Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Copom Preview

Executive Summary

- The Copom are widely expected to hike the Selic rate by 100bps to 12.75% at their May meeting.

- This action would be in line with prior BCB communication signalling a hike of the same magnitude made at the previous meeting in March.

- Despite hinting that the tightening cycle may come to an end in May, continued inflationary pressures have led the majority of analysts to expect further policy tightening, placing increased significance on the BCB’s guidance within the statement on Wednesday.

Click to view the full preview: MNI Brazil Central Bank Preview - May 2022.pdf

BCB Rhetoric Keeps Future Guidance In Focus

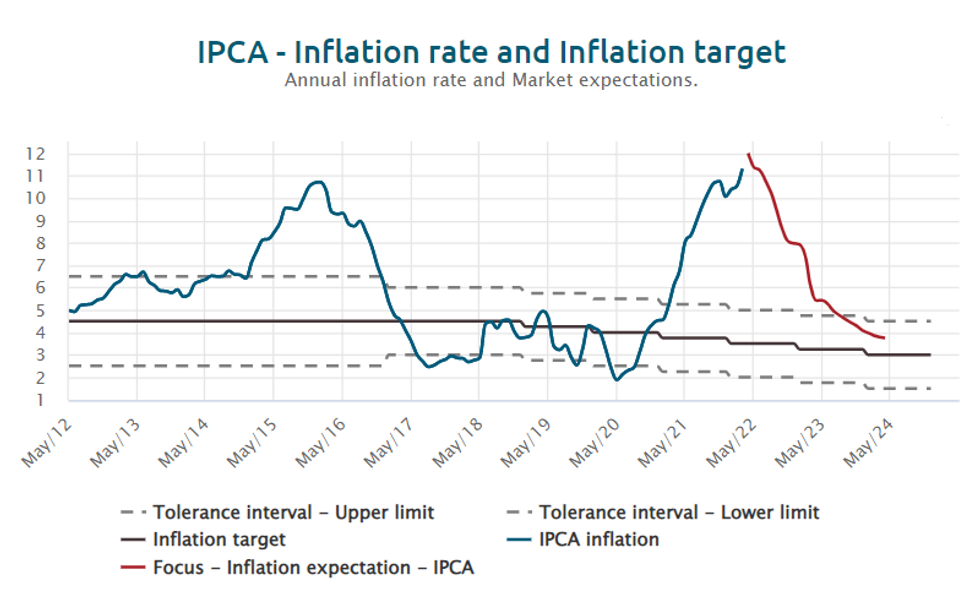

While the decision at this week’s meeting seems almost a foregone conclusion, market participants will be scrutinising the statement very closely looking for clues surrounding the June decision. The increased significance stems from inter-meeting comments from BCB Governor, Roberto Campos Neto. Speaking during a virtual event on March 25, the central bank chief said that hikes to the Selic rate would most likely end at 12.75% in May. However, Campos Neto did provide the caveat that if the international scenario worsened and there was another shock that affected expectations, the board could make an additional move in June.

This now looks like the most likely scenario for multiple reasons. First of all, his initial comments were made before the March inflation print where the headline figure rose to 11.3% Y/y. Following this release, Campos Neto said the increases in retail prices of fuel, clothing and food were big surprises, and those trends are now being reviewed by policy makers. Given a further worsening in both mid-month IPCA data and expectations within the central bank’s survey of economists, it appears the Copom may have to adjust their original rate path plan.

Source: Brazil Central Bank

Source: Brazil Central Bank

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.