Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

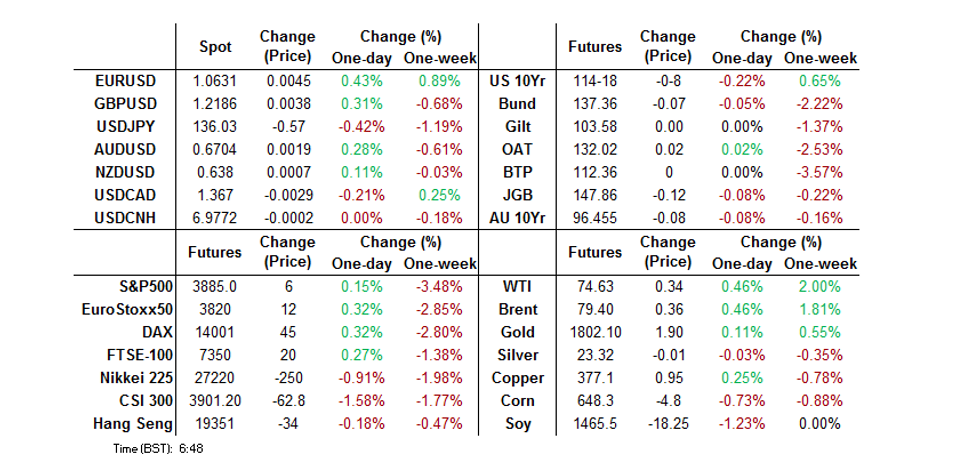

- The BoJ rumour mill was in full effect over the weekend, with Kyodo sources noting that the Japanese government is set to revise the BoJ accord that commits the Bank to achieving 2% inflation at “the earliest possible date.” The piece suggested that the new mandate would be more flexible around the 2% goal, which could potentially become a medium- or longer-term target. Kyodo went on to note that the matter is expected to be discussed with the new BoJ Governor (Kuroda’s term comes to an end in April). This resulted in weakness for JGBs and swap spread widening across most of the curve during the Tokyo morning. Japanese Chief Cabinet Secretary Matsuno subsequently pushed back against the need for a change in the accord, which put a bit of a bid back into JGBs in the early rounds of afternoon dealing, although that impulse has faded as we work towards the close.

- The USD is lower to start the week, but up from session lows. The BBDXY was last around 1262.50, -0.15% for the session. Much of the focus has been on the yen, following weekend reports of a possible shift in the BoJ's inflation mandate.

- Coming up, we have ECB speak and German IFO data. In the US the NAHB index prints.

US TSYS: Early Cheapening Holds, BoJ Matters Dominate Asian Session

TYH3 deals at 114-18+, -0-07+, 0-02 away from the base of its 0-06+ range on volume of ~60K.

- Cash Tsys are dealing 0.5-3.0bp cheaper, with 10s leading the cheapening.

- Tsys were softer at the open as the reaction to a source report from Kyodo re: the possible revision to the Japanese gov’t-BoJ accord applied some moderate pressure on increased speculation re: nearer dated BoJ policy tweaks (early in the post-Kuroda era, with his term set to conclude in April) and related spill over from JGBs.

- Japanese Chief Cabinet Sec. Matsuno subsequently pushed back against the need for change in the accord allowing Tsys to tick away from session cheaps, before they re-cheapened into the London handover, with TY futures retesting their early Asia lows at one point.

- In Europe today we have a thin data calendar, save the latest IFO survey from Germany, although there will be some focus on the ECB speakers that are slated, given last week’s hawkish guidance from President Lagarde and the increased cross-market impact witnessed during ’22. European & U.S. digestion of the BoJ speculation & subsequent government denial will also factor into price action. Further out we have the latest NAHB House Market Index reading.

JGBS: Pressured By Speculation Surrounding Changes To BoJ Policy Accord

JGB futures are -11 into the bell, with the major cash JGB benchmarks running little changed to 6bp cheaper as the curve steepens (10s are capped by the BoJ’s YCC settings).

- The BoJ rumour mill was in full effect over the weekend, with Kyodo sources noting that the Japanese government is set to revise the BoJ accord that commits the Bank to achieving 2% inflation at “the earliest possible date.” The piece suggested that the new mandate would be more flexible around the 2% goal, which could potentially become a medium- or longer-term target. Kyodo went on to note that the matter is expected to be discussed with the new BoJ Governor (Kuroda’s term comes to an end in April). This resulted in weakness for JGBs and swap spread widening across most of the curve during the Tokyo morning.

- Japanese Chief Cabinet Secretary Matsuno subsequently pushed back against the need for a change in the accord, which put a bit of a bid back into JGBs in the early rounds of afternoon dealing, although that impulse has faded as we work towards the close.

- Note that our policy team has flagged its understanding that “the Bank could discuss changes to its easy policy framework as early as June, with a mid-year timeframe allowing the new Governor time to conduct a policy review and assess wages growth.”

- Sub-2.00x offer/cover ratios across the BoJ’s 1- to 25-Year Rinban operations also helped the early afternoon bid.

- The latest BoJ monetary policy decision headlines on Tuesday, with no changes expected (our full preview of that event will cross in the next few hours).

AUSSIE BONDS: Cross-Market Flows Aid Cheapening Impulse

Aussie bonds struggled to catch a bid during Monday’s Sydney session.

- At one point we saw an extension of the steepening/weakness observed earlier in the session, with a lack of headline drivers evident. Cash ACGBs were 4.5-9.5bp cheaper across the curve at the close, while YM settled -5.0 with XM -8.0, after weakness in the latter extended through its overnight session base, pushing a pure flow element to the fore.

- Building on the flow-centric nature of the move is the fact that the AU/U.S. 10-Year yield spread is showing above 0bp, as Aussie 10s widen vs. their U.S. counterpart (that spread hasn’t closed in positive territory since mid-October). This triggered RBC into issuing a tightener recommendation in that spread. ACGBs also notably underperformed vs. NZGBs.

- Note that YM pulled lower into the close, in what looked like a liquidation of longs at first glance, although the widening of 3-Year EFP alongside the move suggested swap payside flows were also evident.

- Bills finished +2 to -4, twist steepening, with little movement noted in RBA dated OIS vs. Friday’s late Sydney levels.

- There wasn’t much in the way of meaningful idiosyncratic news flow, with headlines dominated by PM Albanese noting that Foreign Minister Wong will visit China on Tuesday.

- The minutes covering the most recent RBA monetary policy meeting headline the local docket on Tuesday.

NZGBS: Early, Modest Cheapening Reverses

NZGBs faded the early cheapening/steepening, with (delayed) impact from soft domestic data and yield appeal (outright and cross-market) perhaps at play, leaving the major NZGB benchmarks 2-3bp richer across the curve at the bell, with bull steepening in play.

- Receiver-side flows in swaps would have also aided the richening, with swap spreads little changed to a touch tighter across the curve (bull steepening was also observed on the swaps curve).

- The major RBNZ dated OIS pricing in the front end of the strip is little changed, with ~70bp of tightening priced for the Feb ’23 meeting, alongside a terminal OCR of ~5.55%.

- Local data flow saw a lower rate of expansion in the services PMI reading alongside a record low Q4 consumer confidence reading in the latest Westpac survey.

- The NZGB space was more resilient to speculation surrounding the BoJ vs. global counterparts, with some AU/NZ cross-market trades perhaps lending support as ACGBs struggled and NZGBs outperformed.

- Looking ahead, Tuesday’s local docket is headlined by the monthly round of ANZ business and consumer confidence readings.

FOREX: USD Lower, JPY and AUD Higher

The USD is lower to start the week, but up from session lows. The BBDXY was last around 1262.50, -0.15% for the session. Much of the focus has been on the yen, following weekend reports of a possible shift in the BoJ's inflation mandate.

- USD/JPY dipped to a low of 135.77 before support emerged. The Japanese Cabinet Secretary pushed back on any change to the BoJ mandate. This took us off the lows and we last tracked around 136.20, with firmer UST yields at the back end arguably providing some support.

- AUD/USD has tracked high as well but has lost momentum this afternoon. The pair was last around 0.6705, still +0.30% for the session. News that Australian Foreign Minister Wong will visit China on Tuesday provided some support, although only at the margins.

- NZD/USD has been a laggard, last around the 0.6370/75 region, flat for the session. Weaker domestic survey data has likely weighed, with the Westpac Consumer Sentiment Index dropping to a record low. The AUD/NZD cross is back above 1.0500, last at 1.0515.

- EUR/USD is back above 1.0600 +0.20% for the session.

- Coming up, we have ECB speak and German IFO data. In the US the NAHB index prints.

AUD: A$ Correlations Weaken With Yield Spreads/Iron Ore, Firmer Elsewhere

AUD/USD correlations with yield differentials have dipped in the past week, but remain positive for the past month. The table below presents the levels correlations for AUD/USD and key macro drivers over the past week and month.

- Higher AUD/USD levels today (+0.43%, the best performer within the G10 space) look to be associated with better yield spread momentum against the US. Still, the AUD is slightly lower in the past week as yield momentum has improved, which explains the correlation result.

- In contrast, correlations with global commodities and base metals are quite firm, although more so for the past week rather past month. Iron ore's correlation has dipped though.

- The correlation with global equities remains quite high, less so for the VIX in recent weeks.

Table 1: AUD/USD Correlations

| 1wk | 1mth | |

| 2yr yield differential | -0.87 | 0.42 |

| 5yr yield differential | -0.94 | 0.36 |

| 10yr yield differential | -0.94 | 0.17 |

| Global commodity prices | 0.89 | -0.09 |

| Base metals | 0.81 | 0.60 |

| Iron ore | -0.75 | 0.36 |

| Global equities | 0.89 | 0.52 |

| US VIX index | -0.47 | -0.28 |

Source: MNI - Market News/Bloomberg

NZDJPY: Bullish Trend Intact, Relative Rates Outlook Still Supportive

NZD/JPY prints at ¥86.94, shy of the cycle high seen on 13 Dec at ¥88.17.

- The pair briefly traded through its 20-day EMA in early dealing today before finding support at ¥86.57 at the base of its bull channel that the pair has been in since 11 Oct.

- Despite the aforementioned report over the weekend of a possible revision of the BOJs inflation accord, which was subsequently denied by Cabinet Sec. Matsuno, rate divergence looks set to continue, at least in the near term.

- OIS markets are pricing ~70 bps of tightening into February's RBNZ meeting, with a terminal rate at ~5.55%. The BOJ on the other hand is expected to keep its Policy Balance Rate at -0.1% and 10-Yr Yield Target at 0.00% when they meet tomorrow (the MNI BOJ Preview will be available in the London Session today).

- NZD bulls will be targeting a break above the cycle high ¥88.17, opening up the bull channel resistance at ¥90.94. Bears will target a break through the bull support to test the 50-day EMA at ¥86.09.

Source: MNI - Market News/Bloomberg

ASIA FX: USD Weakness Not Uniform To Start The Week

Not all USD/Asia pairs are following the lead from the G10 space, with a number of pairs bucking the softer USD trend. USD/CNH is the mostly notable seeing some support today. In terms of tomorrow's session, the focus is likely to rest on the China LPR decisions, with the consensus looking for no change, although some forecasters see risks of the 5yr rate coming down by 10bps (currently at 4.30%). Also out is Taiwan export orders.

- USD/CNH has tracked a narrow range today, last above 6.9850, slightly higher for the session. The CNY fix came out a touch weaker than expected, while onshore equities are lower. Concern around the domestic covid situation outweighing optimism on the growth outlook for next year.

- 1 month USD/KRW has traded with a softer bias for much of the session, but we are now back to the 1300 level, still -0.70% for the session. Onshore equities are weaker (-0.50%), but hedging flows by NPS could be providing a positive offset. Late last week it was announced NPS would raise its hedges on offshore assets to 10% from the current 0.

- USD/THB is down around 0.35%, with the pair continuing to find selling interest above 35.00. We last tracked around 34.85, slightly above session lows around 34.735. BoT commentary reiterated recent guidance on the monetary policy outlook.

- USD/IDR hasn't been unable to find much downside traction. The pair last near 15630, +0.20% on closing levels from last week. Onshore equities are weaker, -0.40% at this stage. Offshore investors have sold close to a $1bn of local shares so far this month. The BI decision comes later this week, with +25bps expected.

- USD/PHP is lower, last near 55.41, -0.28% for the session so far. FX markets are shrugging off a weaker equity lead (-1.30%), with the authorities talking about a robust growth backdrop in Q4., which may help the country exceed its 6.5-7.5% growth target, a positive offset. Remittance inflows ahead of year end is another positive being cited.

EQUITIES: Most Markets Follow US/EU Lead Lower

(MNI Australia) Most regional equity markets are down at the start of this week, in line with US/EU bourse weakness from Friday's session. US equity futures are tracking higher but are only just in positive territory at this stage and comfortably down from best levels.

- Hong Kong equity market sentiment has again been volatile. Early positive sentiment in the tech index couldn't be sustained, with the sub-index last down 0.43%, (gains were above 2% earlier). The overall HSI is tracking -0.5% lower at this stage. Property stocks have also weighed amid fears of further fund placements by developers.

- Mainland China stocks are also down, the CSI 300 off by 1%. Covid fears are still weighing, as Shanghai will close most schools amid surging case numbers. The conclusion of the CEWC meeting, which vowed to boost domestic demand next year, has been offset by the headwinds.

- Tech sensitive plays are mostly lower, with the Nikkei 225 down over 1%.

- The Philippines main bourse is down 1.44%, mainly due to PDLT weakness amid reports of governance/budget issues.

- Indian shares, +0.40% in the first part of trading are one of the few positive stories in the region today.

GOLD: Moving Sideways At the Start Of The Week

Gold tracked higher in the first part of the session before losing some momentum. We got to a high close to $1797, before moving lower. We currently sit around $1793, little changed from NY levels at the end of last week. This leaves the precious metal slightly underperforming USD weakness today (BBDXY -0.20%).

- Overall, gold continues to respect recent ranges. Support continues to be evident around the $1775 level. Bulls likely need to see a sustained break of $1800 to turn more constructive.

- ETF gold holdings ticked higher at the end of last week.

OIL: Brent Can't Hold Above $80/bbl, But Still A Positive Start To The Week

Brent crude is starting the week on a firmer footing. We are up around 1% at this stage, tracking at $79.80/bbl (earlier highs were just above $80.50/bbl). This of course comes after late weakest towards the end of last week (-4.5% down through Thur/Fri trading). WTI is also 1% higher for the session, last trading just above $75/bbl.

- Market sentiment has been buoyed by China's growth plans for next year, particularly around reviving consumption/domestic demand. The other positive cited is the rebuild of strategic petroleum reserves by the US government, following releases earlier this year.

- Still, it remains to be seen if these factors can generate a sustained turnaround. Weaker US survey data from the Friday session last week has raised fears as we progress into 2023. Other indicators like prompt spreads also don't suggest near term tightness from a supply standpoint.

- The focus in the London/EU time zone is likely to be the EU energy ministers meeting, which is aimed at agreeing to a gas price cap level.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/12/2022 | 0800/0900 |  | EU | ECB de Guindos Speech at Economia Forum | |

| 19/12/2022 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 19/12/2022 | 1000/1100 | ** | | EU | Construction Production |

| 19/12/2022 | 1100/1100 | ** |  | UK | CBI Industrial Trends |

| 19/12/2022 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 19/12/2022 | 1500/1000 | ** |  | US | NAHB Home Builder Index |

| 19/12/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 19/12/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.