Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

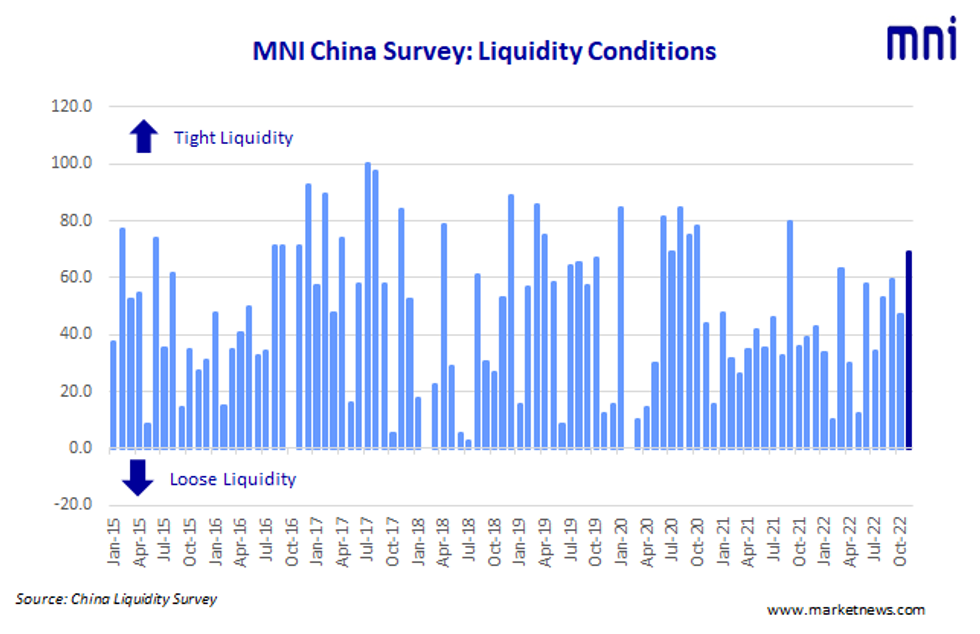

China’s interbank market liquidity conditions tightened in November, despite renewed Covid concerns, as the Peoples’ Bank of China, drained funds from the system, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index, surged to 69.1 from 46.9 last month, with over half of respondents reporting tighter conditions, especially in the first half of the month. The index marked the highest reading of the year.

The higher the index reading, the tighter liquidity appears to survey participants.

“(Liquidity) is tightening on PBOC draining and investors’ redeeming of capital assets,” a Shandong based trader with city commercial bank told MNI.

However, there were signs of improvement later in the months, with one trader at a state-owned bank based in Fujian said, as the central bank injected some liquidity into the market. The PBOC conducted CNY850 billion MLF in November, draining CNY 150 billion from the market after offsetting the maturity of CNY 1 trillion MLF. PBOC drained a net CNY827 billion via its open market operation as of November 29, MNI calculated.

COVID RETURNS

The Economy Condition Index, fell sharply to 26.5 in November, slumping from 53.1 in October, as views over the economy clouded, with the reading the lowest since April, with one Shenzen-based trader saying the 5.5% growth target could be missed.

China’s industrial output rose 5.0% y/y in October, slowing from the previous 6.3% y/y increase.

The PBOC Policy Bias Index stood at 32.4, down from 37.5 in October with 64.7% of the participants seeing the central bank’s stance unchanged.

“The prudent stance is not going to change, but the central bank has strengthened the implementation with more tools,” a senior analyst based in Beijing told MNI.

The People’s Bank of China announced a 25bps reserve requirement ration (RRR) cut last Friday. The move which will take effective on December 5 shall release an estimated CNY 500 billion into the banking system and aims at maintaining “reasonable and ample liquidity” in the real economy.

The Guidance Clarity Index stood at 52.9 in November, down from 59.4 last month, although the steady reading underlines the market’s satisfaction in understanding the central bank’s action.

RATES SLIDE

The 7-Day Repo Rate Index edged down to 38.2, compared with last 39.1 reading, with 52.9% participants seeing the rate is likely to fall from the high point along with the injection of the capitals.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 1.8788% Tuesday.

The 10-year CGB Yield Index stood at 31.5 in November, down from 46.9 previously, with predictions of the yield diverging further.

GROWTH TARGET

Given the strict Covid control measures and the markets increasing concern about the yearly economic target, MNI added a special question of “Do you think China will hit the year economy target?”.

A quarter of respondents are quite confident that China will hit the 5.5% goal while 61.8% are saying to achieve the goal will be of great challenge especially on back of increasing Covid cases disrupting the economy.

The MNI survey collected the opinions of 34 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted November 14 – November 25.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.