- There was some focus on the deaths of the Iranian President and Foreign Minister in a helicopter crash. There is concern that President's death could leave a power vacuum and destabilise the world’s third largest oil producer, but Ayatollah Ali Khamenei said that there “won’t be any disruption to the country’s affairs”.

- Oil prices are little changed, while gold has risen to fresh record highs, likewise for copper. The A$ has outperformed modestly on firmer metal prices.

- Elsewhere, JGBs continue a downward trend, with yields making fresh highs. This isn't lending support to the yen though.

- Later the Fed’s Bostic, Barr, Waller, Jefferson and Mester speak. There are no data of note.

MARKETS

US TSYS: Treasury Futures Little Changed, Busy Day Ahead For Fed Speakers

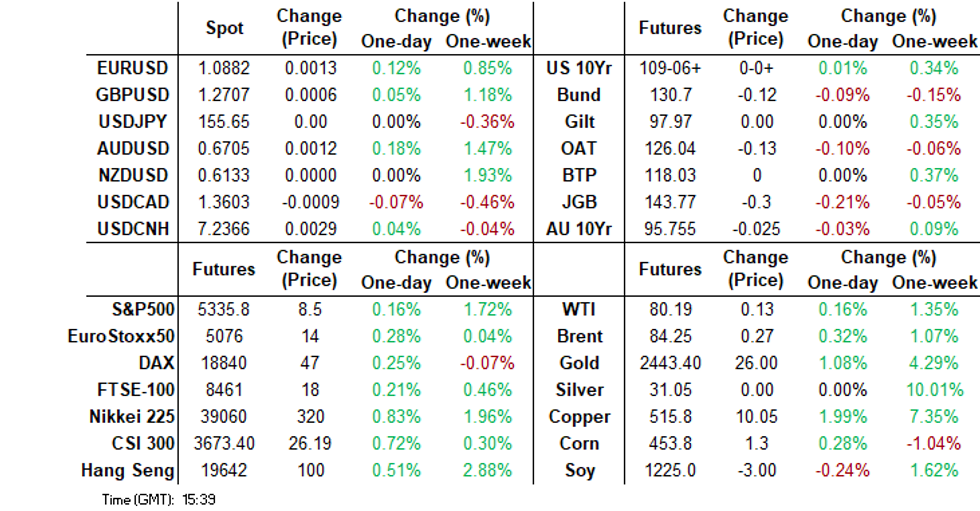

- Treasury futures are little changed today with the 10Y contract now (+ 00+) at 109-06+, the contract made highs of 109-09 and lows of 109-05, while the 2Y contract is (+ 00.375) at 101-22.75

- The treasury curve is little changed today with yields were flat to 1bps lower, the 2Y yield -0.7bps at 4.818%, 10Y -0.8bps to 4.412%.

- Tsys Flows today: A 20k likely buyer of TYM4 110 calls, 0.03 at 10:24:49 AEST, and a block seller of 1,800 FVM4 105-29.25

- Across local rate markets: ACGBs yields are 2-3bps higher, curve slightly steeper, NZGBS 1-2bps higher, curve steeper, while JGBs 1-4bps higher with the 10y yield rising to 0.975% for the first time since 2013

- Rate cut projections remain largely in-line with this morning's levels (*): June 2024 at -10% w/ cumulative rate cut -2.5bp at 5.313%, July'24 at -22% w/ cumulative at -8bp at 5.258%, Sep'24 cumulative -21.1bp, Nov'24 cumulative -29.2bp, Dec'24 -44.4bp

- Today, there is little on teh data calendar with markets focusing on Fed speakers including Raphael Bostic, Christopher Waller, Philip Jefferson, Loretta Mester and Michael Barr.

JGBS: Solid Demand At Linker Auction, 10yr Yield At Highest Levels Since 2013

JGB futures got to lows of 143.78 post the lunchtime break, but we have since stabilized somewhat. JBM4 was last around 143.81, -.26, generally maintaining a downside bias in the first part of trade today.

- Downside focus will be on recent lows near 143.70. There has been little spill over from US Tsys today, with 10yr futures largely tracking sideways.

- The 10yr linker auction drew a strong bid to cover ratio of 4.27 (the highest since 2007). The broader backdrop is also focused on the BoJ outlook, with the latest MNI interview with an ex BoJ official noting we could see a cut to BoJ bond purchases at the June meeting (see this link).

- Cash JGB yields remain on the front foot, with the 10yr up to 0.975%, fresh highs going back to 2013. We continue to see firmer yield gains at the back end of the curve, the 20-40yr tenors seeing yield gains of around 3bps. The 10yr swap rate is back near 1.025.

- Tomorrow the data calendar is relatively light.

AUSSIE BONDS: ACGBs Cheaper, Curve Steepens, RBA Minutes Tomorrow

ACGBs (YM -2.0 & XM -2.0) are cheaper today, it was a slow and uneventful day with no local headlines or data out. Looking ahead tomorrow we have Westpac Consumer Confidence for May due out and the RBA minutes of May policy meeting.

- Cross-asset moves: Equities are higher today, ASX200 is up 0.64%, while US equity futures are current about 0.15% higher. In FX the BBDXY is little changed today with the AUD is up about 0.20%, while Iron Ore was up 0.89% at $118.25/ton

- US treasury futures are slightly higher in Asia trading, the 10Y contract is (+ 01) at 109-07, after earlier making highs of 109-09, while volumes are on the low side, yields are about 1bp lower across the curve. In tsys flows there was earlier a block seller of FV, and a likely buyer of 20k TY Jun 24 110 calls.

- The ACGB curve has bear-steepened today with the 2y10y +0.340 at 30.110, yields are 1-3bps higher, while the AU-US 10-year yield differential is 3bps higher today at -18bps

- Swap rates are are 1-2bps lower today

- The bills strip is flat to 1bps lower.

- RBA-dated OIS implied rate is little changed this morning with 18bps of easing into the year-end to a terminal rate of 4.17%

- Looking ahead, Westpac Consumer Conf & RBA Minutes

AUSTRALIA: Government Increases Support Post Budget, Voters Don't Believe It’s Disinflationary

According to The Australian’s Newspoll voters don’t believe that last week’s budget will make them better off and will make inflation worse, but it has boosted support for PM Albanese and his Labor party increasing speculation of an early election. The two-party preferred split has widened to 52:48. The next election is due before May 2025.

- 27% believe that they will be better off financially from the budget with 29% saying worse off, which is an improvement on last year’s 20% and 36%. But 39% said it would make inflation worse while 15% said better and 34% no difference, which was in line with last year. Voters don’t seem to think that inflation will fall to below target as Treasurer Chalmers expects. The numbers viewing the budget as good or bad for the economy were equal at 27%. In May 2023, 33% said it would be “good”.

- Support for the incumbent Labor party rose 1pp to 34% while the opposition coalition fell 1pp to 37%. The Greens increased 1pp to 13% but remained in the range they’ve been in since mid-2023. The survey was taken May 16-18 while the budget was released May 14.

- Albanese remains the preferred PM increasing his support 4pp to 52% compared with opposition leader Dutton who fell 2pp to 33%.

NZGBS: Cheaper, RBNZ Survey Shows Household Inflation Expectation Falls

NZGBs are flat to 1.5bps cheaper today, the curve has bear steepened. It has been a slow day, RBNZ published Q2 household expectations survey earlier with the two-year inflation expectation now at 3% down from 3.2% in Q1, otherwise the market will be waiting for the RBNZ rate decision on Wednesday were they are widely expected to keep rates on hold.

- US treasury futures are slightly higher in Asia trading, the 10Y contract is (+ 01) at 109-07, after earlier making highs of 109-09, while volumes are on the low side, yields are about 1bp lower across the curve. In tsys flows there was earlier a block seller of FV, and a likely buyer of 20k TY Jun 24 110 calls.

- The NZGB curve is steeper, but trading near session best at the moment, the 2Y +0.5bps at 4.674%, 10Y is +1.0bps at 4.596%.

- Earlier, The RBNZ's 2Q household expectations survey shows a decrease in the median expected inflation rate for the next two years to 3% from 3.2% in 1Q, and for the next year to 4% from 5%. The median expected inflation in five years remains at 3%. The mean expected inflation in two years is unchanged at 3.6%. Additionally, 52% of respondents expect higher house prices, with the median expected house price inflation in one year at 0%.

- Swap rates are flat to 1bps lower

- RBNZ dated OIS is slightly today today down 2bps heading into year-end with cumulative 47bps of easing now.

- Looking Ahead: RBNZ on Wednesday

FOREX: A$ Outperforms On Higher Metals, Steady Trends Elsewhere

The BBDXY USD index sits a touch under end levels from last week, last around 1244.80/85. Overall trends have been fairly muted in the FX space in Monday trade to date.

- AUD/USD has outperformed marginally, up around 0.20%. Commodity prices remain favorable from a metals standpoint, with copper hitting a fresh record high. Regional equity sentiment is mostly positive as well.

- US equity futures are marginally higher as well, while US yields are down a touch, losses are close to 1bps at this stage.

- AUD/JPY is tracking higher, last near 104.45. We aren't too far away from late April highs of 104.94.

- USD/JPY has risen a touch but hasn't broken back above 156.00 (the pair last 155.75/80).

- NZD/USD is down a touch to 0.6125/30. A Q2 RBNZ survey of inflation expectations showed households saw a slightly lower median expected inflation rate for the next two years at 3% from 3.2% in 1Q. The RBNZ meeting on Wednesday is expected to be unchanged.

- Later the Fed’s Bostic, Barr, Waller, Jefferson and Mester speak. There are no data of note.

ASIA STOCKS: HK & China Equities Head Higher, Property Off Morning Lows

Hong Kong & Chinese equities have opened higher today, the main focus today has been on the property space after the Chinese government announced new measures to support the sectors on Friday, however many analysts have mixed views on how much the recent announcements will do to help the struggling sector, while China EV makers are taking longer than ever before to pay their suppliers. Earlier, China left the 1 & 5yr LPRs unchanged.

- Hong Kong equities are mostly higher today, property indices initially opening lower with the HS Property Index opening down 1.40% however has recovered to now trade up 0.95%, while he Mainland Property Index now trades unchanged for the day. The HSTech Index is up 0.60%, while the HSI is up 0.50%. In China onshore markets, the CSI300 is trading up 0.20% while the the small-cap CSI1000 Index, up 0.30% and the ChiNext is up 0.21%.

- On Friday, The Chinese government announced a comprehensive support package to revive its struggling property market, including relaxed mortgage rules and encouraging local governments to purchase unsold homes. This move aims to mitigate the sector's impact on economic growth. The measures include lower down-payment requirements, central bank funding, and various incentives to stabilize the market. However, there are concerns about whether these measures will be sufficient to address the deep-rooted issues within the property sector and stimulate long-term demand.

- China's electric car market is facing significant stress, with companies like Nio and Xpeng taking much longer to pay suppliers due to sluggish economic growth, reduced demand, and intense price wars. This delay is impacting auto-parts suppliers, increasing their receivables and reducing cash reserves, potentially leading to a "messy consolidation" as weaker suppliers face bankruptcy, per bbg.

- Looking ahead, quiet week for China on the data front, Hong Kong has Unemployment Rate later today

ASIA PAC STOCKS: Equities Head Higher, Miners Top Performers On Strong Metal Prices

Asian markets are higher today, boosted by China property market and US equities climbing to fresh highs on Friday thanks to strong earnings, the MSCI Asia Pacific is on track for its seventh straight day of gains and is currently up about 0.70%, with mining stocks rallying on strong commodity prices. It has been a relatively quiet session, very little in the way of economic data.

- Japan equities are higher today, materials stocks are higher as copper and oil continue to rise. Semiconductor names are slightly lower after the Philadelphia SE Semiconductor Index fell on Friday ahead of Nvidia earnings due out later this week. The Nikkei 225 is up 0.89% and is closing back in on the 40,000 mark, while the Topix is up 0.77%.

- South Korean equities are higher today as the Kospi edges closer to the year-to-date highs up 0.63%, Samsung and SK Hynix hare the top performers, small caps are underperforming today with the Kosdaq down 1.24%

- Taiwan equities are lower today, with the Taiex down about 0.45% with TSMC is the biggest drag on the index after the Philadelphia SE Semiconductor Index traded lower on Friday. We have Export orders due out a bit later today and Industrial Production on Thursday.

- Australian equities are higher today led by mining and energy stocks, the moves are largely tracking US equities from Friday as well as China taking steps to support their local property market. The ASX200 is up 0.68%

- Elsewhere in SEA, New Zealand equities are up 0.14%, Indonesian equities are up 0.18%, Philippines equities are up 0.94%, Malaysian equities are up 0.76%, Indian equities are up 0.16%.

ASIA EQUITY FLOWS: Equity Flows Mixed, Indonesia Breaks Selling Streak

- South Korean equity markets were lower on Thursday with a $275m outflow. South Korea’s Financial Supervisory Service Governor Lee Bokhyun said his “personal desire and plan” is to see stock short selling partially resumed in South Korea in June. The 5-day average is now $65m, just below the 20-day average of $70m, although well down on the longer term 100-day average at $172m.

- Taiwan equities were lower on Friday, foreign investors bought just $92m of equities on which was well down on the $1.7b purchased on Thursday. The 5-day average now sits at $738m, well above the 20-day average at $172m and the 100-day average at $96m.

- Thailand equities were higher on Friday with foreign investors buying $23m of equities a touch below tee 5-day average. Later today we have GDP. The 5-day average now at $28m, the 20-day average $0.7m, while the 100-day average is -$18.21m.

- Indonesian equities had had their second straight day of inflows, after ending over a month straight of outflows. The 5-day average now -$18m in slightly above the 20-day average at -$43m while the 100-day average is still positive at $5.3m.

- Philippines equities were higher on Friday, with a small inflow of $0.54. Later today we have BoP Overall. The 5-day average is $10m, above the 20-day average at -$17m and the 100-day average of -$2.95m

- Indian equities have seen foreign investors sell stocks for the 11th straight session. The 5-day average now -$267m, the 20-day average is -$214m while the 100-day average is still positive but declining quickly and sits at $23m.

- Malaysian equities continue making new highs with the Malay KLCI trading above 1,600. Equity flows have been positive for the past two weeks, with just a single $2.2m outflow on Apr 9th. The 5-day average now $32m, in line with the 20-day average at $27m and above the longer term 100-day average at $0.23m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -276 | 326 | 15223 |

| Taiwan (USDmn) | 92 | 3693 | 4469 |

| India (USDmn)* | -280 | -2060 | -3343 |

| Indonesia (USDmn) | 54 | -94 | 50 |

| Thailand (USDmn) | 23 | 143 | -1826 |

| Malaysia (USDmn) * | 64 | 160 | -36 |

| Philippines (USDmn) | -1 | 43.9 | -276 |

| Total | -324 | 2211 | 14261 |

| ** Data Up To Apr 16th |

OIL: Crude Little Changed Today Despite Geopolitical Events

Oil prices are slightly higher during APAC trading today as the risk tone remains favourable. Brent is up 0.2% to $84.12/bbl after a high of $84.30. WTI is 0.1% higher at $79.65/bbl after reaching $79.83. Supply risks remain the focus with instability in Russia/Ukraine and the Middle East. The USD index is slightly lower.

- The crash site of Iran’s President Raisi’s helicopter has been found and he and the foreign minister were killed. There is concern that his death could leave a power vacuum and destabilise the world’s third largest oil producer, but Ayatollah Ali Khamenei said that there “won’t be any disruption to the country’s affairs”.

- Over the weekend an oil tanker was hit by Houthis off the coast of Yemen and Ukraine struck Russia’s Slavyansk refinery again causing operations to cease. It refines 80kbd. But there has been little reaction in APAC trading.

- Money managers’ net long crude positions fell for a second straight week, according to Bloomberg.

- Later the Fed’s Bostic, Barr, Waller, Jefferson and Mester speak. There are no data of note.

GOLD: Fresh Record Highs

Bullion touched a fresh record high in the first part of Asia Pac trade. We got to $2440.59, but sit slightly lower now, last near $2438. We are still up 0.90% on Friday levels and this follows a +2.3% gain for gold last week.

- Broader USD sentiment has been relatively steady so far today, with the BBDXY index little changed near 1245. Still, some risk aversion may be creeping into markets given the on-going Israel-Hamas conflict and the reports of the death of the Iranian President and Foreign Minister in a helicopter crash.

- There are no reports of external involvement in the crash, with US Senator Chuck Schumer stating US intelligence agencies indicated there was no evidence of foul play. We broader tensions in the region still elevated though, the news may have lent some support to gold today.

- Broader commodity sentiment is positive in the metals space today, with copper continuing to track higher.

ASIA FX: THB Surges, Aided By Q1 GDP Beat, Steady Trends Elsewhere

USD/Asia pairs are mixed for the most part, outside of strong THB gains. We have seen some modest USD support elsewhere but overall gains are muted at this stage. Baht is up 0.90%, aided by stronger than expected GDP figures for Q1. Still to come today we have Taiwan export orders and the current account balance. Tomorrow, South Korea consumer confidence is out, along with first 20-days of trade data for May as the main focus points.

- USD/CNH is marginally higher for the session, last near 7.2370. Onshore spot has also risen a touch to 7.2300. Equity markets are higher, albeit modestly, as markets digest the recent property support measures. Onshore media expect mortgage rates to come down, while property developers also noted a pick up in weekend activity from China home buyers. Outside of this the yen is slightly weaker, likely curbing yuan sentiment to a degree.

- 1 month USD/KRW is slightly higher, last around 1352, against earlier highs above 1355. We have tracked recent ranges in the first part of Monday dealing. Cross asset wise onshore equities are higher, the Kospi +0.55%, shrugging off a negative tech lead from the end of last week. Tomorrow the focus will rest on household inflation expectations and momentum in trade for the first 20-days of May.

- USD/THB has fallen sharply. The pair was last under 36.90, around 0.9% stronger in baht terms for the session. This is fresh lows in the pair back to mid March. Part of this is catch up to weaker USD trends from late last week (post the onshore spot close). However, it has outperformed the rest of the USD/Asia bloc comfortably. This morning's Q1 GDP beat is a positive, with growth up 1.1% q/q, versus 0.6% forecast. Y/Y growth was at 1.5%, versus 0.8% forecast but slightly slower than the Q4 pace. Growth reflected a resilient consumption backdrop, with drags from government spending and investment. Given scope for government spending to improve, couple with the digital wallet rollout, this result may temper pessimism around the domestic growth backdrop, which could alleviate some pressure on BoT.

- Elsewhere, SGD and MYR sit marginally higher against the USD. USD/MYR last near 4.6840, USD/SGD around 1.3440/45. Earlier Malaysian trade data was a little bit weaker than expected but still showed a recovery in export growth (to 9.1% y/y from -0.9%).

- USD/PHP is tracking higher, last in the 57.75/80 region, but we remain below recent highs. USD/IDR was last just under 15980.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 20/05/2024 | 0900/1000 |  | UK | BOE's Broadbent Monetary Mechanism Workshop | |

| 20/05/2024 | - | | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 20/05/2024 | 1530/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 21/05/2024 | 0130/1130 |  | AU | RBA Minutes | |

| 21/05/2024 | 0800/1000 | ** |  | EU | Current Account |

| 21/05/2024 | 0900/1100 | ** | | EU | Construction Production |

| 21/05/2024 | 0900/1100 | * | | EU | Trade Balance |

| 21/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 21/05/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 21/05/2024 | 1230/0830 | *** |  | CA | CPI |

| 21/05/2024 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 21/05/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 21/05/2024 | 1300/0900 | | US | Fed Governor Christopher Waller | |

| 21/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 21/05/2024 | 1700/1800 | | UK | BOE's Bailey Lecture at LSE | |

| 21/05/2024 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic | |

| 21/05/2024 | 2300/1900 | | US | Cleveland Fed President Loretta Mester |