Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Japan markets returned today for the first trading day of 2024. Yen has remained on the backfoot, with dips in USD/JPY supported and the pair tracking through Wednesday highs. It has been a subdued start for JGBs, with futures stronger, +11 compared to settlement levels on Friday. More broadly, the USD and US yields hold sub recent highs.

- Elsewhere, China equity market weakness has been notable, despite better local data. Fallout for CNH has been limited though.

- Looking ahead, markets receive a host of Eurozone inflation prints for December. US ADP employment and jobless claims are notable releases in the US, although the focus will quickly turn to non-farm payrolls on Friday.

MARKETS

US TSYS: Cash Bonds Dealing Little Changed

TYH4 is trading at 112-13, -0-03+ from NY closing levels.

- Cash US tsys are dealing little changed in today's Asia-Pac session, with local participants digest yesterday’s release of the December FOMC Minutes.

- There has been little by way of meaningful newsflow today, other than better than better-than-expected China Caixin PMI services.

- The market’s focus now turns to ADP private employment later today, followed by December employment data on Friday.

JGBS: Subdued Open To The New Year, US ADP Data Due Later Today

In Tokyo afternoon dealings on the first local session of the year, JGB futures are stronger, +11 compared to settlement levels on Friday.

- The session has been data-light, with Jibun Bank Japan PMI Mfg (F) as the sole release.

- ICYMI, BoJ Governor Ueda said that he hopes wages and inflation will rise in a balanced manner this year. He added that the BOJ will be fully prepared to support the financial system after the earthquake in northwestern Japan earlier this week. (See Bloomberg link)

- Cash US tsys are dealing flat to 2bps cheaper in today's Asia-Pac session as participants digest yesterday’s December FOMC Minutes, ahead of the release of US ADP private employment later today and December employment data on Friday.

- Cash JGBs are dealing mixed, with yields 0.1bp lower to 2.4bps higher. The benchmark 10-year yield is 0.7bp higher at 0.621% versus the Nov-Dec rally low of 0.555%.

- Swaps are little changed across maturities, with swap spreads narrower.

- Tomorrow, the local calendar sees Monetary Base, Jibun Bank PMI Composite & Services and Consumer Confidence data.

AUSSIE BONDS: Slightly Richer, Narrow Ranges, US ADP Data Due Later Today

ACGBs (YM +1.0 & XM +1.0) are slightly richer, after dealing in relatively narrow ranges in today’s Sydney session. With the domestic data calendar light apart from the previously outlined Judo Bank Services & Composite PMI data, local participants appear to have sat on the sidelines ahead of the release of US ADP private employment later today and December employment data on Friday.

- Cash US tsys are dealing little changed in today's Asia-Pac session as participants digest yesterday’s release of the December FOMC Minutes.

- (AFR) A multi-month surge in iron ore prices is poised to deliver Treasurer Jim Chalmers as much as $18 billion in extra tax revenue. (See link)

- Cash ACGBs are 2bps richer, with the AU-US 10-year yield differential 3bps tighter at +10bps.

- Swap rates are little changed, with EFPs 2-3bps wider.

- The bills strip is little changed, with pricing flat to -1.

- RBA-dated OIS pricing is little changed, with 56bps of easing priced by end-2024.

- Tomorrow, the local calendar is empty.

AUSTRALIAN DATA: PMI Data Point To Sticky Services Inflation

The final Judo Bank composite PMI for December was revised down 0.5pp to 46.9 from the preliminary read but it is still up on November’s 46.2. Judo Bank notes this is consistent with a “soft landing”. It is signalling that the economy contracted at the end of the year though but at a slightly slower pace. The move was driven by a 0.5pp downward revision to 47.1 for the services sector as new business fell at its fastest pace in over two years. November was 46.

- Input costs for services eased but optimism regarding the outlook over the year ahead resulted in a pickup in selling price inflation. Judo Bank observes that both input and output prices remained “well above their series averages” but December costs rose at the slowest since October 2021.

- The RBA has been concerned about the stickiness of services prices and if the Q4 data due on January 31 shows that it is not moving lower fast enough to bring the aggregate back to target in line with forecasts, then that could be enough to drive a February rate hike.

- Australia’s employment growth has been an area of the economy that defied gravity in recent months and the services PMI is suggesting that it accelerated in December. Employment data is due on January 18.

- The drop in new business was both domestically-driven and from abroad due to elevated costs, higher rates and a weaker economy.

- The Q4 services PMI deteriorated over 2 points from Q3 and is suggesting that quarterly GDP growth may slow further.

- See Judo Bank report here.

Source: MNI - Market News/ABS/Bloomberg

AUSTRALIA: Core Inflation Running Higher Than Other Countries

In the RBA’s December meeting minutes, it noted that underlying inflation is higher in Australia than in several other countries. Given the RBA mentioned this development, it is worth monitoring it, and there may be pressure for them to hike if the gap doesn’t narrow in upcoming data . November CPI prints on January 10 with December/Q4 on January 31, by this time most OECD countries will have released their December data.

- US core has been running below Australia since October 2022 and in October 2023 stood 1pp lower. US December data are released on January 11.

- Euro area underlying inflation has consistently printed below Australia’s and in October was 0.9pp lower. It peaked at 5.7% versus Australia’s 7.2%. Euro area preliminary December CPI is this week on January 5.

- One of the biggest differences is with Canada who recorded underlying inflation of 2.8% in October compared with Australia’s 5.1%. The Bank of Canada has hiked rates 475bp to 5% this cycle compared with the RBA’s 425bp to 4.35%.

- However, Australian core inflation remained below the UK in October at 5.1% versus 5.7% but in November the UK saw it ease substantially to 5.1%.

- NZ and Australia’s core inflation were inline in Q3. There is a high correlation between both countries for both headline and underlying CPI rates. Q4 NZ CPI is released on January 24.

Source: MNI - Market News/ABS/Refinitiv

NZGBS: Twist-Steepening, 10Y Underperformance Vs. $-Bloc

NZGBs have twist-steepened into the close, with yields 1bp lower to 4bps higher. The 5 and 10-year benchmarks closed at session cheaps, despite the lack of newsflow locally.

- On a relative basis, the NZGB 10-year has also underperformed its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials respectively 8bps and 9bps wider.

- Cash US tsys are dealing little changed in today's Asia-Pac session as participants digest yesterday’s release of the December FOMC Minutes. The market’s focus now turns to ADP private employment later today, followed by December employment data on Friday.

- Swap rates closed 3-4bps firmer, with short-end implied swap spreads wider.

- RBNZ dated OIS pricing closed flat for meetings out to July and 3-5bps firmer beyond. 106bps of easing is priced by November.

- Tomorrow, the local calendar is empty.

EQUITIES: Japan Markets Recoup Early Losses, China Equity Weakness Extends

Regional equities are mixed in Thursday trade to date. On the downside China equity losses are a standout, with the CSI 300 down 1.40% at the break. Japan markets, on the first trading day of 2024, have pared losses as the session progressed. US equity futures sit marginally higher at this stage. Eminis were last near 4751, +0.10%, with Nasdaq futures up by a similar amount.

- The CSI 300 is off by 1.4% at the break. Sentiment not buoyed by a much stronger than expected Caixin services PMI result. Aggregate markets continue to unwind the late 2023 rally.

- The real estate sub index is down a further 2.40%, making fresh cyclical lows, with little respite for the under pressure sector. Fitch downgraded the outlook for a number of China national asset management companies on expectations of reduced government support.

- The HSI is off nearly 0.50% at the break.

- Japan markets opened lower, playing catch up to the softer global equity trend since the start of the year, but we are comfortably away from lows. The Topix sits +0.30% higher, the Nikkei 225 down -0.75%. Weaker yen levels are likely helping at the margin, although airline stocks have been pressured in the wake of the recent crash.

- The Kospi continues to correct lower, off a further 0.90%, while the Taiex in Taiwan has seen a more muted fall (off 0.15%).

- In SEA, Philippines stocks have outperformed, up 1%. The bourse will reportedly offer new products to retail investors, while IPOs are expected to rise this year (see this link). Trends are mixed elsewhere.

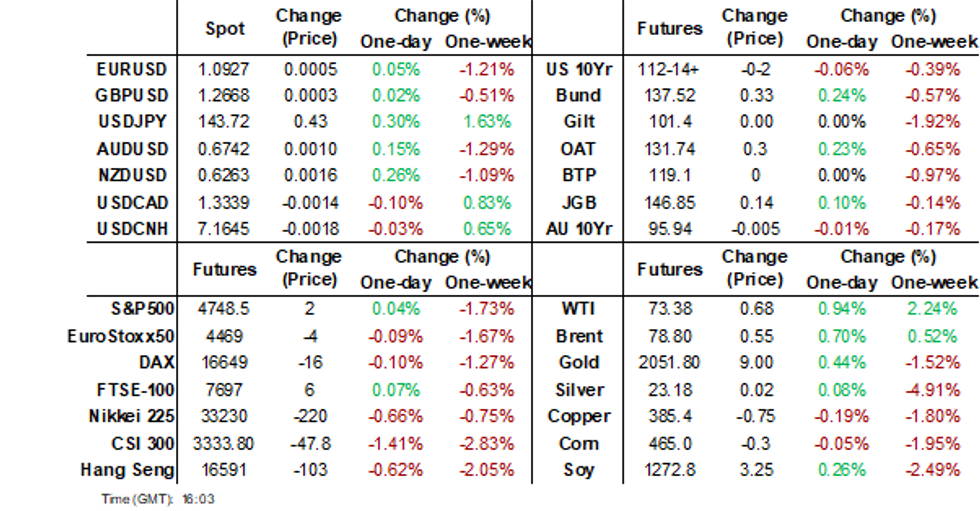

FOREX: Dollar Index Close To Unchanged, Yen Marginally Weaker, NZD Firms

The BBDXY sits slightly lower in latest dealings versus end NY levels from Wednesday. The index was last under 1224, but has maintained tight ranges overall. Yen has underperformed at the margins, most notably against the NZD.

- Early trade saw USD/JPY dip to 142.86, but this was short lived and we climbed back towards 143.50 as the session progressed. We were last near these levels, with Wednesday highs (143.70/75) still intact. There was a modest PMI revision for Dec, while onshore equities have pared losses as the session progressed (in the first trading session for the year).

- BoJ Governor Ueda stated that he hopes wages and inflation rise in a balanced fashion this year. He also stated the financial system will be supported in the wake of the recent earthquake.

- NZD/USD has recovered from earlier lows, the pair last near 0.6265/70, around 0.30% firmer than Wednesday NY closing levels. Recent dips below the 20-day EMA (0.6245) have been supported. Local news flow has remained light.

- AUD/USD sits near 0.6740 slightly above end Wednesday levels.

- Cross asset moves in the US space have been muted, with US bond and equity futures relatively steady.

- Looking ahead, markets receive a host of Eurozone inflation prints for December. US ADP employment and jobless claims are notable releases in the US, although the focus will quickly turn to non-farm payrolls on Friday.

OIL: Ongoing Middle East Tensions May Add War Premium To Crude

Oil prices have held onto the 3.5%-plus gains made on Wednesday during the APAC session today, as the factors driving it higher haven’t dissipated and US data showed a large stock drawdown. WTI is up 0.7% to $73.22/bbl, off the intraday low of $72.90. Brent is 0.5% higher at $78.62. The USD index is flat.

- Crude rose yesterday on OPEC reiterating its commitment to market stability, a terrorist attack in Iran adding to tensions in the region, shutdowns at Libyan oil fields worth 365kbd and the US announcing it will buy 3mn barrels for its SPR while last week there was a large US stock drawdown.

- The US and its allies have warned the Houthis that there will be consequences if they don’t stop attacking ships in the Red Sea. The UN said that 18 companies have now rerouted ships. There is a risk that if the situation deteriorates, a war risk premium will be added to oil prices again, which Goldman Sachs estimates could be $3-4/bbl. It expects Brent to stay in the $70-90/bbl range over 2024, according to Bloomberg.

- Bloomberg reported that US crude stocks fell 7.418mn barrels in the latest week, according to people familiar with the API data. But gasoline inventories rose 6.913mn and distillate 6.686mn. The official EIA data is out later today.

- Later the US December ADP employment and jobless claims print. There are also final S&P Global US/Europe composite/services PMIs for December. There are also preliminary December German and French CPIs.

GOLD: Down For The Fourth Consecutive Day

Gold has registered a slight uptick in the Asia-Pac session, partially recovering from a 0.8% decline that brought it to a closing price of $2041.49 on Wednesday. The strength of the dollar played a pivotal role in Wednesday's decline, marking the fourth consecutive day of diminishing gold values.

- US Treasuries finished little changed on Wednesday. The NY session saw choppy trading after the December FOMC Minutes release. The minutes were balanced but with a dovish tone as officials noted diminished inflation and the need to start a discussion of QT wind down.

- Data released on Wednesday showed the ISM Manufacturing Index remaining in contraction territory for a 14th month at the end of 2023. Job openings eased in November to the lowest level since early 2021.

- The market’s focus now turns to ADP private employment later today, followed by December employment data on Friday.

ASIA: Most Of Asia Doesn’t Have China’s Property Woes

Residential property markets in Asia are mixed with some, such as Singapore, soaring above trend, whereas others are stagnating or declining, and it is not just China. Tighter monetary policy and debt issues have impacted some markets, including Korea. Korean house prices steadied in H2 2023 to be down 4.7% y/y in December but they remain above trend. Housing is not an area of concern for most countries with positive annual growth in prices and some below-trend markets are correcting for a period of above trend house price inflation. Where prices are falling, such as in China, HK and Korea, policy makers have either reacted or are watching developments closely.

North Asian residential property prices y/y%

Source: MNI - Market News/Refinitiv

ASEAN residential property prices y/y%

Source: MNI - Market News/Refinitiv

CHINA DATA: Caixin Services PMI Beats, Diverging Further From The Official Print

The Dec Caixin services PMI comfortably beat expectations, rising to 52.9 (51.6 forecast and 51.5 prior). The follows the better than expected Caixin manufacturing PMI from earlier this week, 50.8 against 50.3 forecast.

- For the Caixin services PMI we are still below earlier 2023 highs (57.8), but the trend improvement was evident through the final stages of 2023.

- In terms of the detail, new business activity was supported by consumer spending (Rtrs), while increased foreign travelers to China was also cited as a positive. The employment sub index rebounded to 50.4 from 49.9 in Nov.

- The early 2024 outlook is positive but remains below its long run average (Rtrs). The prices charged component of the index also fell versus Nov levels.

- The result furthers the divergences with the official PMI readings, which lost ground in Dec, particularly in the manufacturing space.

- Analysts note this likely reflects differences in terms of firms covered within the respective PMI releases, with the Caixin PMI tending to be more focused on smaller businesses and in the export sector.

- The market reaction has been fairly muted, with HK and China equities remaining in the red, while USD/CNH dips remain supported.

ASIA FX: Spot FX Weaker, But NDF Levels Mostly Away From Wednesday Lows

USD/Asia pairs are mostly higher in spot terms, but trends in the NDF space have been more muted relative to Wednesday session trading session highs, as USD gains have been tempered somewhat. USD/CNH has been supported on dips, but is also not seeing headway through Wednesday highs. Tomorrow, we have Thailand and Philippines CPI prints. Taiwan inflation figures are also out. Singapore retails sales is also due.

- USD/CNH was supported sub the 7.1600 level, as the CNY fixing stabilized. We couldn't breach the 7.1700 on the topside though. Local equities are down sharply, the CSI 300 off nearly 1.40%. Fitch downgraded the outlook for some local asset managers. The Caixin services was stronger than expected, but didn't aid sentiment.

- 1 month USD/KRW has been relatively stable, the pair currently holding near the 1307/08 region. Onshore equities have continued to correct lower, off nearly a further 1%, but this hasn't impacted won sentiment negatively.

- Spot USD/IDR has continued to push higher, the pair last near 15530, off around 0.3% versus yesterday's closing levels. The 1 month NDF sits lower though relative to Wednesday highs, tracking at a similar level (15533). For spot we are through all key EMAs, with upside focus likely to rest on the 15600 level. A weaker global equity trend since the start of the year has weighed on the rupiah, with 5yr CDS ticking up to 76bps, against late 2023 lows sub 70bps.

- USD/THB has continued to climb today, back into the 34.55/60 region. This is 0.70% weaker in baht spot terms. A weaker baht tone is in line with the broader recovery in USD sentiment, along with softer gold prices. Local equities sit off recent highs, while offshore investors have had a mixed start in terms of flows since the start of the year. The Dec inflation print is due tomorrow. The market looks for similar trends to the Nov outcome. The next monetary policy meeting isn't until Feb 7.

- PHP has outperformed the firmer USD backdrop. Spot USD/PHP sits relatively steady in the 55.55/60 region. Onshore equities have outperformed, up 1.2%, with more IPOs this year and more retail products set to become available. BSP Governor Remolona has stated the central bank doesn't want to overtighten but knows what it has to do if inflation stays high (RTRS). The Governor also noted the country was moving towards a less managed FX rate (BBG).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/01/2024 | 0630/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 04/01/2024 | 0745/0845 | *** |  | FR | HICP (p) |

| 04/01/2024 | 0900/1000 | *** | | DE | Bavaria CPI |

| 04/01/2024 | 0900/1000 | *** | | DE | Saxony CPI |

| 04/01/2024 | 0930/0930 | ** |  | UK | BOE Lending to Individuals |

| 04/01/2024 | 0930/0930 | ** | | UK | BOE M4 |

| 04/01/2024 | 0930/0930 | | UK | BOE's Monthly Decision Maker Panel data | |

| 04/01/2024 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 04/01/2024 | 1300/1400 | *** | | DE | HICP (p) |

| 04/01/2024 | 1315/0815 | *** |  | US | ADP Employment Report |

| 04/01/2024 | 1330/0830 | *** | | US | Jobless Claims |

| 04/01/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 04/01/2024 | 1600/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 04/01/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 04/01/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.