Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

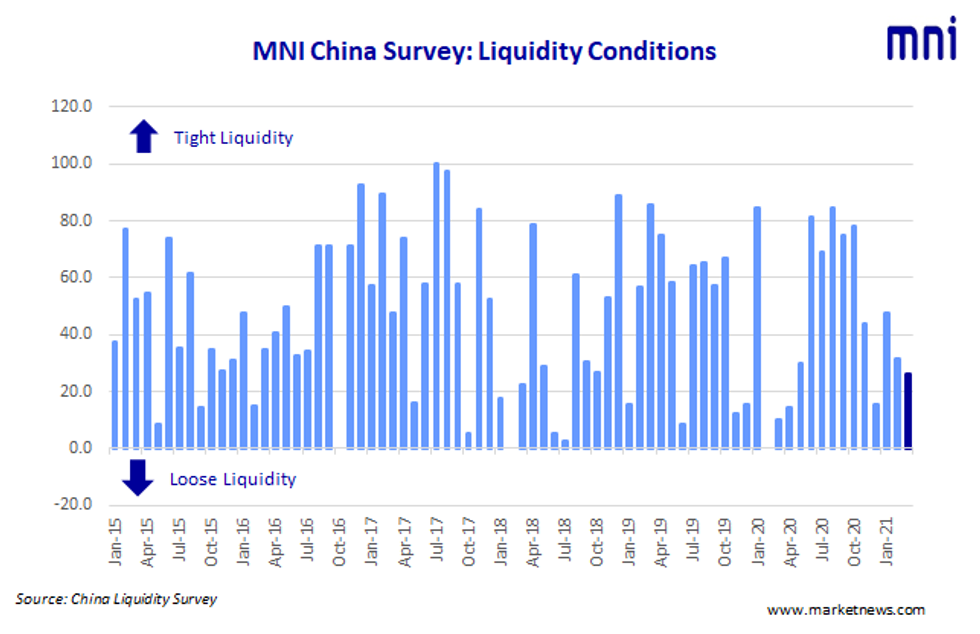

Liquidity conditions were little changed across China's interbank money markets in March as the People's Bank of China kept a firm grip on policy levers, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index eased lower for a second month, falling to 26.2 in March from 31.6 in February, with just over half of the traders surveyed reporting better condition compared to last month.

The higher the index reading, the tighter liquidity appears to survey participants.

"The (liquidity) conditions were quite stable in March with repo rates falling (further from January's peak), especially the short end rates," a trader with State-owned bank based in Nanjing told MNI.

"Though it's the quarter end when MPA (Macro Prudential Assessment) starts, lower bond issuance as well as increased financial expenditure can still hedge some of the tension," another trader in Tianjin said.

The central bank conducted CNY100 billion MLF in the month to hedge the equivalent maturity of MLF, and drained net CNY25 billion from the market via open market operations as of March 29, MNI calculated.

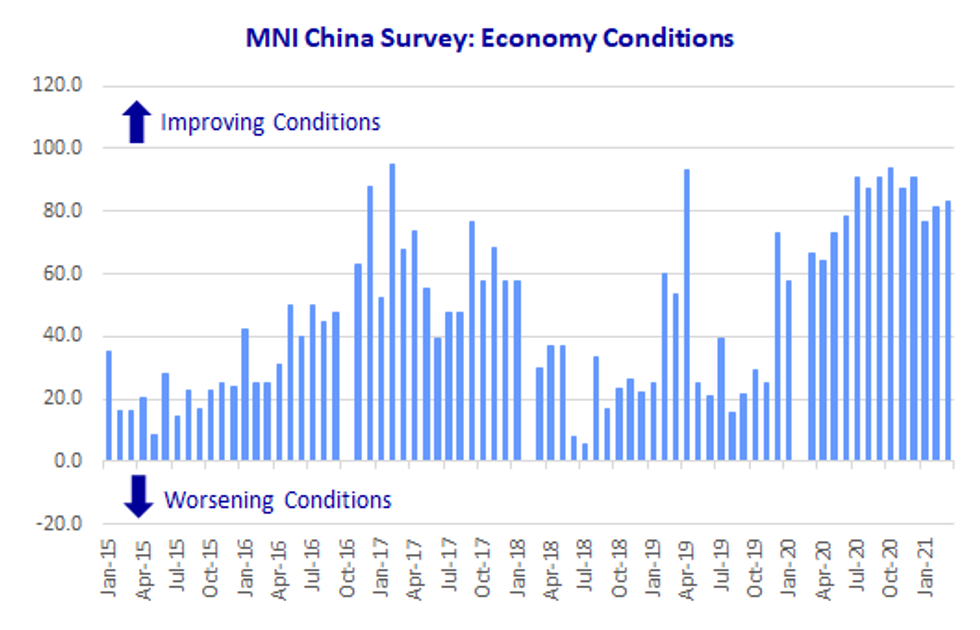

SUSTAINED RECOVERY

The Economy Condition Index inched higher to 83.3 in March from a previous 81.6, for an 11th reading above 70 level, with two-thirds of participants confident over the economic outlook, particularly with a quick COVID-19 vaccine roll-out.

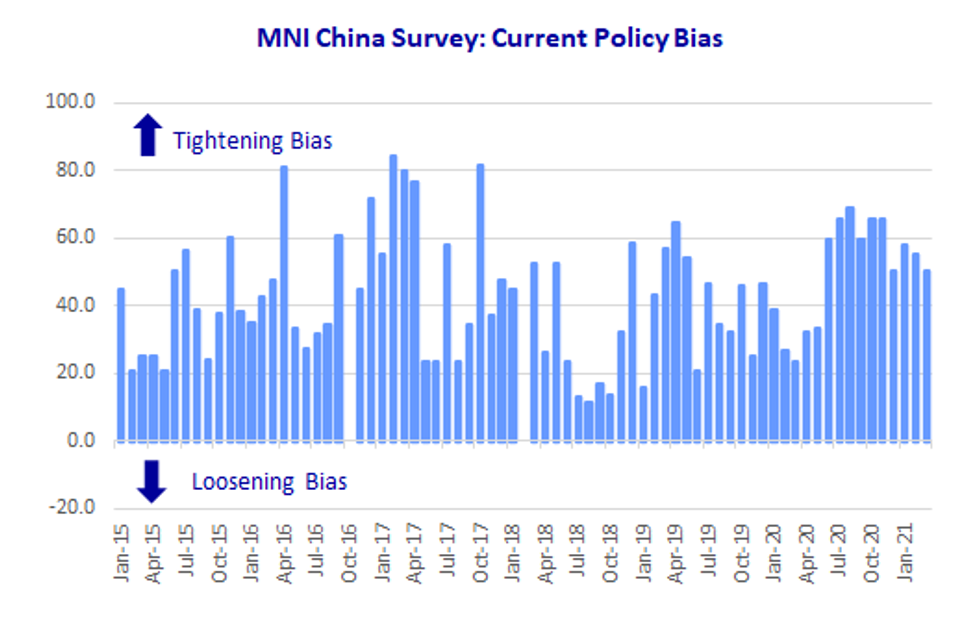

The PBOC Policy Bias Index came in at 50 in March, after standing at 55.3 in February, with just over 80% of traders clear on the policy stance. "The central bank will not allow a big fluctuation in the interbank market," one Beijing-based trader at the leading state-owned bank commented.

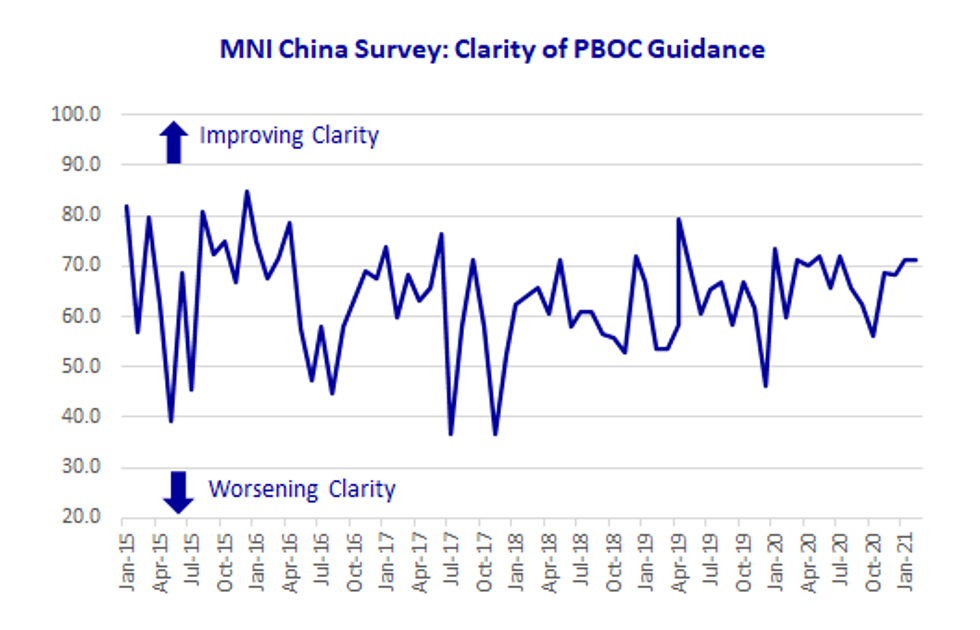

The Guidance Clarity Index was 71.4 in March, up from 71.1 in February, with 42.9% traders pointing to the PBOC's transparency. One Shanghai-based trader said the PBOC's operations underlined its aim to maintain the stability.

RATES

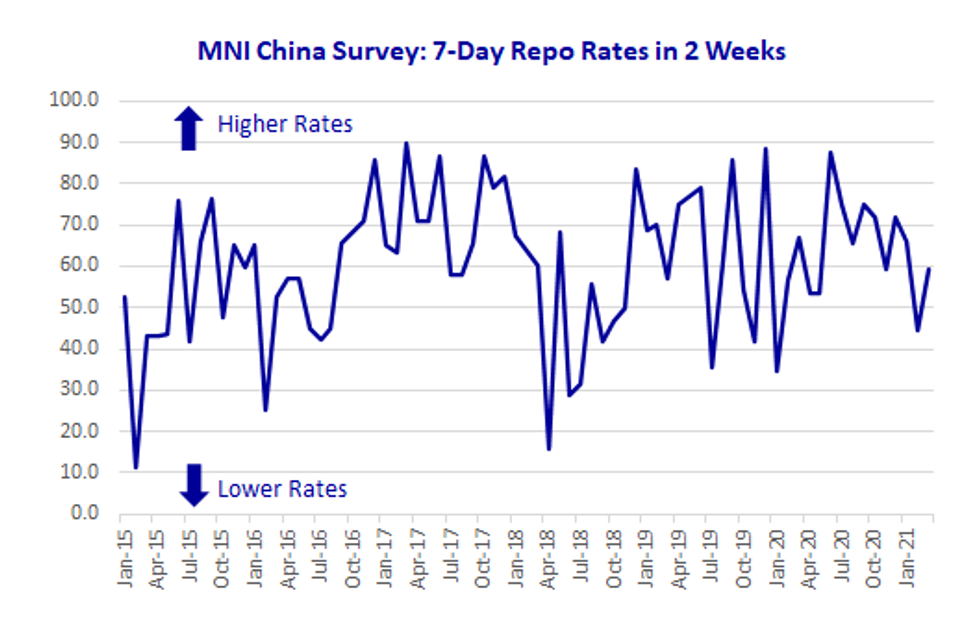

The 7-Day Repo Rate Index rose to 59.5 from 44.7, with 47.6% of the participants seeing rates higher due to a marginal tightening of conditions towards quarter-end. As liquidity normalizes, repo rates are not likely to move "too much away from 2.2%," a senior trader in Shanghai told MNI.

The 7-day weighted average interbank repo rate for depository institutions (DR007) ended Tuesday at 2.2435%.

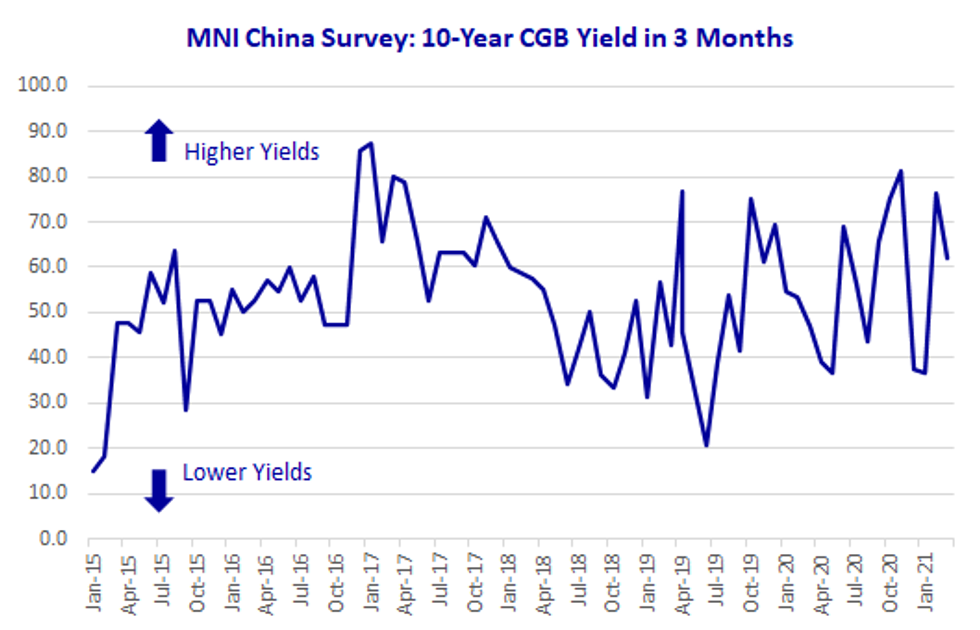

The 10-year CGB Yield Index, fell to 61.9 in March after the 76.3 reading in the previous month, with more than half of the traders seeing a reasonable volatility in future three months.

RRR CUT?

MNI added a special question of "do you think there will be a targeted RRR cut in the near future?" Nearly 60% of participants expect no move, pointing to ample liquidity at present.

The MNI survey collected the opinions of 21 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Mar 15 – Mar 26.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.