Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: Community Bankers Say U.S. Already In Recession

- MNI US: Yellen: A Default Would Cause An Economic And Financial Catastrophe

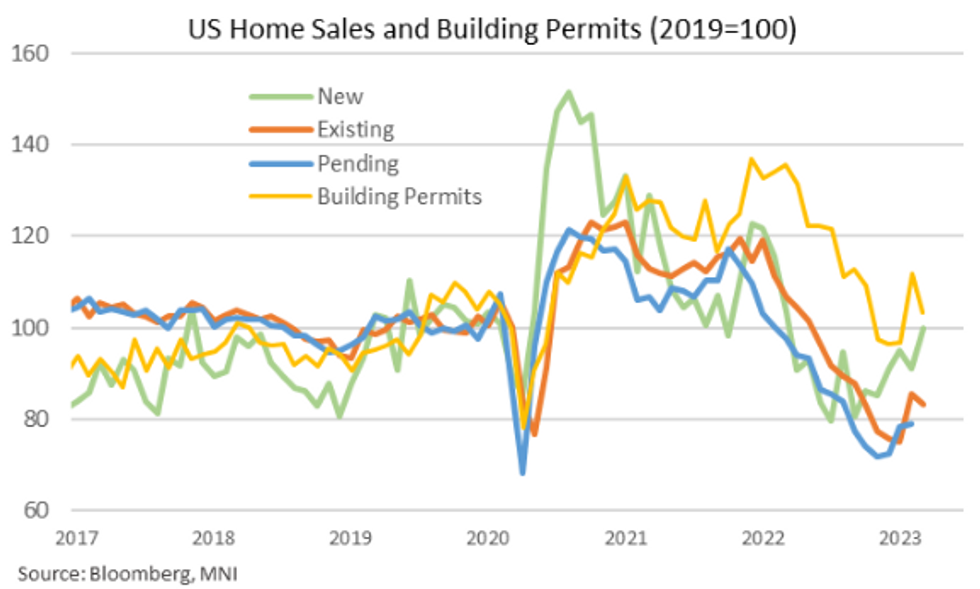

- US DATA: New Home Sales Surprisingly Jump With Regional Divergence

US

US: Community banker sentiment in the U.S. cratered further last month after bank runs, deposit complications and the subsequent closure of Silicon Valley Bank and other lenders, according to newly released survey data from the Conference of State Bank Supervisors, a nationwide organization of banking regulators.

- Driving community banker sentiment lower are concerns that government regulation could become more burdensome, through either new legislation designed to prevent similar liquidity problems in the future or more forceful supervisory actions as banks continue to adjust to the significantly higher interest rate environment, said Thomas Siems, chief economist at the group.

- The liquidity struggles influenced by the Fed’s rapid rate increases since March and the Fed’s apparent policy dilemma of fighting inflation on the one hand, and maintaining financial stability on the other hand, have heightened community banker worries of slower economic growth, higher inflation, and larger federal deficits, he said. For more see MNI Policy main wire at 1107ET.

US: Treasury Secretary Janet Yellen will tell the Sacramento Metropolitan Chamber of Commerce today that a federal default would cause an economic "catastrophe." Yellen will say: "We have enacted our generation’s most ambitious investment in infrastructure; led a major expansion of American advanced manufacturing; and passed the boldest climate action in our nation’s history."

- Yellen: "The Inflation Reduction Act presents a generational economic opportunity... and extend our country’s economic leadership in key clean energy..." She will warn that the economic recovery is under threat: "In my assessment [...] a default on our debt would produce an economic and financial catastrophe."

- "Household payments on mortgages, auto loans, and credit cards would rise. And American businesses would see credit markets deteriorate... it is unlikely that the federal government would be able to issue [Social Security] payments to millions of Americans... In the longer term, a default would raise the cost of borrowing into perpetuity. Future investments would become substantially more costly." "This economic catastrophe is preventable... Congress must vote to raise or suspend the debt limit. It should do so without conditions. And it should not wait until the last minute."

US TSYS: Rates Near Mid-Apr/Pre-Retail Sales Highs, 50Bp Dec Rate Cut In Play

- Front month Treasury futures extended session highs in late trade, partially driven by sell-off in stocks, SPX Eminis through 20-day EMA support of 4128.95 to 4097.50 low, just shy of 50-day EMA support at 4086.73.

- Underperforming sectors: Energy, Materials and Industrials continue to lead the sell-off in SPX, Financials near the middle of the pack while shares of First Republic Bank (FRC) falling 50% in late trade.

- Treasury curves bull steepening (2s10s +5.964 at -54.276 as 2s surged 13.5 to 103-15 following today's 2Y auction: 3.969% high yield vs. 3.965% WI; 2.68x bid-to-cover. Implied rate cuts into year end surged back over 50bp for Dec'23, Jan'24 -75bp cumulative.

- The rally in 10s undermines the recent bearish theme with price trading above both the 20- and 50-day EMAs. A continuation higher would signal scope for a climb towards 116-08, the Apr 12 high and expose the key resistance at 117-01+, the Mar 24 high.

- Wednesday Data Calendar, focus on Wholesale/Retail Inv, Durables and Capital Goods. Next legs of the week's Treasury coupon supply with $24B 2Y FRN (91282CGY1, $36B 17W bill auction at 1130ET; $43B 5Y Note auction (91282CHA2) and $45B 17D bill CMB auction at 1300ET.

OVERNIGHT DATA

- US REDBOOK: APR STORE SALES +1.5% V YR AGO MO

- US REDBOOK: STORE SALES +1.8% WK ENDED APR 22 V YR AGO WK

- US APR PHILADELPHIA FED NON-MFG INDEX -22.8

- US FEB. FHFA HOME PRICE INDEX RISES 0.5% M/M; EST. -0.1%

- US FEB. S&P CORELOGIC CS 20-CITY ADJUSTED INDEX UP 0.1% M/M (est -0.35%)

- US APRIL RICHMOND FED FACTORY INDEX -10; EST. -8, Bbg

- US APRIL CONSUMER CONFIDENCE 101.3; EST. 104.0, Bbg

- US MARCH NEW-HOME SALES AT 683,000 ANN. RATE; EST. 632,000. New home sales were far stronger than expected in March, jumping +9.6% M/M (cons -1.3).

- It follows a notably downward revised -3.9% in Feb (initial +1.1%) but that in turn followed an upward revised +4.2% in Jan (initial +1.8%), the broad upshot of which has left new home sales with a clearer upward trend in recent months off lows from Jun-Sep’22.

- The latest increase wasn't broad-based though, led by a 171% spike in the small north-east category with west sales also +30% on the month, whilst sales in the largest southern region fell -5.5%.

- The increase in new home sales has led the more recent recovery in both existing home sales and building permits, with existing home sales still almost 20% below pre-pandemic levels vs new home sales which have now closed the gap.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 291.45 points (-0.86%) at 33581.56

- S&P E-Mini Future down 58 points (-1.39%) at 4100.75

- Nasdaq down 204.8 points (-1.7%) at 11831.88

- US 10-Yr yield is down 9.8 bps at 3.3921%

- US Jun 10-Yr futures are up 30/32 at 115-26

- EURUSD down 0.0071 (-0.64%) at 1.0975

- USDJPY down 0.66 (-0.49%) at 133.58

- WTI Crude Oil (front-month) down $1.56 (-1.98%) at $77.19

- Gold is up $9.02 (0.45%) at $1998.16

- EuroStoxx 50 down 23.95 points (-0.54%) at 4377.85

- FTSE 100 down 21.07 points (-0.27%) at 7891.13

- German DAX up 8.18 points (0.05%) at 15872.13

- French CAC 40 down 42.25 points (-0.56%) at 7531.61

US TREASURY FUTURES CLOSE

- 3M10Y -12.3, -166.759 (L: -171.419 / H: -158.612)

- 2Y10Y +5.278, -54.962 (L: -63.49 / H: -52.454)

- 2Y30Y +9.055, -29.183 (L: -40.707 / H: -27.092)

- 5Y30Y +7.419, 21.11 (L: 13.865 / H: 21.539)

- Current futures levels:

- Jun 2-Yr futures up 13/32 at 103-14.5 (L: 103-04.25 / H: 103-16.625)

- Jun 5-Yr futures up 25/32 at 110-8.5 (L: 109-20.25 / H: 110-11.5)

- Jun 10-Yr futures up 30.5/32 at 115-26.5 (L: 115-01 / H: 115-30)

- Jun 30-Yr futures up 1-20/32 at 132-12 (L: 130-30 / H: 132-20)

- Jun Ultra futures up 1-29/32 at 142-2 (L: 140-15 / H: 142-15)

US 10YR FUTURE TECHS: (M3) Bounce Extends

- RES 4: 117-01+ High Mar 24 and bull trigger

- RES 3: 116-30 High Apr 5 / 6

- RES 2: 116-08 High Apr 12

- RES 1: 115-30 High Apr 25

- PRICE: 115-25 @ 1515ET Apr 25

- SUP 1: 114-28/15+ The 20- and 50-day EMA values

- SUP 2: 113-30+ Low Apr 19 and key short-term support

- SUP 3: 113-23 50.0% retracement of the Mar 3 - 24 bull run

- SUP 4: 113-08+ Low Mar 15

Treasury futures have found support and are trading higher today. The recovery undermines the recent bearish theme with price trading above both the 20- and 50-day EMAs. A continuation higher would signal scope for a climb towards 116-08, the Apr 12 high and expose the key resistance at 117-01+, the Mar 24 high. Key support has been defined at 113-30+, the Apr 19 low. A break would reinstate the recent bearish theme.

SOFR FUTURES CLOSE

- Jun 23 +0.110 at 95.015

- Sep 23 +0.190 at 95.335

- Dec 23 +0.240 at 95.765

- Mar 24 +0.270 at 96.270

- Red Pack (Jun 24-Mar 25) +0.240 to +0.295

- Green Pack (Jun 25-Mar 26) +0.155 to +0.215

- Blue Pack (Jun 26-Mar 27) +0.105 to +0.140

- Gold Pack (Jun 27-Mar 28) +0.080 to +0.10

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.01904 to 4.99648 (+.09650 total last wk)

- 3M +0.01074 to 5.07877 (+.09561 total last wk)

- 6M +0.00233 to 5.09070 (+.14765 total last wk)

- 12M -0.01428 to 4.86300 (+.18392 total last wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00700 to 4.80071%

- 1M +0.00157 to 5.01771%

- 3M +0.02343 to 5.29157% */**

- 6M -0.02814 to 5.40586%

- 12M -0.05471 to 5.37300%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.26500% on 4/17/23

- Daily Effective Fed Funds Rate: 4.83% volume: $110B

- Daily Overnight Bank Funding Rate: 4.81% volume: $275B

- Secured Overnight Financing Rate (SOFR): 4.80%, $1.298T

- Broad General Collateral Rate (BGCR): 4.77%, $533B

- Tri-Party General Collateral Rate (TGCR): 4.77%, $521B

- (rate, volume levels reflect prior session)

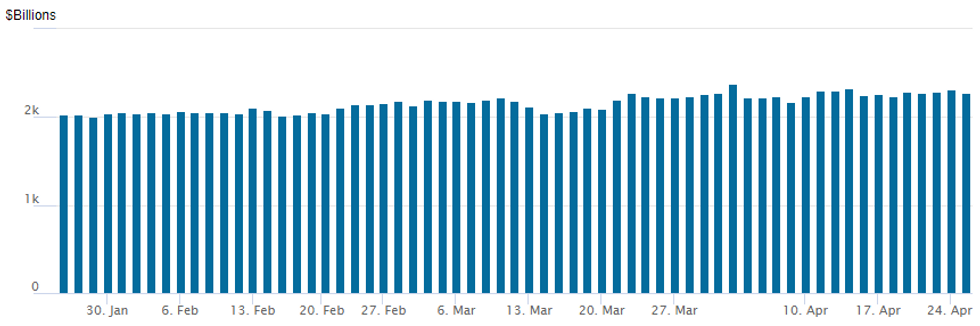

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,275.402B w/ 100 counterparties, compares to prior $2,038.538B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

EGBs-GILTS CASH CLOSE: Bunds Outperform As Bank Woes Resurface

Bunds outperformed Gilts amid a strong risk-off core FI rally Tuesday, with banking sector concerns returning to market consciousness.

- Cyclical stocks led equities lower, with financials the biggest drag on European indices following poor results by beleaguered US bank First Republic. The German curve bull steepened while the UK's bull flattened.

- Weak Spanish PPI set a bullish tone for bonds, but Bunds' outperformance was helped by a sharp 10bp pullback in ECB peak rate expectations, partly explained as a retracement of a bearish move on hawkish commentary by ECB's Schnabel late in Monday's session.

- BoE pricing retraced slightly less (-5bp), though a dovish move on comments by Chief Econ Pill seemed unwarranted as they were stale (recorded Apr 18, prior to CPI data).

- Despite equity weakness, EGBs held in fairly well, with spreads widening only modestly (Greece worst off, with 10Y GGBs 4.5bp wider to Bunds).

- Wednesday hosts another 2nd tier data slate, but we get the Swedish Riksbank decision (MNI preview here) as well as multiple ECB speakers including Vujcic, Guindos and Herodotou.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 13.2bps at 2.845%, 5-Yr is down 14.5bps at 2.415%, 10-Yr is down 12.4bps at 2.384%, and 30-Yr is down 10.8bps at 2.451%.

- UK: The 2-Yr yield is down 7.1bps at 3.733%, 5-Yr is down 9.3bps at 3.561%, 10-Yr is down 8.6bps at 3.695%, and 30-Yr is down 7.7bps at 4.043%.

- Italian BTP spread up 2bps at 189.2bps / Greek up 4.5bps at 183.4bps

FOREX: Poorer Risk Sentiment Prompts Safe Haven Demand, AUDJPY Slides 1.7%

- Worsening risk sentiment across global markets on Tuesday prompted a flight to quality. Historical safe havens are leading the charge with the USD index rallying half a percent and the Japanese Yen also benefitting.

- The session saw significant pressure on First Republic Bank with shares down as much as 45% at one point which filtered through to major indices. Furthermore, a strong rally for front end treasury futures, increasing bets for FED rate cuts this year, provided an additional JPY tailwind which resulted in AUDJPY registering declines of 1.7% as we approach the APAC crossover.

- With risk-tied AUD faring only behind NOK as the worst performers in G10, it is worth noting that AUDJPY has unwound the majority of the April bounce, significantly narrowing the gap with the month’s lows around 87.60. The move comes ahead of key CPI data due overnight for both March and the first quarter.

- Additionally, for EURJPY, after breaching the 2022 highs on Monday and reaching the highest level since late 2014 overnight at 148.62, the pair registered a 230 pip reversal with EURUSD sinking back below 1.10 heaping on the pressure. Overall, technical conditions remain bullish for the pair and today’s price action may be allowing an overbought condition to unwind. Initial firm support lies at 145.84, the 20-day EMA.

- USD/CNH briefly matched the 200-dma to the upside at 6.9507 – a significant resistance point for the pair. A break above here would be the first since February and open scope for further gains toward mid-March highs of 6.9971. Worsening trade tensions with the US remain a key driver - particularly following weekend reports that the US requested South Korean firms do not backfill chip orders to China should US-listed firms be barred access to China.

- As mentioned, Australian CPI highlights Wednesday’s docket. In the US, March durable goods figures will precede Thursday’s advanced Q1 GDP reading.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/04/2023 | 2301/0001 | * |  | UK | XpertHR pay deals for whole economy |

| 26/04/2023 | 0130/1130 | *** |  | AU | CPI inflation |

| 26/04/2023 | 0130/1130 | *** | | AU | CPI Inflation Monthly |

| 26/04/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 26/04/2023 | 0600/1400 | ** |  | CN | MNI China Liquidity Suvey |

| 26/04/2023 | 0600/0800 | ** |  | SE | Unemployment |

| 26/04/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/04/2023 | 0730/0930 | ** | | SE | Riksbank Interest Rate |

| 26/04/2023 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 26/04/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 26/04/2023 | 1200/1400 |  | EU | ECB de Guindos Panels Delphi Economic Forum | |

| 26/04/2023 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 26/04/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/04/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 26/04/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 26/04/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 26/04/2023 | 1730/1330 |  | CA | BOC minutes from last rate meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.