Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

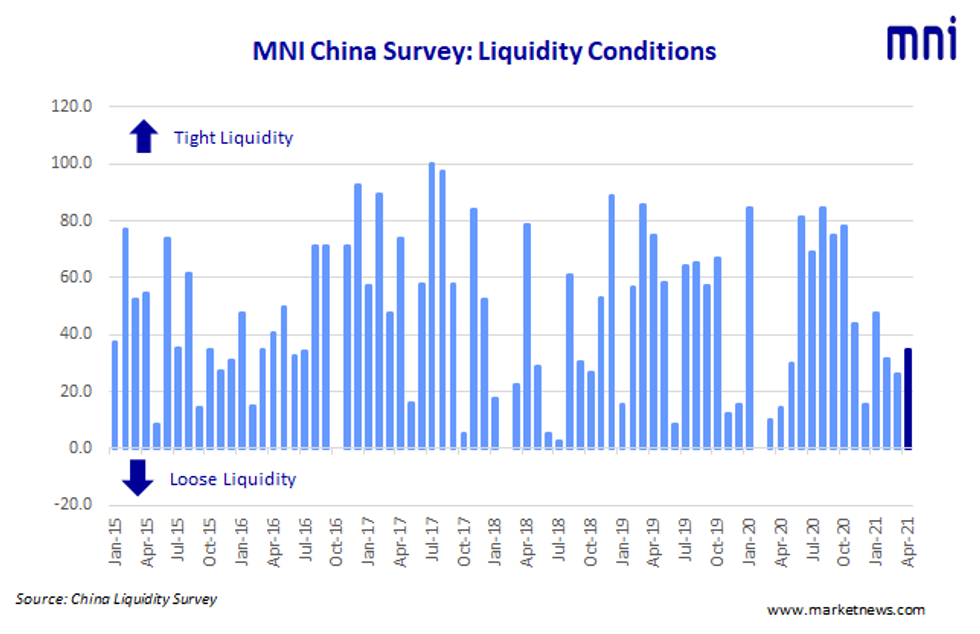

Liquidity conditions remained 'comfortable' across China's interbank market in April, helped by the People's Bank of China continuing with its moderately loose policy, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index rose for the first time in three months to 34.8 in April, up from 26.2 in March, with almost 70% of traders reporting "stable" conditions. The higher the index reading, the tighter liquidity appears to survey participants.

Despite increased government bond issuance, 'liquidity remained loose and the 7-day repo rate was kept around the policy rate of 2.2%," a trader with a state-owned bank based in Anhui told MNI.

"Recent open market operations are quite conservative," another trader in Nanjing said, noting the PBOC had done little but keep conditions stable.

SLOWING ECONOMY

The Economy Condition Index slid to 65.2 from 83.3 in March, the lowest reading in 12 months, on fears the the recovery is fading. Concerns are growing after the release of the Q1 GDP and other recent indicators.

"The slowing down industrial output data as well as the under-expectation manufacturing recovering, due to the increasing costs and production restriction under carbon emission requirement, might face increasing downward pressure in the second half," a trader based in Guangzhou concerned.

China's GDP rose 18.3% on a yearly basis, or 0.6% q/q, in the first quarter, below consensus. Retail sales rose 34.2% compared to the same period last year, making it the stand out data point to end Q1.

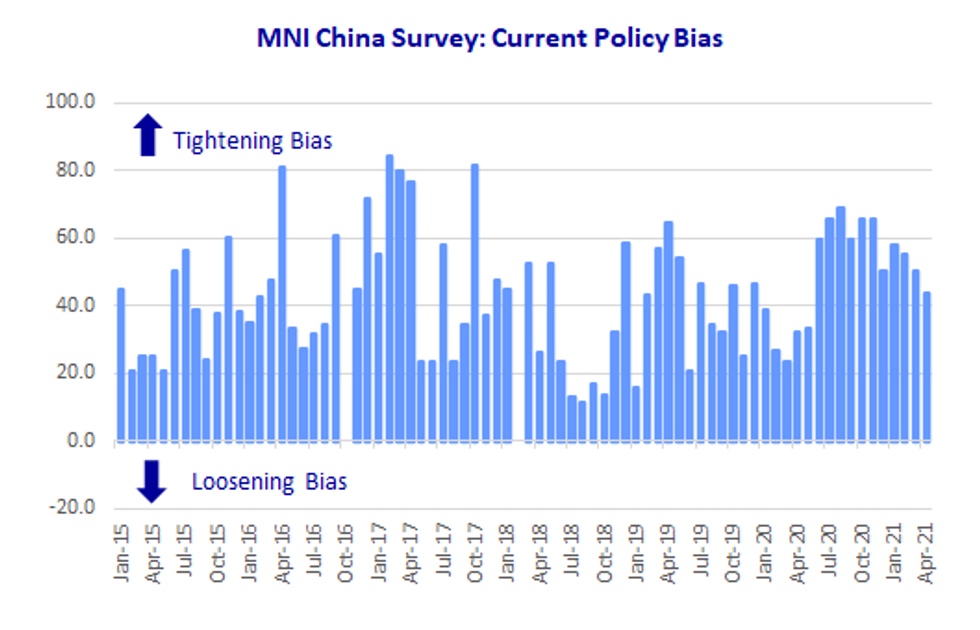

NEUTRAL POLICY

The PBOC Policy Bias Index stood at 43.5 in April, down from the breakeven 50 level seen in March, as more traders feel the current neutral monetary policy will be continued, with one Beijing-based trader seeing 'little possibility' of a rate or RRR cuts, although he didn't rule out more targeted policy moves.

Another trader with a state-owned bank told MNI the risk of higher inflation could impede the PBOC even if it did want to ease policy at all.

The Guidance Clarity Index reads at 67.4 in April, down from the 71.4 reading in March, with 65.2% traders smiling upon the more and more transparent guidance from the central bank.

RATES SLIDE

The 7-Day Repo Rate Index edged down to 56.5 from last 59.5, with almost 40% of participants seeing rates move higher due to end-month effect. The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.2087% Tuesday.

The 10-year CGB Yield Index, fell for a second month, dipping to 43.5 in April after 61.9 previously, with just over a quarter of traders seeing possible lower yields in the next three months.

INFLATIONARY PRESSURE

International commodity prices, including copper, aluminum, iron and ore and soybeans, have increased considerably since the start of the year, causing a direct rise in production costs. China's PPI rose 1.6%m/m in March, the biggest 1-month increase since 2002.

Asking "How do you think the inflation will affect the economy?" survey, almost 40% of traders saw modest inflation, although not impacting China's economy.

The MNI survey collected the opinions of 23 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Apr 12 – Apr 23.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.