Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

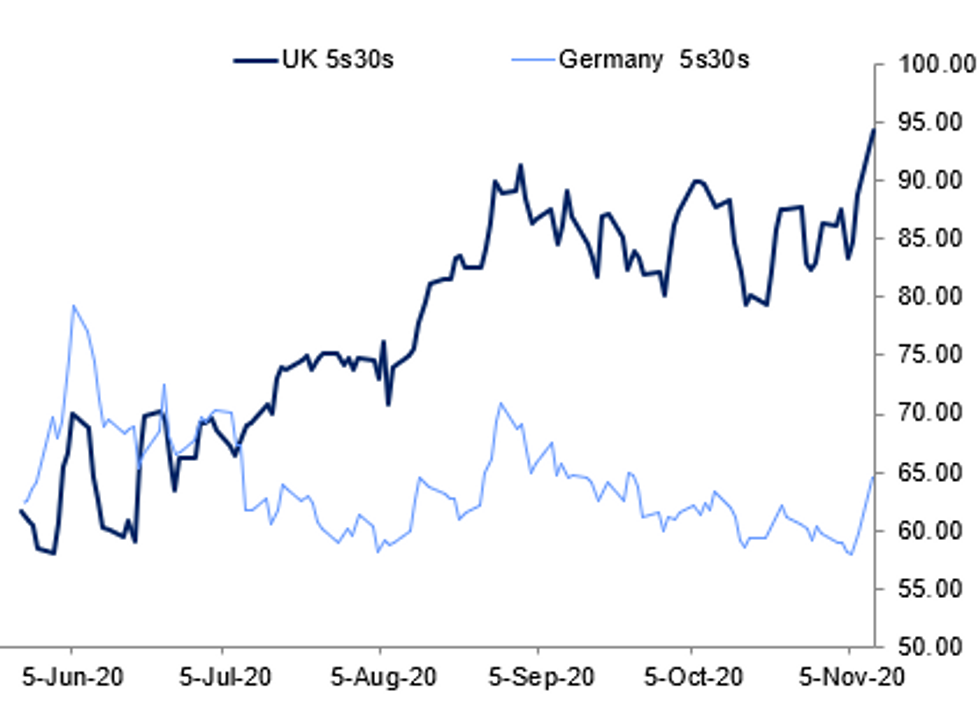

Fig. 1: Core Curves Steepen On Vaccine Hopes

BBG, MNI

BBG, MNI

- EGBs are lower across the board following the news that the Pfizer vaccine has seen 90% effectiveness in its stage 3 trial so far. The benchmark for passing the trial would have been 50% and 70% would have been considered a success so a 90% effectiveness has seen equities rally and fixed income bear steepen globally.

- 10-year Bunds are outperfoming both gilts and USTs but yields are still 9.3bp lower on the day at writing. Schatz yields have moved in line with UK yields, up 4.2bp at the time of writing with both having seen larger moves than 2-year Treasuries.

- Peripheral spreads are tighter across the board with the exception of Italy.The most noteworthy moves have been seen in Cyprus where 10-year spreads toBunds have narrowed 12bp. Positive Greek ratings news, Turkish political news and the vaccine news (helping tourism) have all been contributors.

- BTP futures are down -0.94 today at 149.67 with 10y yields up 10.0bp at0.739% and 2y yields up 5.7bp at -0.369%.* OAT futures are down -1.07 today at 169.14 with 10y yields up 7.8bp at-0.279% and 2y yields up 1.9bp at -0.681%.

GILT SUMMARY: Vaccine Hopes Drives Curve Steepening

News that Pfizer may have an effective Covid Vaccine triggered a sharp equity rally and hefty bear steepening of the gilt curve.

- The gilt curve had initially bull flattened early in the session before the Pfizer news broke. Gilt cash yields are now 5-12bp higher on the day with the 2s30s spread 7bp wider. Last yields: 2-year 0.0062%, 5-year 0.1595%, 10-year 0.3787%, 30-year 0.9754%.

- The Dec-20 gilt future trades at 134.27, just one tick off the day's low in what has been a wide intraday range (L: 134.26 / H: 135.97).

- The short sterling futures strip has steepened with greens/blues up 5.5-8.5 ticks.

- The BoE earlier purchased GBP1.463bn of short-dated gilts with offer-to-cover of 3.47x.

- Tomorrow sees the release of jobless claims data for October and employment/wage data for September.

DEBT FUTURES/OPTIONS:

- LH1 100.25c, bought for half in 2.5k

- 0LH1 100/100.12cs vs 99.875p, sold the put at 1.25 in 10k

- RXF1 175/174ps, bought for 11 in 2k

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok