Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

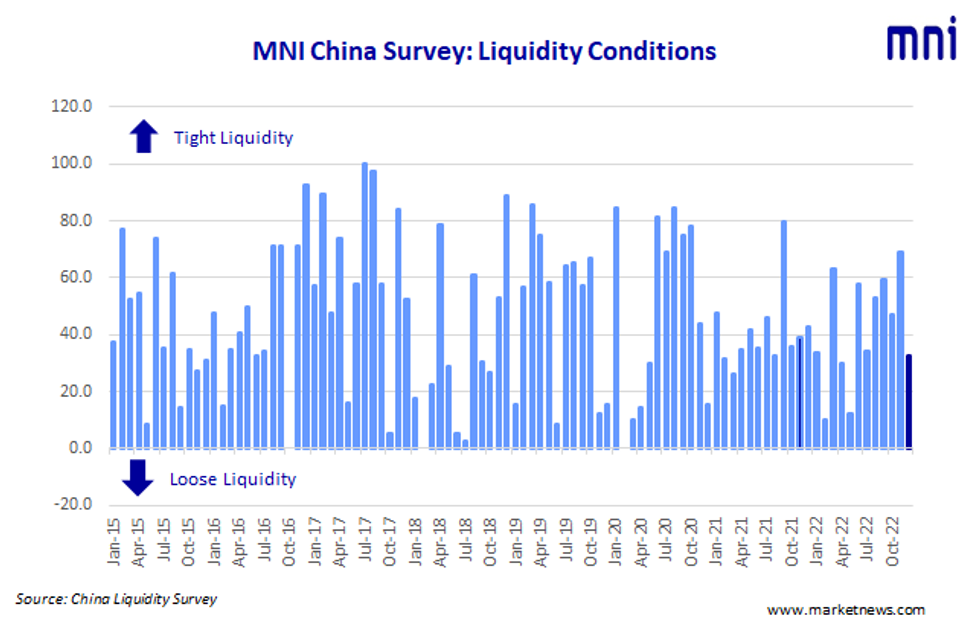

Liquidity across China’s interbank market looks ample to deal with year end factors, with no signs of a drying up of capital pools, the latest MNI Liquidity Conditions Index shows.

Unlike previous Decembers when liquidity usually tightens, the Liquidity Condition Index fell to 32.9 this time from last 69.1. Almost half of survey participants reported easier conditions, with an estimate of CNY500 billion capitals released by the Reserve Requirement Ration cut. The index marks the lowest reading since May.

The higher the index reading, the tighter liquidity appears to survey participants.

Besides the reserve cut, help from the fiscal side also helped, with lower bond issuance.

The People’s Bank of China conducted CNY650 billion MLF in December, injecting CNY 150 billion into the market after offsetting the maturity of CNY500 billion MLF. PBOC injected net CNY411 billion via its open market operation as of December 21, MNI calculated.

ECONOMY DIPS FURTHER

The Economy Condition Index stood at 27.1, following last month’s 26.5, with 57.1% of traders seeing a weakening economy.

China’s industrial output rose 2.2% y/y in November, dip further from the previous 5.0% y/y growth. Fixed asset investment rose 5.3% y/y in Jan-Nov period while retail sales falling 5.9% y/y in the month, registering a bottom in six months.

POLICY STAND

The PBOC Policy Bias Index reads at 37.1, following November’s 32.4 with 74.3% of the participants seeing the stance is not changing.

“We are still facing the inflation concerns, and the central bank is still working on stabilizing economic growth; a change of the stance is not a great possibility,” a senior trader familiar with the market told MNI.

China held the annual Central Economic Work Conference (CEWC) on 15-16 December, which laid out key tasks and economic policies for 2023. The meeting called for progress while maintaining stability next year, to continue to implement a proactive fiscal policy and a prudent monetary policy to promote high-quality development.

The Guidance Clarity Index stood at the breakeven in December, following the previous reading of 52.9. Traders are all agree with the transparency conveyed by the central bank.

RATES SLIDE

The 7-Day Repo Rate Index dropped to 18.6, quickly down from the previous 38.2, with 68.6% participants seeing the rate fall due to an abundance of funds.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 1.7692% Tuesday.

The 10-year CGB Yield Index read at 25.1 in December, lower from the previous 31.5 reading, with 34.3% traders predicting a sliding yield while another 17.1% seeing a rise of the curve.

“With the support of RRR cuts and PBOC’s injection, both 7-day repo rate and 10Y CGB yield are likely to fall back,” a trader based in coastal province Fujian commented.

RATE CUT?

Along with the carry out of the reserve cut, rate cut has drawn more market attentions. MNI tried to figure it out by adding a special question of “Do you think it’s likely to have a rate cut in future three months?” . 74.3% of the participants denied the possibility as inflation hinders.

“We should pay great attention to the potential increasing inflation and be very cautious using price based monetary policy tool (rate cut) during the recovering process,” the Beijing manager warned.

“It is not necessary to cut rate in short term as the economy recovery driven by rebounding consumption next year has been basically confirmed,” a Shanghai based analyst said.

The MNI survey collected the opinions of 35 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted December 5 – December 16.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.