Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

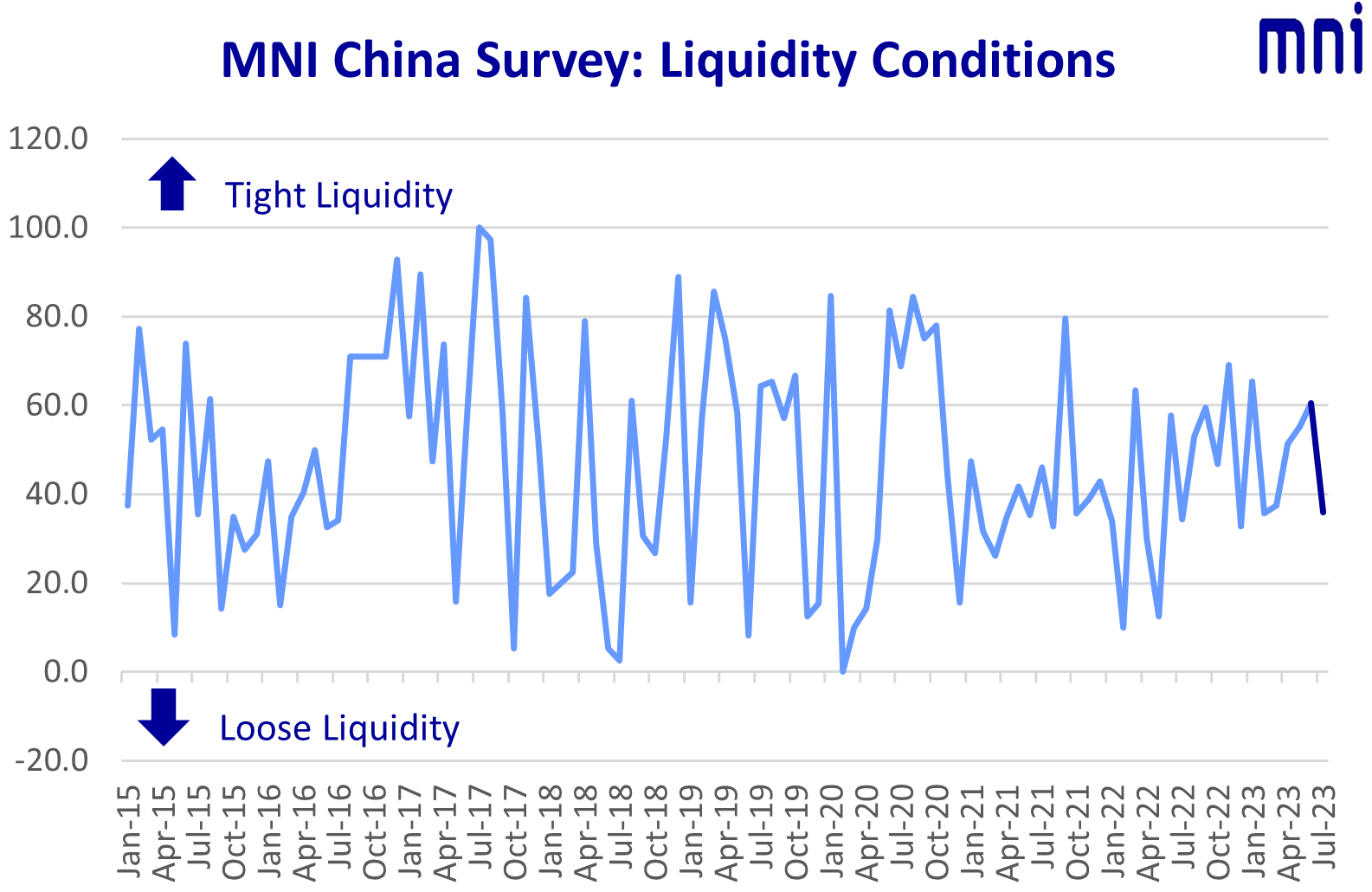

Chinese interbank liquidity eased in July breaking a five month run of tightening as banks released funds following end of H1's macro-prudential assessment, with traders expecting The People's Bank of China (PBOC) to maintain a loose environment to support the economy after economic sentiment dropped again, the latest MNI Liquidity Conditions Index shows.

The MNI China Liquidity Condition Index fell to 35.9 in July from 60.5 in June, the largest month-to-month change since February, with 46.2% of local traders reporting easing of conditions.

The higher the reading, the tighter liquidity.

“Liquidity has returned to the market after June ended, the overnight rate is likely to be maintained at or below 1%,” a trader with a big commercial bank based in Shandong told MNI.

The PBOC will maintain ample intermarket liquidity to ensure credit expansion and meet local government needs as they accelerate debt issuance, traders have told MNI. (See MNI PBOC WATCH: LPR To Remain Unchanged, H2 RRR Cut Possible - Bonds & Currency News | Market News)

The PBOC conducted CNY103 billion of MLF in July, injecting CNY3 billion into the market after maturities of CNY100 billion. It drained net CNY338 billion via open market operations as of July 25, MNI calculated.

The MNI China PBOC Policy Bias Index read 35.9 in July with 71.8% of local traders expecting a continuation of prudent monetary policy and 28.2% expecting further easing.

ECONOMY DOWN

The MNI China Economy Condition Index dropped to 37.2, down from 48.7 in June and the fifth consecutive month of decline, with 41.0% of traders seeing weaker conditions.

GDP grew by 6.3% y/y in Q2 in July, lower than market consensus of 7%, prompting a further decline in sentiment after a run of weak data in May and June. The Politburo signalled further policy support for the private sector and capital markets whilst maintaining prudent monetary policy and avoiding systemic risks on Monday. (See MNI BRIEF: China To Support Private Investment - Bonds & Currency News | Market News)

However authorities’ policy response may be limited by local governments’ heavy debts and poor market confidence, policy advisors and economists say. (See MNI: Weak Credit Demand Limits PBOC Easing, Fiscal Move Needed - Bonds & Currency News | Market News)

“The recovery is not smooth sailing” a trader in Beijing told MNI, expressing concern about the economy following Q2 GDP and export data.

“The PBOC could further ease policy to support the economy but any moves will be relatively restrained as authorities need to prevent and defuse risks,” a senior Shanghai fund manager told MNI.

RATES DOWN

The MNI China 7-Day Repo Rate Index fell to 38.5 in July compared with June’s 50.0, with 46.2% of traders seeing the rate curve dropping due to ample liquidity.

“There's a strong possibility conditions will be looser in Q3 if you look at the overall policy tone, so short-term rates won’t climb up sharply,” a Shanghai trader said.

The MNI China 10-year CGB Yield Index read 37.2, down from 46.1, with 38.5% of traders expecting a fall in the curve due to weak expectations and good liquidity, with 12.8% predicting a rise. “Long-end rates are likely to return below 2.65% if ample liquidity is sustained,” the Shandong trader predicted.

RRR CUT

Given recent market calls for more supportive policies, MNI’s July special question asked traders the probability of an RRR cut in the next three months. In total 46.2% said “very likely yes”, whilst 28.2% responded “not very likely”.

The central bank said it will implement prudent monetary policy and make cross-cycle adjustments to stabilise growth, employment and prices, at its recent Q2 monetary policy committee meeting.

Economists recently told MNI the PBOC may cut the RRR to lower real interest rates to accommodative levels given restrictions it faces on lowering the MLF. (See MNI PBOC WATCH: Lower Rates Seen For Existing Mortgage Holders - Bonds & Currency News | Market News)

The full report is here:

MNI China Liquidity Index July 2023.pdf

For full database history on the MNI China Liquidity Index™, please contact:sales@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.