Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Bonds and Equities rangebound in Asia ahead of NFPs.

- Oil firms in wake of OPEC+ short-term pact.

- Brexit talks set to continue over the weekend, with familiar sticking points still in

BOND SUMMARY: A Pre-NFP Lull

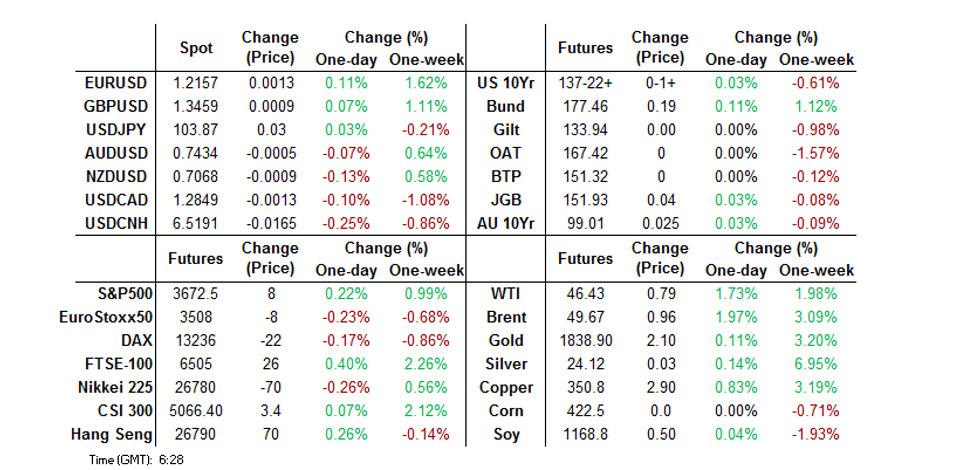

Light macro-headline flow and the traditional pre-NFP Asia-Pac lull has made for limited U.S. Tsy trading, with a 0-03 range for T-Notes overnight, last dealing +0-02 at 137-23, while cash Tsys are little changed along the curve. Sino-U.S. tension, the fiscal situation in DC and the tail end of President Trump's days in office continue to dominate on the headline front, in addition to COVID matters.

- The JGB curve saw some twist steepening, with an acceleration of super-long paper cheapening into the close. Futures held a narrow range, closing +3 on the day. The latest round of BoJ Rinban ops saw the Bank leave the size of its 5-25 Year JGB purchases unchanged, with offer/cover ratios as follows: 5-10 Year 2.51x (prev. 2.44x), 10-25 Year 2.75x (prev. 4.17x). Elsewhere, Tokyo Governor Koike pleaded for people to refrain from unnecessary journeys out of the house. Broader focus continues to fall on the local fiscal dynamic, with the potential for further clarity surrounding the matter during the coming week.

- The Aussie bond curve flattened on Friday, although it has been a fairly lacklustre end to week for the space. A slim weekly issuance slate from the AOFM, with the final week of 2020 issuance set to see only one round of conventional ACGB supply, would have provided some light support. Aussie 10s managed to chip away at their latest leg of underperformance vs. their U.S. equivalent as we moved through the day. YM unchanged, XM +2.5 at the close. Swaps were generally wider vs. ACGBS across the curve. Local retail sales data had little in the way of impact on the space, while the latest round of ACGB Nov '25 supply was better received than the '31 offering seen earlier this week (likely owing to a much more digestible DV01). The average yield of the auction stopped through prevailing mids by ~0.5bp (per BBG pricing), with the cover ratio slipping at the margin but still operating near the 6.00x area.

FOREX: US Dollar Holds Near Lows Ahead Of Key Data, Brexit Developments Eyed

A quiet Asia-Pac session to end the week, to trot out a well-worn phrase. Markets await key US NFP data and touted Brexit breakthroughs or collapse, the anticipatory nature of the session accounting for narrow ranges seen.

- DXY has come off its lows hit early on in the Asia-Pac session, regaining a very limited amount of poise. DXY last at 90.697, just above lows of 90.50 at the end of the European session. Implied volatility in the US dollar has risen to 7.34, the highest since early November.

- In a CNN interview US President elect Biden said the proposed $900bn package is a good start and expects it to be passed. There was some vague market chatter earlier, which concurs with previous rumours, that US Senate leader McConnell heartened by the Democrats supporting a smaller fiscal package.

- AUD and NZD were initially supported by a confluence of factors are supporting including a rise in crude oil and iron prices, and increase in the Fonterra milk price forecast. However AUD and NZD crosses gave back gains as the session wore on despite further increase in oil. It is worth noting that the pull backs in both were very modest and come from multi-year highs.

- GBP/USD was quiet despite reports that UK PM Johnson will be speaking with his French counterpart Macron over the weekend on Brexit. Macron has taken a hard line and reiterated his intention to protect French fishermen which has proved a sticking point.

- EUR/USD barely moved through the session. There are some headwinds for the euro after its relentless ascent; Poland and Hungary are expected to veto the approval of the European Recovery Fund at the European Council Summit on 10‑11 December which could derail the EU's recovery from the pandemic by aid for struggling economies.

- USD/CAD moved in a narrow range, but markets the US DOJ is reportedly discussing a deal with Huawei's Meng Wanzhou that would allow her to return home to China from Canada if she admits wrongdoing. A resolution could be positive for CAD as it eases tension between China and Canada.

- TWD and KRW were the big winners in Asia, the won is now set for the fifth straight week of gains against the US dollar and has gained almost 7% in Q4. TWD hit its highest level against the US dollar in 23-years.

FOREX OPTIONS: Expiries for Dec4 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900(E825mln), $1.2000(E2.1bln, E1.78bln of EUR calls), $1.2250(E928mln-EUR calls)

- USD/JPY: Y102.00($718mln), Y103.00($871mln), Y104.00-20($646mln-USD puts), Y105.00($864mln), Y105.50-55($750mln)

- EUR/GBP: Gbp0.8900(E587mln), Gbp.0.9000-05(E500mln)

- USD/CAD: C$1.2900($540mln-USD puts), C$1.3000($743mln, $643mln USD puts)

- USD/CNY: Cny6.60($917mln)

EQUITIES: Little Changed Ahead Of NFPs

Another marginally mixed session for the Asia-Pac equity space as the week draws to an end, with little in the way of macro headline flow leaving focus on the familiar risk drivers, namely the global COVID situation and fiscal matters in DC. Regional markets generally lacked any meaningful direction heading into the monthly U.S. NFP release.

- Nikkei 225 -0.2%, Hang Seng +0.2%, CSI 300 unch., ASX 200 +0.3%.

- S&P 500 futures +8, DJIA futures +61, NASDAQ futures +45.

GOLD: Familiar Drivers At The Fore

Spot last deals around unchanged levels at ~$1,840/oz after running out of steam ahead of resistance in the form of the Sep 28 low at $1,848.8/oz on Thursday, with the pullback from best levels coinciding with the DXY's move away from lows of the day (which also represented fresh cycle lows), although the dip in U.S. real yields provided some cushion.

OIL: A Deal Was Done

WTI and Brent continued to benefit from the OPEC+ group of producers reaching a short-term production agreement on Thursday. The major crude benchmarks currently sit $0.85 & $1.05 above their respective settlement levels, after registering fresh multi-month highs.

- As a reminder, the OPEC+ group of producers was ultimately unable to flesh out a long-term production plan. As a result, the group agreed to lift cumulative output by 500K bpd during the month of January and will conduct monthly meetings to decide on output levels (which could provide flash points in the coming months).

- Participating Energy Ministers noted that each monthly adjustment will not exceed 500K b/d in either direction (meaning that supply can still be removed from the market), with the arrangement set to remain in place until the cumulative production rise reaches 2mn bpd vs. current levels.

- The facilitates that account for previous undercompliance re: the deal were extended through March.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.