Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

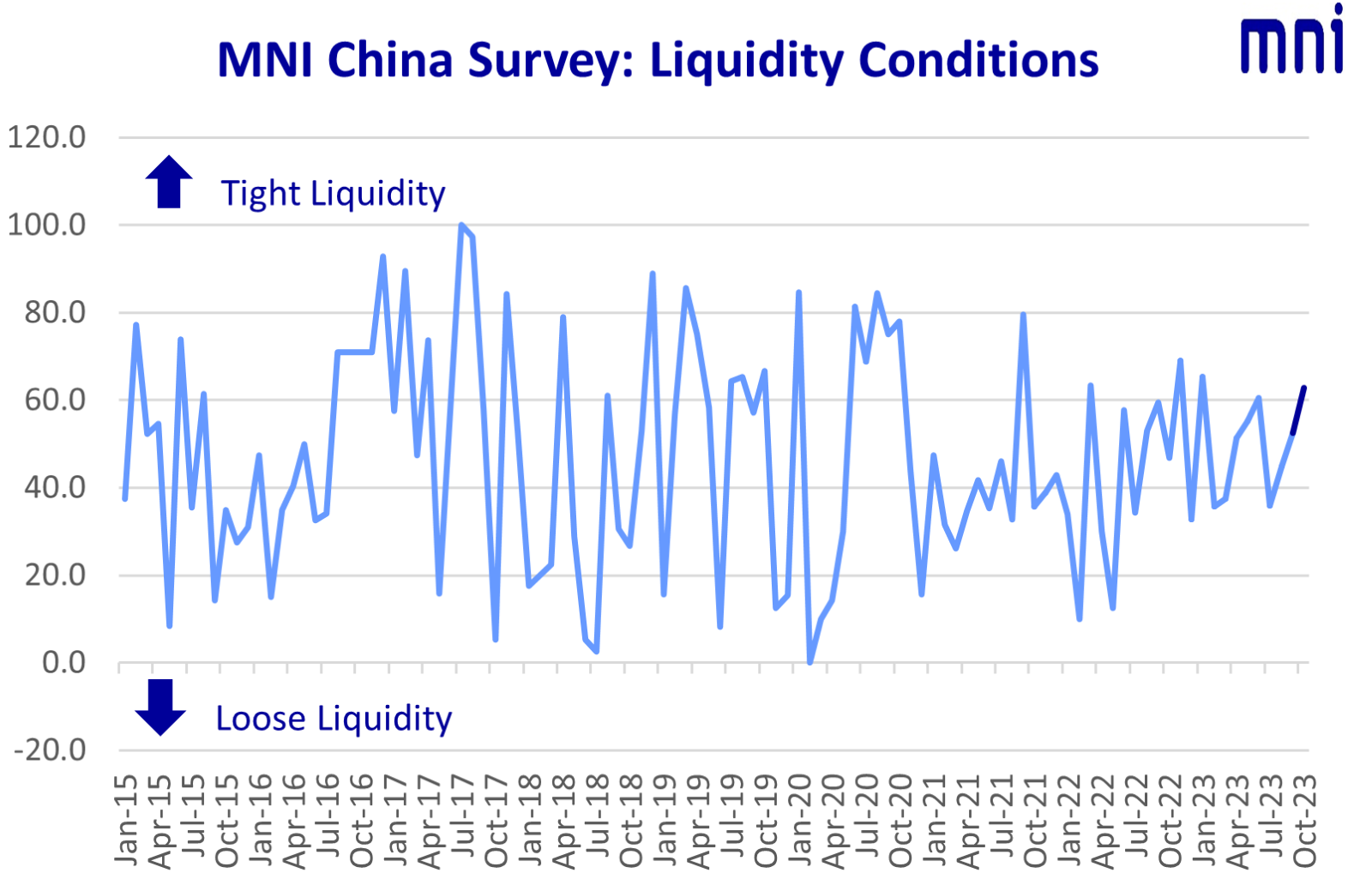

China’s interbank liquidity reached its tightest level since January as economic recovery gathered strength following mid-year lows, but the proportion of traders expecting further easing jumped ahead of key year-end policy meetings, MNI's latest China Liquidity Survey shows.

The Chinese economy grew by 4.9% y/y in Q3, beating market expectations of 4.5%, as production and consumption rebounded more than anticipated but weakness in real estate continued to drag down investment. (See MNI INTERVIEW: China GDP To Beat Expectations- Ex PBOC's Sheng)

The MNI China Economy Condition Index jumped to 69.2 in October, the highest since March, from 55.1 previously.

Despite strong data, a Beijing-based trader said Q4 rate and reserve cuts remain possible as authorities needed to secure economic momentum, and another trader expected more easing ahead of top level economic conferences. A total of 33.3% of respondents expected more easing with 66% expecting unchanged, the strongest anticipation of future easing since November last year.

The benchmark MNI China Liquidity Condition Index reached 62.8 in October, the tightest since January with 46.2% of traders reporting tighter conditions due to maturing reverse repos, tax payments and high government bond issuance.

One trader noted big bank net-lending helped liquidity earlier in the month but was overpowered by an estimated CNY1.5 trillion in government bond sales.

Given tightening liquidity, the People’s Bank of China last week provided CNY789 billion from its Medium-Term Lending Facility, injecting CNY289 billion the most for 33 months, after offsetting maturities of CNY500 billion. The PBOC also injected a net CNY265 billion via open market operations as of Oct 24, MNI calculated.

The former head of the PBOC Statistics department recently told MNI the PBOC should retain its easing bias and that there is still space for cuts in interest rates and reserve requirement ratios, though some experts told MNI the economy still faced weak credit demand, making RRR cuts less effective. (See MNI: Scope For China Fiscal, Monetary Stimulus Seen As Limited)

In a report to the State Council last week, Governor Pan Gongsheng said the PBOC would ensure more precise and powerful monetary policy and promote the sustained recovery with a focus on expanding domestic demand.

China is on track to achieve its 5% GDP growth target this year but domestic demand remains insufficient, according to Sheng Laiyun, spokesperson for the National Bureau of Statistics, after announcing Q3 GDP data.

RATES UP

Traders expected liquidity to remain tight with one trader saying the 7-day repo rate will climb but not sharply. The MNI China 7-Day Repo Rate Index rose to 51.3 in October, with 35.9% seeing rates increase due to tight conditions.

The MNI China 10-year CGB Yield Index reached 47.4, up from 39.7 in September, with 23.1% expecting rates to climb while 28.2% expected a fall. The yield is currently set to rise but may drop if there are more reserve or rate cuts, one trader said.

The full report can be found here:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.