Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Equities bid in Asia, broader markets calm after Wednesday's shocking scenes in DC, with the Capitol secured and approval of the Electoral College results moving forwards.

- Oil pushes on to fresh multi-month highs.

- Raft of Fedspeak due on Thursday.

BOND SUMMARY: Light Pressure In The Main During Asia Hours

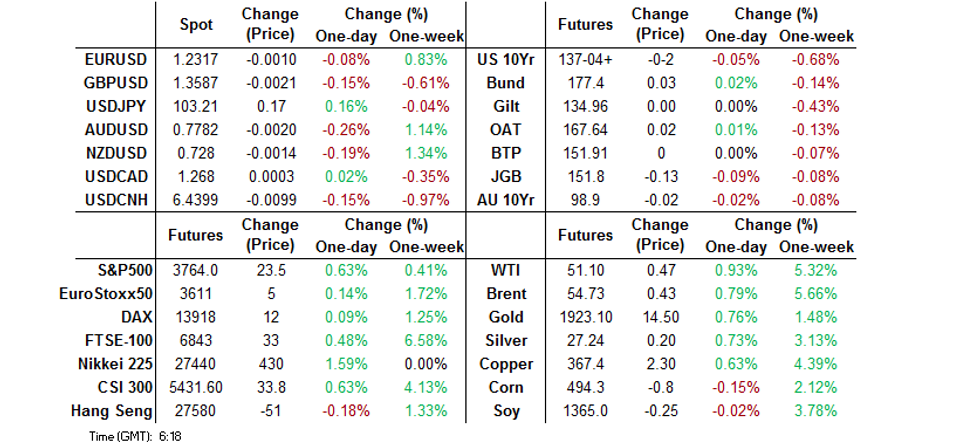

T-Notes held to a 0-05 range overnight, last -0-01+ at 137-05, with a sense of normality coming back to the fore re: procedural matters in DC, as GOP Senators rolled back their objections to the certification of the Electoral College count with the Capitol re-secured . Still, calls for impeachment of Trump have become evident, while there are suggestions that senior members of Trump's staff could resign from their roles in the coming days. Potential Asia-Pac buyers haven't shown their hand, with the fiscal dynamic in the U.S. perhaps sidelining them (as we suggested may be the case earlier). The curve has bear steepened, with 30s sitting 1.6bp cheaper vs. closing levels at typing, a little off cheapest levels of the day. On the flow side, 20K block buying of the TYH1 136.50/136.00/135.50 put ladder headlined, with focus on low vol, relatively nearby downside exposure now spreading to the H1 expiries.

- JGB futures finished -13 ticks, softening further in afternoon trade, while the cash curve saw some twist flattening as the super long end was initially more concerned by the impending state of emergency declaration in Tokyo & the surrounding areas (details were outlined by COVID response chief Nishimura and met expectations that were a product of recent press reports), while the shorter end looked to the dynamic of global FI markets. The super-long end faded then from best levels as we moved through the day. Elsewhere, local monthly wage data was much softer than expected, in both headline and real terms. 30-Year JGB supply headlines locally on Friday.

- More attractive FX-hedged entry points for Japanese investors may have provided some support for the Aussie bond space in early Sydney trade, before the broader impetus resulted in some fresh, albeit light, pressure for the space, with YM -1.0 and XM -2.0 at the bell, while the cash curve bear steepened. Swaps were generally flat to tighter vs. ACGBs. Elsewhere, Australian PM Morrison outlined Australia's COVID-19 vaccination strategy, while local data provided nothing in the way of notable impetus for the space.

FOREX: G10 FX Stabilise, Congress Resumes Certification Process

G10 FX held tight ranges in the Asia-Pac session, struggling to find a coherent sense of direction, with all eyes on the Capitol Hill, where the U.S. Congress resumed the process of certifying the results of the 2020 presidential elections. Several GOP lawmakers pulled back from earlier commitments to oppose the results, as the dust started to settle after yesterday's turmoil in DC.

- JPY slipped ahead of the expected declaration of emergency in Tokyo and neighbouring prefectures, with Japanese media reporting that PM Suga will hold a presser on the matter this evening. Elsewhere, Japanese wages fell faster than exp. in Nov.

- PBOC fixed USD/CNY at CNY6.4608, slightly weaker for the yuan than yesterday after strengthening for a total of 645 pips in 2021 so far. The central bank continued its post New Year drain, withdrawing CNY 110bn from the financial system, which equates to a net drain of CNY510bn this week. USD/CNH faltered, albeit yesterday's low remained unthreatened.

- Indonesian rupiah softened after Indonesia moved to implement tighter movement restrictions in Java and Bali. USD/IDR tested weekly highs and its RSI crossed above the 30 (overbought) level, sending a bullish signal.

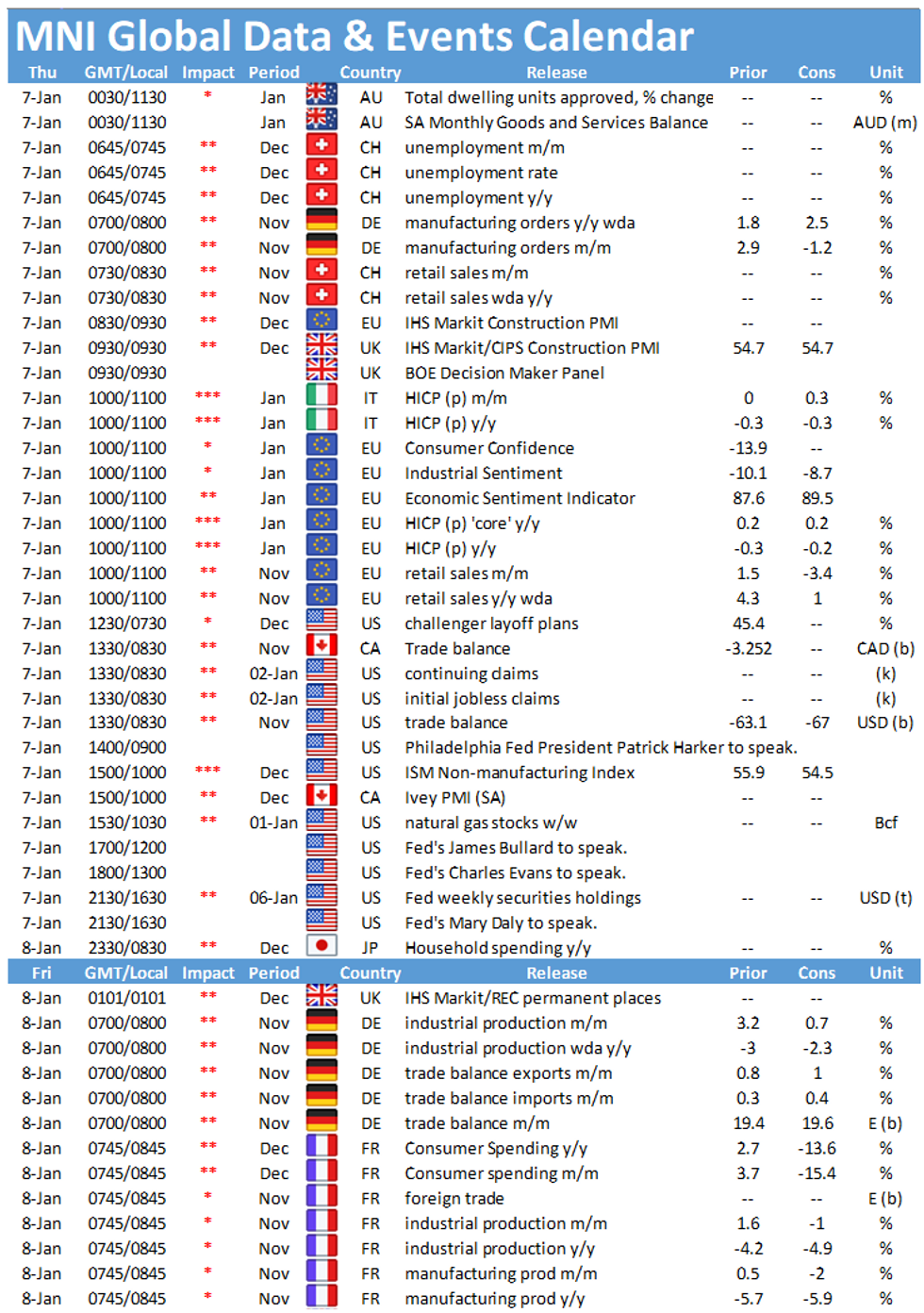

- Focus moves to U.S. initial jobless claims & ISM Services, flash EZ & Italian CPIs, German factory orders as well as Fedspeak from Harker, Barkin, Bullard, Evans & Daly.

FOREX OPTIONS: Expiries for Jan07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2155(E1.3bln-EUR puts), $1.2250(E727mln-EUR puts), $1.2300(E411mln), $1.2340-50(E499mln), $1.2700(E924mln-EUR puts)

- USD/JPY: Y102.50-60($640mln), Y103.20-25($794mln), Y103.70($670mln-USD puts), Y104.00($1.2bln)

- EUR/GBP: Gbp0.8800(E1.1bln-EUR puts), Gbp0.8850(E649mln), Gbp0.9300(E510mln)

- AUD/NZD: N$1.0690(A$640mln-AUD puts)

- USD/CNY: Cny6.4894($500mln-USD puts), Cny6.50($555mln), Cny6.5960($500mln)

EQUITIES: Firmer Overnight

Equities have generally firmed in Asia-Pac hours, although the major e-mini contracts have stuck to the ranges established on Wednesday, with a sense of normality returning to DC after Wednesday's shocking scenes.

- The process of certification of the results from the U.S. electoral has resumed, with some notable GOP Senators removing their previously outlined opposition to the results.

- The Hang Seng was the exception to the broader rule, after a WSJ report noted that "U.S. officials are considering prohibiting Americans from investing in Alibaba Group Holding Ltd. and Tencent Holdings Ltd."

- As a reminder, Wednesday saw the NYSE finally decide that it will remove the ADR listings of the 3 major Chinese telecoms firms targeted by President Trump's executive order.

- Nikkei 225 +1.6%, Hang Seng -0.8%, CSI 300 +0.3%, ASX 200 +1.6%.

- S&P 500 futures +23, DJIA futures +154 NASDAQ 100 futures +100.

GOLD: Some Pressure From The Blue Wave Narrative

The uptick from lows in U.S. real yields has applied pressure to bullion over the last 24 hours, but bears have failed to force their way below $1,900/oz, with spot last dealing little changed on the day around the $1,920/oz mark. A break below the psychological $1,900/oz level (which has limited significance at present) would have bears looking to the 20-day EMA.

OIL: Fresh Multi-Month Highs

WTI & Brent sit ~$0.40 above their respective settlement levels, benefitting from the broader uptick in equity markets in Asia-Pac hours, geopolitical tension surrounding Iran and spillover from the large drawdown in headline crude stocks seen in Wednesday's DoE inventory report, although the large builds on the product side of the equation tempered the post-release reaction re: the latter (the figures were roughly in line with what was seen in Tuesday's API inventory estimates, at least in directional terms, if not outright levels).

- Elsewhere, that latest RTRS OPEC survey, released Wednesday, was a little less bullish as it revealed that "OPEC oil output rose for a sixth month in December, a Reuters survey found, buoyed by further recovery in Libyan production and smaller rises elsewhere in the group… The OPEC producers bound by the (OPEC+) supply deal also boosted output in December, the survey found, which meant their compliance with agreed output cuts slipped to 99% from 102%."

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.