Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

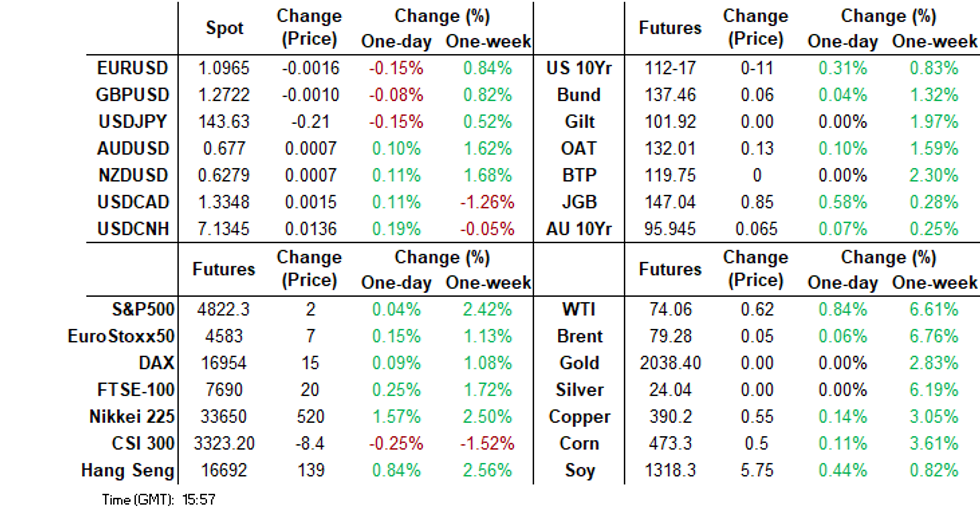

- The bias in US Tsy futures has been higher today, although we remain sub recent highs. Chicago Fed President Goolsbee noted this morning that the market may be getting ahead of itself when it comes to pricing in rate cuts. JGB futures have remained on the front foot, while the 10yr JGB yield has fallen sub its 200-day MA, as fall out from yesterday's dovish BOJ hold continued.

- USD trends were steady against the majors, yen slightly firmer, despite the onshore yield fall. USD/Asia pairs were mostly lower, although CNH was a notable laggard. Fresh cyclical lows in China equities not aiding sentiment. As expected, the 5yr and 1yr LPRs were held steady in China.

- Looking ahead, CPI data from the UK provides the highlight in Europe today, further out we have Nov Home Sales and Consumer Confidence. We also have Fedspeak from Atlanta Fed President Bostic and Chicago Fed President Goolsbee due.

MARKETS

US TSYS: Marginally Richer, Narrow Ranges In Asia

TYH4 deals at 112-16, +0-02, a range of 0-05 has been observed on volume of ~44k.

- Cash tsys sit ~2bps richer across the major benchmarks.

- Tsys have firmed in Asia today operating in narrow ranges for the most part. The space trimmed its losses seen in yesterday's NY session, participants perhaps used the opportunity to close short positions/add fresh longs.

- Chicago Fed President Goolsbee noted this morning that the market may be getting ahead of itself when it comes to rate cuts, adding that such easing will only be justified if inflation continues to cool toward the central bank’s target (BBG).

- CPI data from the UK provides the highlight in Europe today, further out we have Nov Home Sales and Consumer Confidence. We also have Fedspeak from Atlanta Fed President Bostic and Chicago Fed President Goolsbee due.

FED: Goolsbee - Mkt Got A Little Ahead of Itself On Cuts

Chicago Fed President Goolsbee has stated in a Fox News interview that the market got a little ahead of itself in terms of pricing in rate cuts. He added the Fed should not be bullied by what the market wants.

- Goolsbee added that if inflation keeps coming down then the Fed can determine how restrictive it is.

- The Fed President also added that he didn't disagree with anything Fed Chair Powell stated at last week's post-meeting press conference (BBG).

- The market reaction has been negligible to the comments. US Tsy Futures sits a touch higher, last at 112-14 for TYH4. The USD is relatively steady.

JGBS: Futures Pushing Higher, 10yr Yield Sub 200-day MA

JGB futures sit sub session highs, but have maintained a positive bias through the session. We were last 146.93, +.74 for JBH4. Highs came in at 147.10, while earlier dips sub 146.80 drew support. Volumes have been over 34.5k.

- Some mild support has been evident from firmer US Tsy futures, with TYH4 last at 112-16+, +02.

- The 10yr cash JGB yield sits near 0.56% in latest dealings, sub its simple 200-day MA (0.574%). We are down 7bps for the session in yield terms. We are off by a similar amount in yield terms for the 7yr, and 20-40yr tenors.

- 10yr swap rates sit near 0.77%, off by around 2.5bps.

- The data calendar had Nov trade figures and condominium sales, which haven't shifted sentiment.

- Tomorrow, we have weekly offshore investment flows, but the main focus will be on Friday's Nov National CPI print.

AUSSIE BONDS: Richer On Wednesday

ACGB's have ticked higher on Wednesday, improving risk sentiment and a post-BOJ bid in JGBs which spilled over to the wider space have added support.

- Futures are marginally firmer however XM and YM remain well within recent ranges.

- November Westpac Leading Index printed at 0.07%, the prior read was -0.03%.

- Domestic newsflow was limited today with no news of note crossing.

- The next data of note is Friday's November Private Sector Credit, a reminder that there are no RBA speakers scheduled for this week.

NZGBs: Curve Flattens On Wednesday

NZGBs have finished dealing 1bp cheaper to 5bps richer across the major benchmarks, the curve has twist flattened pivoting on 5s.

- An uptick in US Tsys has provided a level of support to the belly and long end of the curve today.

- Rising Oil prices and an uptick in ANZ Consumer Confidence perhaps weighed on the short end which underperformed today.

- The New Zealand Government pledged to cut spending and return the budget to surplus in 2024 despite a slowdown in economic growth, in its half-year economic and fiscal outlook.

- A reminder that the local docket is empty for the remainder of the week.

FOREX: Muted Asian Session Across G-10

It has been a muted Asian session across G-10 FX on Wednesday, ranges have been narrow for the most part with little follow through on moves. Cross asset wise; US Tsy Yields are a touch lower as is BBDXY.

- The Yen has continued to trim some of yesterday's post BOJ losses however USD/JPY remains well within recent ranges. The pair sits ~0.2% lower today last printing at ¥143.50/55 as the downtick in US Tsy Yields adds a level of support for the Yen. Resistance is at ¥145.26 76.4% retracement of the Dec 11 - 14 sell-off. Support comes in at ¥142.25 Dec 19 low.

- AUD/USD is ~0.1% firmer and is testing Tuesday's session highs. The uptrend in AUDUSD remains intact, bulls target break of resistance at the $0.6800 handle and $0.6821, the Jul 27 high.

- Kiwi is also a touch firmer, NZD/USD has broken Tuesday's high and has continued to tick higher albeit in a narrow range. Bulls focus on the $0.63 handle.

- There are no other moves of note in the space.

- UK CPI provides the highlight of today's European session.

EQUITIES: Asia Pac Markets Higher, But China Underperforms

Asia Pac markets are tracking higher following a positive lead from US/EU markets in Tuesday trade. The main exception is China bourses, which are weaker into lunchtime break. US futures are modestly higher in the first part of Wednesday trade, but overall moves have been modest. Eminis sit near 4822, while Nasdaq futures are near 17037.

- At break, the CSI 300 is off just over 0.5%, putting the index (3316.5) close to recent cyclical lows. We saw LPRs held steady as expected, while developer China South City avoided a dollar bond default (SCMP).

- Still, flows into an ETF which tracks EM stocks (ex China) has surged in recent months (see this BBG link). Investors may still be reluctant to move into China markets given growth and policy stimulus uncertainties.

- Hong Kong markets have performed better. The HSI is up 1% at the break. A leadership restructure at Alibaba has improved sentiment in the company and aided broader sentiment.

- Japan markets are in positive territory, but away from best levels. Toyota has trimmed gains after it suspended shipments from subsidiary Daihatsu, after safety testing issues (see this BBG link).

- The Kospi has broken higher, up nearly 1.7%, buoyed by generally positive tech sentiment/soft landing optimism. The Taiex is lagging up 0.30% at this stage.

- In SEA, markets are tracking higher, but gains are under 1%.

OIL: Largely Holding Week To Date Gains

Brent crude has drifted a touch lower in the first part of Wednesday trade, but overall ranges have been tight. We last sat near $79.10/bbl, a touch below recent highs ($79.65-70/bbl). This follows cumulative gains of nearly 3.50% through Mon-Tues trade this week. WTI was last near $73.45/bbl, having followed a similar trajectory to Brent for the session.

- Reuters headlines crossed earlier, stating that US crude oil and fuel inventories reportedly rose last week according to sources. This comes ahead of the EIA data later today in the US.

- It would also fit with various time spreads, which continue to show a reasonable supply backdrop for Brent and WTI into the first part of 2024.

- The Red Sea situation remains the other focus point. The US and allies are reportedly considering military strikes on Houthi militants based in Yemen. The Houthis warned the US they will be legitimate targets if they interfere in its ongoing operations against Israel-linked vessels.

- A new OPEC+ meeting is possible in the near future for the group to discuss the market situation but currently there is no need for new decisions, Russia Dep. PM Novak said, cited by Interfax.

GOLD: Holding Close To Recent Highs

Gold has largely tracked sideways through the first part of Wednesday trade. We last sat near $2040.5, little changed versus end Tuesday levels. We did see a brief dip to sub $2037, but this was supported. Early gains above $2041 also couldn't be sustained.

- A fairly contained session for gold matches with other macro variables. The BBDXY USD index is steady near 1223, while US Tsy Futures have shown a modestly firmer bias. US equity futures sit a touch higher.

- The broader technical backdrop for gold still looks positive. Recent resistance has been evident on moves into the $2045-2050 range. A break above this level could see $2054 targeted, which is a 50% retracement of the earlier Dec pull back.

Indonesia: MNI Bank Indonesia Preview - Dec 2023: On Hold, Watching The Fed

- Bank Indonesia is widely expected to leave rates at 6% at its December 21 meeting. This would be the second consecutive hold since it hiked in October to aid its other FX stability tools. Inflation is within both the 2023 and 2024 bands of 3.0%±1% and 2.5%±1% respectively.

- While the IDR has stabilised since the end of November, it likely has further to go for BI to be comfortable. Indeed, further appreciation is likely needed though for the central bank to feel that it can consider shifting to an easing bias and that will probably require the Fed to move in that direction first and not just signal it.

- Full preview here:

ASIA FX: CNH Lags Firmer Asian FX Backdrop

Most USD/Asia pairs are lower amid a supportive regional equity backdrop. CNH is an exception, undermined by a weaker local equity tone. IDR has also been steady to slightly weaker. Still to come today is Taiwan export orders for Nov. Tomorrow, we have South Korea PPI and the first 20-days export data for Dec. The BI decision in Indonesia is also due, but no change is expected.

- USD/CNH has risen modestly, last near 7.1350 (+0.20%), slightly sub session highs. We started the session close top 7.1200. The Yuan has underperformed most other Asian currencies. A weaker equity tone to the CSI 300 hasn't helped, with the index close to recent cyclical lows. China equity underperformance compared to the improved global trend has been more prominent in recent months. As expected, the 1yr and 5yr LPRs were held steady.

- 1 month USD/KRW saw a subdued start in early trade but has seen greater downside as the session progressed. We last tracked near 1296.5, against earlier highs were close to 1301. Onshore equities have risen just over 1.6% amid broadly positive risk appetite. Offshore investors have added 300mn to local shares. Slightly lower USD/JPY levels have helped at the margin.

- Rupee has sits at 83.14/15, in line with yesterday’s closing levels marking a muted start to Wednesday’s trade. Monday marked the seventh straight day of inflows into Indian Equities as foreign investors bought a net of $215.2mn. A reminder that the data docket is light this week.

- The Ringgit has firmed in early dealing today trimming some of its recent losses. USD/MYR remains well within the 4.63/70 range which has persisted for the most part since early November. We last print at 4.6530/80, ~0.5% below yesterday's closing levels. Looking ahead the local data docket is empty until Friday when November CPI is due. A downtick in CPI to 1.7% Y/Y from 1.8% Y/Y is expected.

- The SGD NEER (per Goldman Sachs estimates) is steady this morning, we remain well within recent ranges. The measure sits ~0.4% below the top of the band. USD/SGD continues to see-saw around the $1.33 handle as broader greenback trends dominate flows. A downtick in the USD yesterday saw the pair retreat below the handle and we sit ~0.1% lower this morning at $1.3270/75. A reminder that the data docket is empty for the remainder of the week.

- USD/PHP has tracked lower, last in the 55.75/80, and away from recent highs above 56.00. Oil prices may be a headwind in the near term, but we have seen steadier Brent levels so far today. BSP Governor Remolona stated the BSP was unlikely to cut rates in the near term. The CB remains wary of supply side shocks.

- USD/IDR has drifted a little higher, last at 15515. This comes despite modest US Tsy futures gains, although Tuesday US trade saw US real yields steadying. Tomorrow the BI decision is due, with no change expected.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/12/2023 | 0700/0800 | ** |  | DE | PPI |

| 20/12/2023 | 0700/0800 | * | | DE | GFK Consumer Climate |

| 20/12/2023 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 20/12/2023 | 0700/0700 | *** | | UK | Producer Prices |

| 20/12/2023 | 0700/1500 | ** |  | CN | MNI China Liquidity Index (CLI) |

| 20/12/2023 | 0900/1000 | ** |  | EU | EZ Current Account |

| 20/12/2023 | 1000/1100 | ** | | EU | Construction Production |

| 20/12/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 20/12/2023 | 1330/0830 | * | | US | Current Account Balance |

| 20/12/2023 | 1400/1500 | | EU | ECB Lane Speech On Euro Area Outlook | |

| 20/12/2023 | 1500/1000 | *** | | US | NAR existing home sales |

| 20/12/2023 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 20/12/2023 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 20/12/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 20/12/2023 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 20/12/2023 | 1830/1330 |  | CA | BOC minutes from last rate meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.