Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Core markets looked through the latest liquidity injection from the PBoC and solid Chinese economic docket in Asia-Pac hours.

- Short-term COVID-19 pain and the fiscal impasse in DC remain at the fore, with tomorrow's FOMC decision also eyed.

BOND SUMMARY: Narrow Ranges In Play Overnight, Lack Of Catalysts Noted

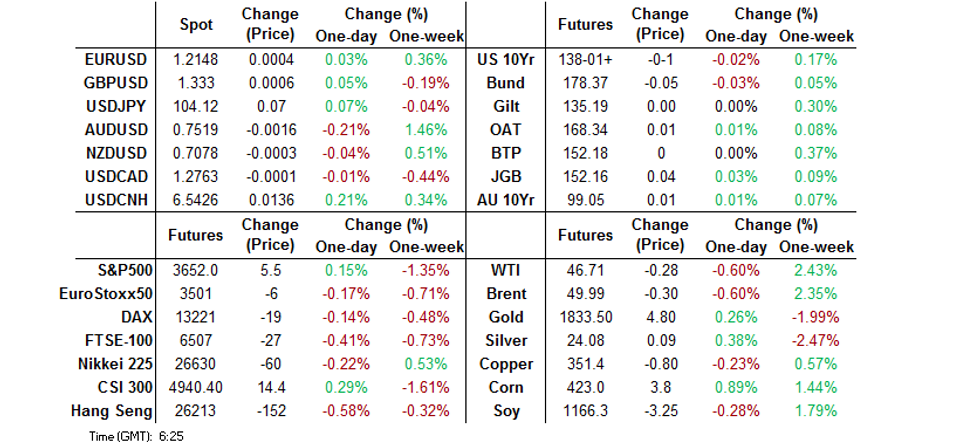

T-Notes stuck to a narrow 0-02+ range in Asia-Pac hours, last +0-00+ at 138-03, with cash Tsys sitting unchanged to 1.0bp richer across the curve, as the long end sees some marginal outperformance. The space has shrugged off the release of the latest round of Chinese economic activity data, PBoC MLF activity and comments from U.S. Senate Majority Leader McConnell as he re-affirmed the need for Congress to bridge its differences and come to a deal re: fiscal support before Christmas (this isn't new and McConnell has maintained his well-defined red lines re: the matter in recent days). Overnight flow was headlined by a block trade which saw 10K of the TYG1 137.00/136.50 put spread bought vs. TYG1 139.50 calls, with the package trading at -0-01.

- It was a sedate Tokyo session for JGB futures, with the contract continuing to operate in familiar territory, finishing +4 on the day. The cash curve saw light twist steepening for most of the session, given the potential for additional 40-Year JGB issuance (as outlined by primary JGB dealers at recent MoF meetings and flagged previously), which could be deployed to finance the latest supplementary budget (although, as outlined previously, total issuance requirements for the package will seemingly be in the region of the median view, avoiding the more burdensome end of the scale. The maturity mix of the issuance will be key). Late in the day we saw local press reports suggest that the supplementary budget will see the Japanese government set aside another Y1tn for its Go To travel campaign (the scheme will be halted over the New Year period, given the current COVID worry, with PM Suga battling against a continued slide in the opinion polls).

- The Aussie bond space looked through the release of the minutes of the RBA's December monetary policy decision, with YM finishing at unchanged levels and XM +0.4. There was always a high bar for the release re: its potential to be market moving, with the Bank affirming recent rhetoric from the RBA Governor surrounding the evolution of its QE scheme: "Members agreed to keep the size of the bond purchase program under review. At its future meetings, the Board will closely monitor the effects of the bond purchases on the economy and on market functioning, as well as the evolving outlook for jobs and inflation. The Board is prepared to do more if necessary."

FOREX: Low Conviction Session In Asia

Headline flow was few and far between in Asia, keeping G10 FX rangebound, with participants awaiting further clarity on U.S. fiscal matters and global restriction tightening. The Antipodeans landed at the bottom of the pile, with simmering Sino-Australian trade tensions eyed.

- AUD/USD blipped higher in early trade, but more than erased gains and last sits down 25 pips at $0.7510. The decline in NZD/USD was shallower, the rate last trades down 7 pips at $0.7074. AUD/NZD retreated after failing to punch through its 200-DMA over the past two days. RBA December meeting minutes release was broadly in line with market expectations.

- JPY crosses were bought into the Tokyo fix, possibly on the back of Gotobi day demand. USD/JPY extended gains thereafter, but AUD/JPY retreated into negative territory.

- The PBOC fixed the USD/CNY mid-point at 6.5434, 73pips weaker than Monday, and injected CNY950bn at an unchanged rate of 2.95%, more than offsetting the CNY 300bn of MLF loans that mature tomorrow (Dec 16) and the CNY 300bn that rolled off on Dec 7. USD/CNH extended gains after the cash injection. Chinese economic activity indicators fell in line with expectations.

- The greenback generally outperformed Asian EM FX. KRW, IDR & MYR were the main laggards in the region.

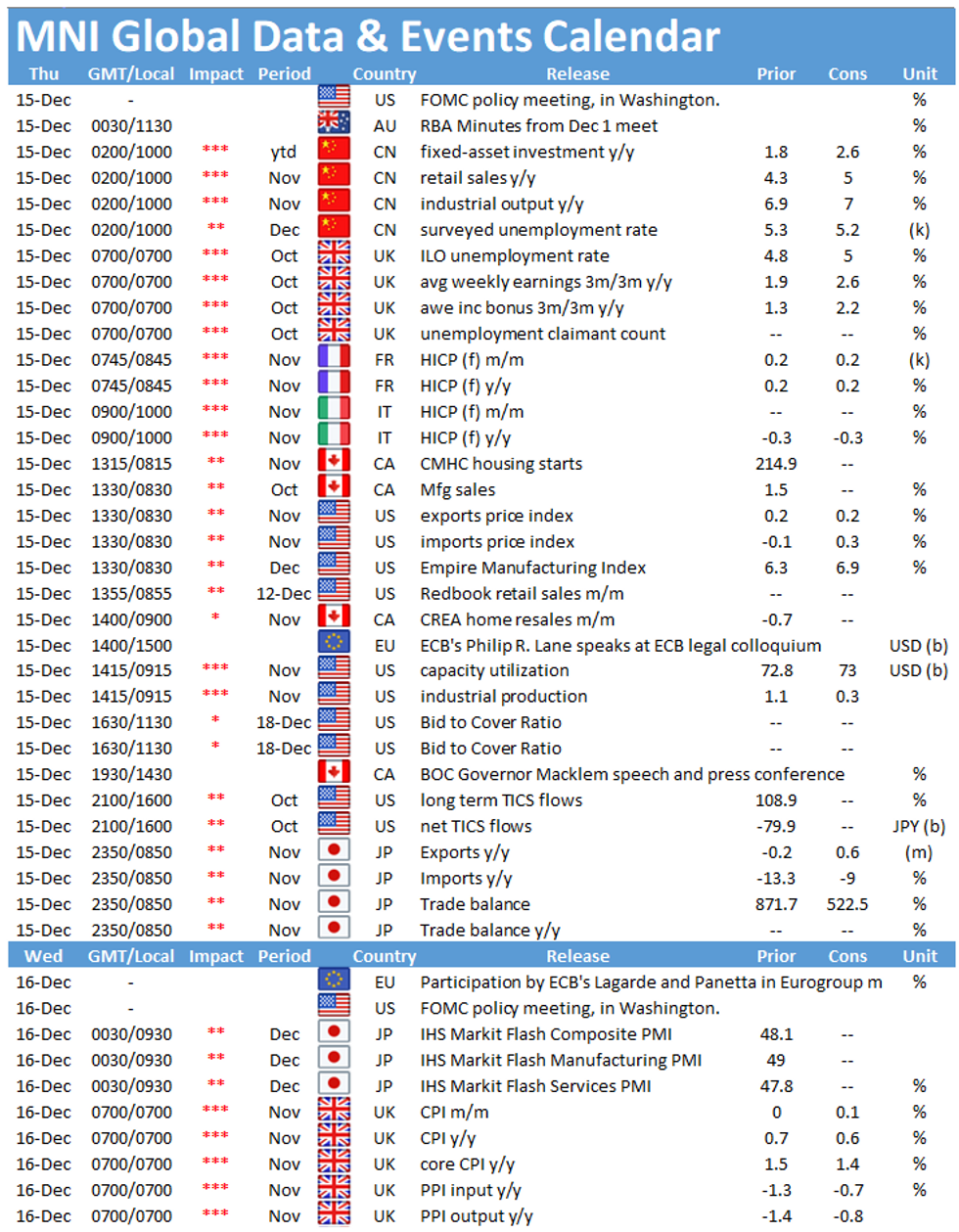

- Focus turns to UK labour mkt report, final French & Italian CPIs, U.S. industrial output & Empire M'fing, Canadian housing starts as well as comments from ECB's Rehn & BoC's Macklem.

FOREX OPTIONS: Expiries for Dec15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E1.2bln), $1.2100(E1.1bln-EUR puts),

$1.2125-35(E1.0bln-EUR puts), $1.2150-55(E486mln-EUR puts), $1.2175(E1.0bln-EUR puts) - USD/JPY: Y102.90-00($746mln), Y104.00($559mln),

Y104.50-55($948mln), Y104.96-105.00($533mln) - EUR/JPY: Y123.70(E501mln)

- EUR/GBP: Gbp0.8950-58(E1.1bln)

- AUD/USD: $0.7420(A$802mln-AUD puts)

- USD/CNY: Cny6.50($1.8bln), Cny6.5920($690mln), Cny6.65($2.0bln)

EQUITIES: Mixed Overnight

E-minis traded in mixed fashion overnight, although all 3 major contracts sit above neutral levels at present, with broader risk assets looking through the latest round of Chinese economic data, PBoC liquidity injection via MLF operations and familiar rhetoric from senior policymakers re: fiscal stimulus.

- Meanwhile, the major regional Asia-Pacific indices were lower in the main.

- This comes after the major Wall St. benchmarks gave back their early gains and more on Monday, as focus turned to immediate COVID-19 worry surrounding London and New York.

- Nikkei 225 -0.2%, Hang Seng -0.6%, CSI 300 +0.2%, ASX 200 -0.4%.

- S&P 500 futures +7, DJIA futures +55, NASDAQ 100 futures +8.

GOLD: Back To Familiar Territory After Look Below Support

Gold pushed through initial technical support on Monday (in the form of the Dec 7 low at $1,822.5/oz), but failed to close below as the early risk positive flows waned and U.S. real yields retraced. Spot has moved back above the familiar $1,835/oz level, although bears remain focused on yesterday's low of $1,818.90/oz. A break there would expose the Dec 2 low at $1,807.5/oz. To the upside, familiar bullish targets remain in focus.

OIL: Marginally Lower

WTI & Brent sit ~$0.30 below their respective settlement levels, with the major regional Asia-Pac equity indices also trading lower, while e-minis have lacked a firm sense of direction.

- This comes after the major crude benchmarks managed to finish a touch higher on Monday, even with questions surrounding demand owing to broader COVID-19 related worry re: New York & London. Geopolitical tensions, most notably in the Middle East, ultimately helped underscore the crude bid, even as equity markets faded on the aforementioned COVID-19 worry.

- In terms of crude specifics, the latest OPEC monthly report saw the cartel mark down its '20 and '21 global crude demand forecasts, the latest indication of issues on that side of the coin. Elsewhere, reports pointing to a marginal uptick in Libyan crude output and worry re: a relatively imminent uptick in Iranian crude supply were noted.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.