2bps at 2.185%.

- UK: The 2-Yr yield is up 2.4bps at 3.254%, 5-Yr is down 3.6bps at 3.504%, 10-Yr is down 8.6bps at 3.552%, and 30-Yr is down 11.5bps at 3.738%.

- Italian BTP spread down 3.4bps at 211.2bps / Spanish down 1bps at 103.4bps

FOREX: Lower Yields Ignite An Extension Of USD Weakness

- A developing theme in the aftermath of the payrolls report has been a souring of greenback optimism, which extended once again on Tuesday. The Japanese Yen outperforms with USDJPY sliding back below 146 and EURUSD extending gains above parity.

- A slightly strange session for risk as an initial rally across equity markets was met with a significant rout across the cryptocurrency market, potentially bolstering the sentiment for gold, which saw 2.2% gains throughout the session.

- Currency markets appeared to take this volatility in its stride and the lower yields weighed on the greenback throughout US trade.

- EURUSD had consolidated much of the European session around parity, however, once breaking yesterday’s highs around 1.0030, the single currency appreciated sharply to the next target of 1.0094, the high on Oct 27 and a technical bull trigger. Despite a brief pullback, the pair maintains a supportive tone ahead of the APAC crossover.

- Similarly in cable, despite pulling back to 1.1430, the broad USD weakness saw the pair rally aggressively before topping out at 1.1600.

- The Japanese Yen is leading G10 gains on Tuesday, as the lower yields work against the favourite trade of 2022. Furthermore, interventions to strengthen the yen continue to linger for short-sellers, especially as we approach the important US CPI data on Thursday.

- Chinese CPI/PPI data is due overnight before another light day for European/US data on Wednesday.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/11/2022 | 0130/0930 | *** |  | CN | CPI |

| 09/11/2022 | 0130/0930 | *** | | CN | Producer Price Index |

| 09/11/2022 | 0700/0800 | ** |  | SE | Private Sector Production |

| 09/11/2022 | 0800/0300 |  | US | New York Fed's John Williams | |

| 09/11/2022 | 1000/1100 |  | EU | ECB Elderson Panels EMEA Event at COP27 | |

| 09/11/2022 | 1200/0700 | ** | | US | MBA Weekly Applications Index |

| 09/11/2022 | 1300/1300 |  | UK | BOE Haskel Speech at Digital Futures at Work | |

| 09/11/2022 | 1500/1000 | ** | | US | Wholesale Trade |

| 09/11/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 09/11/2022 | 1600/1100 | | US | Richmond Fed's Tom Barkin | |

| 09/11/2022 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 09/11/2022 | 1800/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.