Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

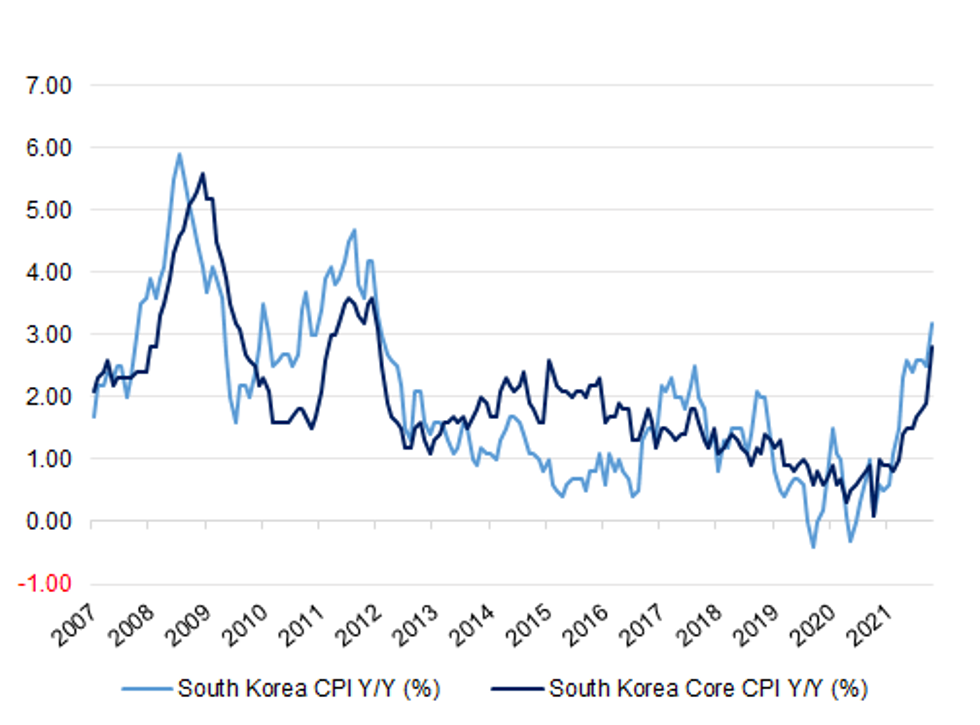

- A larger than expected uptick in inflation (and pipeline pressures) cemented broader expectations for a 25bp rate hike at this meeting, with almost all of the sell side looking for such a move. This moves focus to the vote split, with known dove, Joo Sangyong, providing the most obvious potential source of dissent (voted against the August hike).

- Governor Lee pointed to the likelihood of a November hike back in October, with the evolution of the economic situation since then seemingly greenlighting such a move.

- Despite some clear risks, the recent tweaks to BoK guidance and focus on financial imbalances, coupled with the government's focus on living with COVID, should facilitate at least one further rate hike in H122.

- Further out, elevated levels of debt and tighter macroprudential policy may ultimately cap the terminal rate observed in the current hiking cycle.

- Click to view full preview: BoK Preview - November 2021.pdf

Fig. 1: South Korea CPI & Core CPI (Y/Y

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok