Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Yen has largely reversed Thursday gains, with early comments from BoJ Governor Ueda, which were more cautious around the inflation goal, weighing on sentiment. In the Tokyo afternoon session, JGB futures are slightly higher, +2 compared to the settlement levels, after relatively subdued dealings.

- Jun'24 10Y US Tsy futures have traded sideways today making highs of 110-15+ and lows of 110-11, and now trade unchanged at 110-14, ranges remain well within Thursday's. NY Fed President John Williams spoke earlier where he said we don't need to tighten monetary policy any further and expects the Fed to cut interest rates later this year.

- China official PMIs were net better than expected. Manufacturing was 49.1, versus 49.0 forecast and 49.2 prior. The services or non-manufacturing PMI was 51.4, well above expectations at 50.7. China and Hong Kong equities sit marginally higher, while CNH has remained steady.

- Looking ahead, Eurozone CPI then takes centre stage before US ISM Manufacturing PMI rounds off the week’s tier-one data.

MARKETS

US TSYS: Treasuries Unchanged, Fed's Williams See No Urgency To Cut Rates

- Jun'24 10Y futures have traded sideways today making highs of 110-15+ and lows of 110-11, and now trade unchanged at 110-14, ranges remain well within Thursdays. Initial resistance holds at 110-26+ (20-day EMA), a break above here will open 110-08 (50-day EMA), while initial support remains at 109-25+ (Low Feb 23) a break here opens a move to 109-14+ (Nov 28 Low)

- Curves are bull flattening yield are currently +0.05bp to -0.5bps across the curve, the 2Y yield +0.5bp higher at 4.625%, 10Y +0.2bp higher at 4.252% while the 2y10y is -0.425 at -37.527

- The NY Fed President John Williams spoke earlier where he said we don't need to tighten monetary policy any further and expects the Fed to cut interest rates later this year. See MNI's coverage of he speech here.• Earlier the Short-term funding bill passed senate and now sits with Biden.

- Looking ahead: S&P Global US Manufacturing PMI, U. of Mich. Sentiment, Construction Spending, ISMs & Fed Speakers

JGBS: Subdued Session, Local Data Not Market Moving Today, Heavy Calendar On Monday

In the Tokyo afternoon session, JGB futures are slightly higher, +2 compared to the settlement levels, after relatively subdued dealings.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined labour market and Jibun Bank PMI Mfg data, and comments from BoJ Governor Ueda.

- (Bloomberg) -- Bank of Japan Governor Kazuo Ueda said the Bank of Japan’s price target is not yet in sight, tempering market speculation that the bank’s first rate hike since 2007 is just around the corner. (See link ICYMI)

- Cash tsys are dealing flat to 1bp richer in today’s Asia-Pac session after Fed Williams said in a Fireside Chat after the US market close that he doesn’t believe the Fed needs to tighten monetary policy further. He added that he expects to cut interest rates later this year.

- Cash JGBs are cheaper out to the 10-year and slightly richer beyond. The 5-year zone is the underperformer on the curve, with its yield 1.6bps higher. The benchmark 10-year yield is 1.1bp higher at 0.720% versus the Nov-Dec rally low of 0.555% and the February high of 0.772%.

- Swaps are slightly richer, with swap spreads mostly tighter.

- On Monday, the local calendar sees Capital Spending, Company Profits and Monetary Base data, along with BoJ Rinban operations covering 1-3-year and 10-25-year+ JGBs.

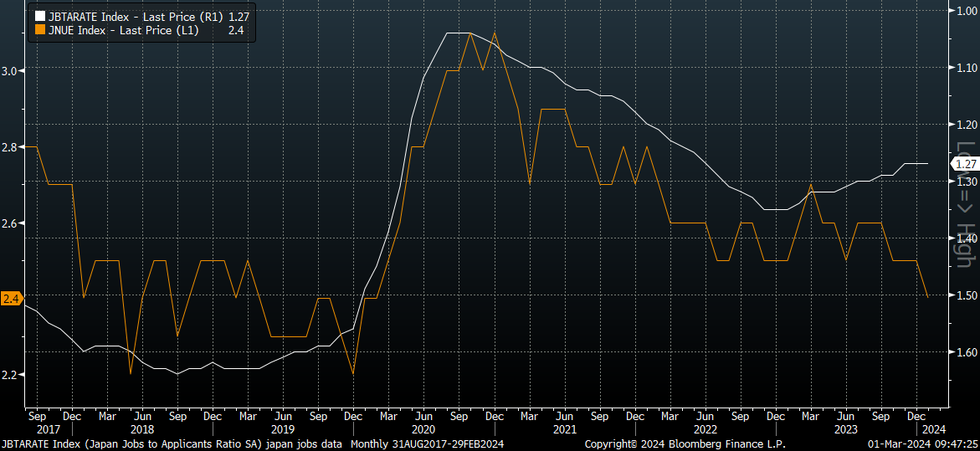

JAPAN DATA: Unemployment Rate Back To Early 2020 Lows, New Job-To-Applicant Ratio Ticks Up

Japan's Jan jobless rate and job-to-applicant ratio were in line with market expectations. The jobless rate printing at 2.4% (which was down from a revised 2.5% in Dec last year). This lows back in the unemployment rate back to early 2020. The job-to-applicant ratio at 1.27 was in line with the prior outcome.

- The participation rate was 62.6%, versus 62.8% in Dec. The number of employed fell by 30k in the month, while those unemployed rose by 130k.

- The chart below overlays the jobless rate and the job-to-applicant ratio (which is inverted on the chart). We are seeing some modest divergence, although the job-to-applicant ratio has stabilized in recent months.

- Also note the new job-to-applicant ratio rose to 2.28 from 2.25 in Dec, the first improvement since August last year.

- Overall, labor market conditions suggest tightness, while BoJ Governor Ueda reiterated the importance of current wage negotiations in driving a sustainable wage/inflation cycle and aiding a consumer spending recovery in H2.

Fig 1: Japan Unemployment Rate & Job To Applicant Ratio (Inverted)

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Little Changed, Light Local Calendar, Heavy Data Calendar On Monday

ACGBs (YM flat & XM +1.0) are slightly richer after dealing in relatively narrow ranges in today’s Sydney session. Today’s data drop (Judo Bank PMI Mfg and CoreLogic House Prices) failed to be market-moving.

- Cash tsys are dealing flat to 1bp richer in today’s Asia-Pac session after Fed Williams said in a Fireside Chat after the US market close that he doesn’t believe the Fed needs to tighten monetary policy further. He added that he expects to cut interest rates later this year.

- Cash ACGBs are flat to 1bp richer, with the AU-US 10-year yield differential 2bps higher at -12bps.

- ACGB May-34 went smoothly with more demand present. The cover ratio moved higher to 3.6437x from 3.1125x at the February auction. The weighted average yield printed 1.28bps through prevailing mids (per Yieldbroker).

- Swap rates are flat to 1-2bps lower.

- The bills strip is little changed.

- RBA-dated OIS pricing is little changed across meetings. A cumulative 37bps of easing is priced by year-end.

- On Monday, the local calendar sees the Melbourne Institute Inflation Gauge, Q4 Inventories, Q4 Company Operating Profits, ANZ-Indeed Job Advertisements and Building Approvals data.

NZGBS: Subdued Session After A Robust Post-RBNZ Rally

NZGBs ended the day flat to 1bp cheaper, reflecting a subdued local session. However, it has been a robust week for NZGBs, as yields closed 10-20bps lower than Tuesday's closing levels following the RBNZ's dovish shift. The 2/10 curve is approximately 10bps steeper than Tuesday's level.

- Moreover, NZGBs have outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials around 5bps tighter than Tuesday's closing levels.

- Swap rates closed 1-3bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 1bp softer across meetings. A cumulative 53bps of easing is priced by year-end from an expected OCR peak of 5.53%.

- Before Wednesday's decision, the market had attached a 29% chance of a 25bp hike at yesterday’s meeting, with an anticipated terminal OCR of 5.65% (reflecting a 61% probability of a 25bp hike) by the May meeting. A cumulative 40bps of easing by year-end had been factored into the pricing.

- It is also worth noting that in late December, the market had expected over 100bps of easing by year-end, stemming from an anticipated terminal OCR of 5.53%.

- Next week, the local calendar sees Terms of Trade data on Monday.

FOREX: Yen Weakens Post Ueda Comments, Modest Risk On Elsewhere

The USD index has tracked tight ranges in the first part of Friday trade, the BBDXY last near 1244, which is close to end levels from NY on Thursday. This has masked some divergent trends within the G10 space though, with a risk on tone amid JPY and CHF underperformance.

- Early doors we had comments from BoJ Governor Ueda (in Brazil for the G20). These were cautious/less hawkish compared to remarks by Board member Takata that were made yesterday. The governor noted the inflation goal is not yet in sight and that current spring wage negotiations were key to ensuring a sustainable wage/inflation outlook.

- USD/JPY didn't react initially, but rose later to 150.40 (after opening around 150.00), this is a 0.30% yen loss and puts us back close to levels that prevailed before Takata headlines crossed yesterday.

- A turnaround in US equity futures, which now sit +0.10-0.20% higher has likely weighed on the yen as well. US yields are close to flat at this stage. Comments from the Fed's Williams haven't impacted sentiment greatly.

- AUD/USD sits back near 0.6510, close to 0.20% higher. The firmer equity backdrop has helped, while iron ore prices sit back above earlier lows in the week. (last near $117.2/ton). The AUD/NZD cross has been unable to re-take the 1.0700 handle.

- For NZD/USD, we are off the lows from earlier this morning, trading again in very tight ranges of 20pips (last 0.6090/95. Earlier RBNZ Gov Orr gave a speech in Christchurch, largely reiterating what was mentioned earlier this week at the RBNZ OCR meeting.

- CHF was a weaker performer through Thursday trade, and it has lagged softer USD trends elsewhere. EUR/CHF tested above it 200-day MA for the first since June, but has seen little follow through. The pair was last near 0.9565.

- Looking ahead, Eurozone CPI then takes centre stage before US ISM Manufacturing PMI rounds off the week’s tier-one data.

ASIA EQUITIES: Hong Kong Equities Reverse Earlier Losses, China Equities Steady

Hong Kong and China equities are mostly higher today, Hong Kong equities had lagged the move, however, are now out-performing China mainland equities. HK markets pushed higher after an official report showed a slump in manufacturing in China persisted last month, it heightened bets on stronger economic stimulus measures as policymakers gather next week to set economic targets.- Hong Kong equities are mostly higher and out-performing today after initially opening down 0.5-2% lower. Property is the worst performing sector, opening down 1.30% before paring losses however heading into the break sold off again to be down 0.85%. HSTech is the best performer up 1.60%, while the HSI is up 0.75%

- China mainland equities have been less volatile today, with the CSI1000 trading flat, while the CSI300 is up 0.30%.

- China Northbound flows were +16.6b yuan on Wednesday, highest since July 2023, with the 5-day average now 5.75b, while the 20-day is at 3.66b yuan.

- China’s home sales slump dragged on in February, even as regulators stepped up efforts to salvage the beleaguered property market, with the value of new home sales sliding 60% from a year earlier.

- It was reported on Thursday that the US will be investigating security risks associated with Chinese Electric Vehicles and other internet-connected cars. It should be noted that Chinese auto companies have a 27.5% tariff imposed on them, so penetration in the US market is limited; however, this would further dampen hopes of growth in the region.

- Earlier, China's February Non-Manufacturing PMI was 51.4 vs 50.7 est, while February Manufacturing PMI was 49.1 vs 49.0 est.

- Looking ahead, Hong Kong Retail Sales at 4:30 pm local time.

ASIA PAC EQUITIES: Asian Equities Push Higher, As Tech Names Out-Perform

Regional Asian Equities have mostly followed US stocks higher today after strong month-end flows and US inflation data put investors at ease. Japan is the best performer in the region, while South Korea is out for Independence day

- Japan equities are higher today, following wider markets after the US index closed at records highs as Tech names led the move. The BoJ Governor Kazuo Ueda was out earlier saying that price goals are not yet in sight, while he will be closely watching wage data. In local markets Tokyo Electron contributed the most to the index up 1.5%, with the Topix up 1.18%, while the Nikkei 225 trades up 1.95% led by tech names.

- South Korean markets are closed today for Independence Day

- Taiwan Equities are slightly lower today, Taiex Down 0.10%, after initially trading up 0.20%. TSMC is the biggest contributor to the market after the Philadelphia Stock Exchange Semiconductor Index pushed 2.70% higher on Thursday. Foreign equity flows are slowing with just $3.1 flowing into the market on Thursday.

- Australian equities have followed US equities higher and officially enter a bull market after rallying 20% off the June 2022 lows. Strong corporate earnings have helped push the market higher with Life 360 the standout today, up 36% on expansion plans. The ASX200 closed 0.53% higher.

- Indian Equities have surged higher today and the most in almost a month after data showed the economy grew at a faster pace than expected in the last quarter, the Nifty 50 is 1% higher today.

- Elsewhere in SEA, NZ equities have reversed earlier losses to trade unchanged, while Indonesian equities continue to see outflows with another $40.75m, with equities down 0.60%.

ASIA EQUITY FLOWS: Asia Equity Markets See Outflows As Foreign Investors Take Profit

- China equities saw their largest northbound inflow since July 2023, as markets surged higher with the CSI300 up 1.91%, in signs that policy support may be changing market sentiment. It had been reported that China was banning some Quant strategies and that they had banned a top performing quant manager from trading for a year. Flows are gaining momentum with 16.6b yuan of inflows yesterday with the 5-day average now 5.75b, while the 20-day average is 3.66b.

- South Korean equities were lower on Thursday, largely due to moves lower in the US and tech names globally after such a stellar run of late. Flows remain positive although momentum is slowing with $184m of inflows, while the 5-day average sits at $160m, while 20-day is at $306m.

- Taiwan equities were back from their break yesterday, trading 0.60% higher led higher by hardware names. While GDP was lower at 4.93% vs 5.10% expected, however projects the economy will rebound quickly as global demand for AI related technologies spur growth higher. Just 3.1m flowed into Taiwan equities on Thursday, with the 5-day average now $226m vs the 20-day average at $250m

- Indonesian again saw outflows marking the 4th of 5 day of negative flow, BI Deputy Gov said they wont be cutting rates yet due to high global uncertainty and rupiah volatility. The 5-day average is -$47m, while the 20-day is at $38m.

- Thailand saw their largest outflow since Jan 17th of $21m of -$120m, while markets were 0.80% lower. Current account Balance swung to a deficit on high gold imports, while factory output contracts fell for a 16th straight month. The 5-day average is now -$24m, while the 20-day is at $4.1m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 16.6 | 28.8 | 46.2 |

| South Korea (USDmn) | 184 | 800 | 8373 |

| Taiwan (USDmn) | 3 | 1134 | 4805 |

| India (USDmn)** | -167 | 214 | -3164 |

| Indonesia (USDmn) | -41 | -236 | 1180 |

| Thailand (USDmn) | -121 | -123 | -788 |

| Malaysia (USDmn) ** | -56 | 21 | 456 |

| Philippines (USDmn) | 8 | 11.4 | 208 |

| Total (Ex China USDmn) | -190 | 1822 | 11071 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Feb 28 |

OIL: Within Recent Ranges, But Up For The Week

The first part of the Friday session has seen oil benchmarks firm modestly. The active Brent contract (K4) was last near $82.20/bbl, up around 0.35% for the session so far. We are tracking around 1.7% higher for the week at this stage. The active WTI contract is near $78.50/bbl, up around 2.6% for the week so far.

- News flow around oil has been light so far today. BBG noted that major China buyers ramped up derivative related activity, which helps price benchmarks (see this link). Broader risk appetite has been firmer in the equity space, which has likely helped oil at the margin.

- Earlier we had China PMI data, which was slightly better than expected, although the manufacturing index remain comfortably in contraction territory. There are some signs that we may a better next month.

- Elsewhere, US President Biden when asked on the prospect of an Israel-Hamas ceasefire agreement says that 'hope springs eternal,' but that it is unlikely to start by Monday 4 March (previously raised by Biden as a target date).

- Wires also carried comments from the leader of the Houthi forces in Yemen, claiming that the group will introduce military "surprises" in their Red Sea operations, which their "enemies" will not expect.

- For Brent, we remain within recent ranges. Late Jan highs at $83.65/bbl remains the upside focus, while recent lows rest near $80/bbl.

GOLD: Pushes To A Three-Week High After PCE Deflator Data

Gold is slightly higher in the Asia-Pac session, after closing 0.5% higher at $2044.30 on Thursday.

- Bullion rose to a three-week high after inflation figures matched expectations and reinforced bets that the Federal Reserve won’t need to raise interest rates again.

- US Treasuries finished the NY session 1-2bps richer. The US 10-year yield finished 1bp lower at 4.26% after pushing as high as 4.32% ahead of the PCE deflator data.

- The US PCE deflator, which is the Fed’s preferred inflation gauge, printed in line with market expectations, with the core measure up 0.4% m/m and 2.8% y/y. This confirmed the jump in inflation in January, as foreshadowed by prior CPI and PPI data.

- Fed speak remained balanced while leaning toward cut(s) in 2H'24. Fed Bostic reiterated that the central bank is likely going to be in a position to begin easing interest rates sometime in the summer.

- According to MNI’s technical team, Thursday’s high of $2050.72 cleared resistance at $2041.1 (Feb 23 high) and opened the key level of $2065.5 (Feb 1 high).

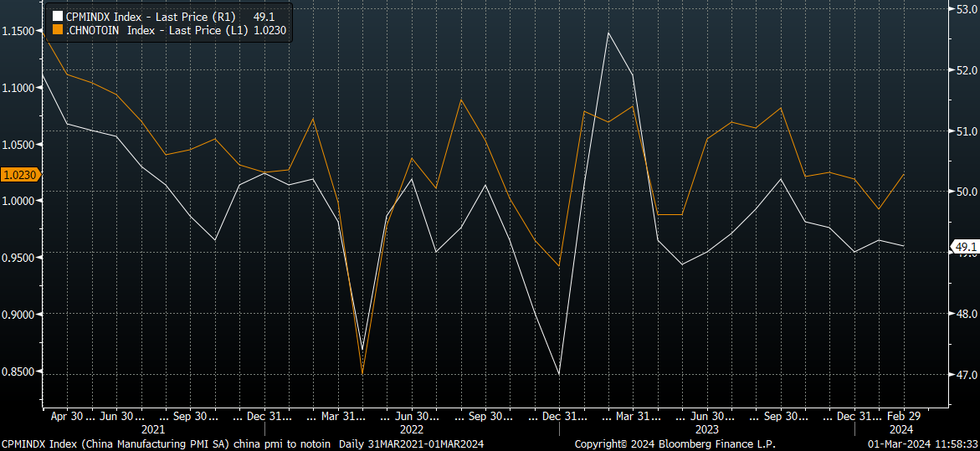

CHINA DATA: PMIs Print Firmer Than Expected, But Details Mixed

China official PMIs were net better than expected. Manufacturing was 49.1, versus 49.0 forecast and 49.2 prior. The services or non-manufacturing PMI was 51.4, well above expectations at 50.7, (which was also the prior outcome).

- Some of the detail was soft though for the manufacturing PMI, output fell to 49.8 from 51.3. New orders were steady at 49.0. Employment eased to 47.5 from 47.6. New export orders fell to 46.3 from 47.2.

- On the prices front we are at 50.1 from 50.4 in Jan for input prices. Output prices rose though to 48.1 from 47.0. The softer conditions were most evident for small enterprises (46.4 versus 47.2 prior).

- Still, the new order to inventory ratio for the manufacturing PMI rose slightly, see the chart below of this ratio against the headline PMI. This suggests at the margin some improvement in the headline result going forward.

- On the non-manufacturing side, new orders fell to 46.8, while business activity expectations eased to 57.7 from 59.7. New export orders rose though to 47.3 from 45.2, while employment was steady at 47. On the prices front, input prices rose, but selling prices eased a touch.

- The Caixin manufacturing PMI also printed slightly firmer than expected for Feb, 50.9, versus 50.7 forecast.

- A reminder that with the LNY timing may have impacted readings as well. Focus will shift the outcomes of the China NPC in the early parts of this month.

Fig 1: China Manufacturing PMI Versus New Order To Inventory Ratio

Source: MNI - Market News/Bloomberg

SOUTH KOREA DATA: Export Growth Slows, But Detail Solid, Chip Export Recovery Continues

South Korea Feb trade figures were stronger than expected from an export growth standpoint, up 4.8%y/y versus 1.4% forecast. This was a down step from Jan's heady 18% pace, but the timing of the LNY this year compared to last year was a factor. Imports fell by -13.1%, compared with a -11.7% forecast. This saw the trade surplus rise to just under $4.3bn, versus $2bn forecast and $0.328bn in Jan.

- Adjusted for working day differences were up 12.5% in y/y terms, still indicating a healthy trend. The equivalent print for Jan was 5.7% for this metric. The chart below overlays this y/y measure against y/y changes in KRW/USD.

- The won looks a little too low from a momentum standpoint, but other factors are also at play, with Fed expectations and strong domestic outflows by local investors to overseas equities won negatives.

- In terms of the detail, chip exports surged 67%, with base effects helping, but this segment has turned the corner. Exports to the US were up 9% y/y, but fell 2.4% to China with the LNY likely impacting. Exports of cars fell 7.8%.

- The trade surplus is just short of recent highs and the trend has moved comfortably back into positive territory, in line with an improved terms of trade backdrop. Still, given some of the headwinds outlined above, this hasn't been as positive for KRW than otherwise might have been the case.

Fig 1: Daily Average South Korea Exports Y/Y & KRW Y/Y

Source: MNI - Market News/Bloomberg

ASIA FX: MYR Top Performer In The Past Week, As Official Concerns Around FX Weakness Rises

Most USD/Asia pairs are lower, aided by an equity risk on tone, although moves have been modest overall. USD/CNH has remained steady, while South Korean markets have been out for Independence Day. IDR and PHP have rallied somewhat, while THB has lagged. USD/MYR tested below the 50-day EMA earlier before stabilizing (the ringgit is the top performer in the past week). Looking ahead to next week we have South Korean IP and the PMI print as the main focus on Monday. Later next week we have the BNM decision in Malaysia.

- USD/CNH has drifted a little higher in the first part of Friday trade, last near 7.2100. USD/CNY spot has also rebounded, back to 7.1970. Overall vols have remained low though. We had the official PMI prints for Feb, along with the Caixin manufacturing PMI. All printed better than expected, particularly the services official read. There was no meaningful CNH reaction though. Onshore equities have struggled for positive traction today.

- With onshore markets out, the 1 month USD/KRW NDF has been very steady, last near 1333. South Korean export data was stronger than expected, as was the trade surplus. The export recovery should support the growth backdrop in the near term.

- USD/IDR spot sits back at 15685 off recent highs in the 15730/35 region. The 20-day EMA sits near 15655, but arguably more important support is at the 100-day EMA down at 15570, a support level we haven't breached since late last year. The rupiah is still the worst performing EM Asia currency in the past week, down 0.60% in spot terms. Portfolio flows in the equity and bond space from offshore investors remain flat to negative. US real yields (10yr basis) are off recent highs, but domestic uncertainty around the new government and its fiscal outlook may be keeping some investors on the sidelines.

- USD/MYR sits up off earlier lows, last near 4.7400, down slightly for the session. Earlier (per BBG) we touched 4.7250, which was fresh lows back to early Feb for the pair. This also put us under the 50-day EMA (near 4.7310), although we haven't been able to sustain this break. MYR is now up around 0.80% for the week, the best performer in the EM Asia FX space. The clear step up in verbal rhetoric around concern for MYR weakness from the PM, BNM Governor and second Vice Finance Minister (who warned that the authorities were prepared to intervene) has been a key factor in the turnaround.

- USD/PHP sits lower, last near 56.00, around 0.30% stronger in PHP terms. There hasn't been a clear macro catalyst for the rebound but clear of month end USD demand may be helping.

- USD/THB has firmed slightly, but remains sub 36.00. The Feb PMI ticked lower to 45.3 from 46.7. This is close to recent cyclical lows and underscores the economic headwinds facing the Thailand economy at the moment.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/03/2024 | 0730/0830 | ** |  | CH | Retail Sales |

| 01/03/2024 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/03/2024 | 0845/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/03/2024 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/03/2024 | 0855/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 01/03/2024 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/03/2024 | 0930/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/03/2024 | 1000/1100 | *** | | EU | HICP (p) |

| 01/03/2024 | 1000/1100 | ** | | EU | Unemployment |

| 01/03/2024 | 1000/1100 | *** | | IT | HICP (p) |

| 01/03/2024 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 01/03/2024 | 1400/1400 | | UK | BOE's Pill Speech at Cardiff University | |

| 01/03/2024 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/03/2024 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 01/03/2024 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 01/03/2024 | 1500/1000 | * | | US | Construction Spending |

| 01/03/2024 | 1515/1015 | | US | Fed Governor Chris Waller | |

| 01/03/2024 | 1515/1015 | | US | Dallas Fed's Lorie Logan | |

| 01/03/2024 | 1715/1215 | | US | Atlanta Fed's Raphael Bostic | |

| 01/03/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 01/03/2024 | 1830/1330 | | US | San Francisco Fed's Mary Daly | |

| 01/03/2024 | 2030/1530 | | US | Fed Governor Adriana Kugler |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.