Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

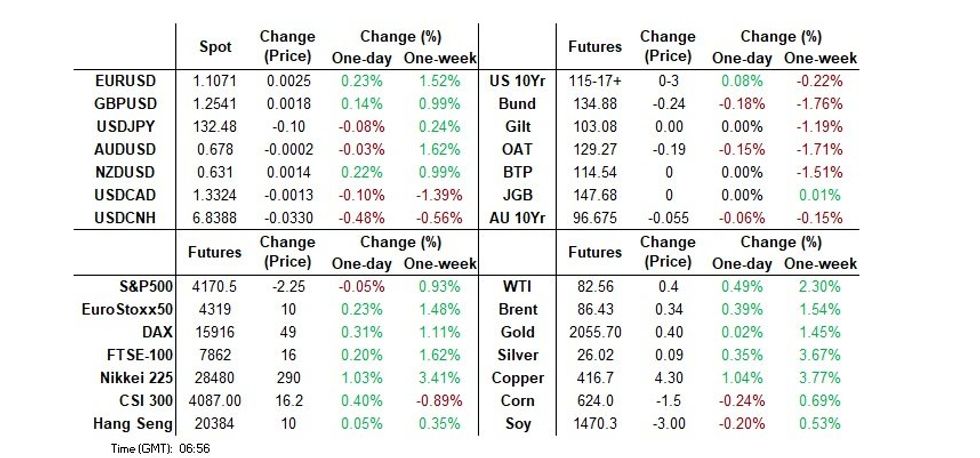

- The USD remained on the defensive during Asia-Pac hours.

- The positive lead from Wall St. and the continuation of the recent USD softening generally supported Asia-Pac equities into the weekend. E-minis were incrementally lower vs. settlement, holding to a tight range, with focus on large cap financial earnings later today (J.P.Morgan, Wells Fargo, Citi & BlackRock), which come in the wake of the well documented banking tumult seen in March. There wasn’t much impact from Boeing warning that it will likely have to reduce deliveries of its 737 Max plane owing to part issues, although the company noted that the problems caused are not an “immediate safety of flight issue and the in-service fleet can continue operating safely.”

- U.S. retail sales data, the inflation expectations component of the latest UoM sentiment survey and Fedspeak from Goolsbee & Waller will provide the meaningful macro inputs ahead of the weekend, with a limited docket apparent in the remainder of the Asia-Pac session and during the London morning (Swedish CPI, as well as final CPI readings from France & Spain provide the pre-NY highlights). Comments from ECB’s Nagel & BoE’s Tenreyro supplement the previously outlined events but shouldn’t be needle movers given the recent rounds of rhetoric from the two and Tenreyro’s soon to be departing status.

US TSYS: Curve Marginally Flattens In Muted Asian Session

TYM3 deals at 115-18, +0-03+, with a 0-04 range on volume of ~65k.

- Cash tsys sit flat to 1.5bps richer across the major benchmarks, the curve is a touch flatter.

- There was a muted start to dealing with cash tsys little changed in early dealing, ranges were narrow with little follow through on moves.

- Tsys marginally richened as USD was marginally pressured as an offer in USD/CNH led the greenback lower.

- Little meaningful macro headline flow crossed through the session.

- FOMC dated OIS price ~18bp hike into the May meeting with a terminal rate of 5%. There are ~65bps of cuts priced for 2023.

- In Europe today we have the final print of French CPI and ECB-speak from Lagarde and Panetta. Further out we have US Retail Sales, Business Inventories, Industrial Production and UofMich Consumer Sentiment. Fedspeak from Chicago Fed President Goolsbee and Fed Governor Waller will cross.

JGBS: Hovering Around Unchanged Into The Weekend

The JGB space hasn’t really managed to generate anything in the way of a meaningful move away from early Tokyo levels, with futures -2 as we move towards the close, while cash JGBs operate within 1bp of yesterday’s closing levels.

- An uptick in swap rates, resulting in swap spread widening and swap curve steepening, will have applied some light pressure to JGBs.

- Headline flow from Finance Minister Suzuki & BoJ Governor Ueda didn’t move the needle, failing to introduce fresh, tangible information.

- BoJ Rinban operations (covering 1- to 10- & 25+-Year JGBs) also did little for JGBs.

- In the corporate bond space, Berkshire Hathaway priced ~Y165bn of bonds in a 5-part deal, after Warren Buffett pointed to increased investment in Japanese trading houses in recent days.

- Market chatter has turned towards the investment intention outlines for the domestic life insurer and pension fund community, with the potential for a meaningful BoJ policy pivot, in addition to the volatility observed in wider financial markets alongside the well-documented, elevated FX-hedging costs that Japanese investors currently face, generating even deeper than normal interest in the capital deployment plans of this sizable investor cohort (the semi-annual outlines will likely filter out over the next couple of weeks or so).

- Looking ahead to next week, national CPI data and 20-Year JGB supply provide the highlights of the local docket.

AUSSIE BONDS: Holding Cheaper & Steeper, ACGB Dec-34 Syndication Slated For Next Week

Aussie bond futures operated in relatively close proximity to their respective overnight lows for most of Friday’s Sydney session, with a shallow look through the overnight base in YM futures failing to generate a meaningful extension. The former sits -2.0, while the latter is -4.5. Wider cash ACGB trade sees 2.5-5.5bp of cheapening, with the overnight/early Sydney bear steepening impulse remaining in play.

- There hasn’t been much in the way of meaningful local news flow to shape price action, which left participants pondering and adjusting to price action in wider markets for most of the day.

- The AOFM’s announcement re: its intent to issue the new ACGB Dec-34 via syndication next week applied some brief pressure to XM futures, although the overnight/early Sydney lows in the contract held, before it bounced back towards pre-syndication announcement levels. A quick reminder that the AOFM had previously outlined its intention to introduce ACGB Dec-34 in the current quarter.

- Bills sit flat to 3bp cheaper through the reds, off lows, with a modest steepening bias.

- RBA-dated OIS is little changed on the day, with the terminal rate pricing hovering at ~3.65%, and just under 15bp of cuts priced by year-end (vs. the current terminal cash rate pricing).

- Looking ahead, the minutes from the most recent RBA meeting, CBA household spending data and flash Judo Bank PMI prints headline locally next week.

NZGBS: Curve A Touch Steeper On The Day

NZGBs held steeper on the day, with little in the way of net movement outside of the early catch up to Thursday’s moves in U.S. Tsys, leaving NZGB benchmarks 2-5bp cheaper at the bell. Swap rates generally mimicked those moves, leaving swap spreads little changed.

- Locally, Finance Minister Robertson outlined ~NZ$9-10bn rebuild costs for Cyclone Gabrielle, although he pointed to that being spread over “many years”, also telling BBG that he wanted to minimise the amount of borrowing deployed when it comes to funding the spending. Finally, Robertson conceded that it is possible that NZ is already in a technical resilience, but pointed to various areas of economic resilience that he hoped would result in a shallow and short-lived recession (in the case that scenario is realised).

- When it comes to RBNZ pricing, RBNZ-dated OIS continues to show 20bp of tightening for the Bank’s next meeting, while terminal OCR pricing continues to hover just below 5.50%.

- Locally, manufacturing PMI data moved back into contractionary territory after a two-month hiatus, although survey sponsor BNZ noted that "disappointing as New Zealand’s March PMI was, it wasn’t especially negative in longer-term context. Neither was it much out of line with manufacturing readings across the world of late.”

- Looking ahead, Q1 CPI data dominates next week’s local docket.

FOREX: USD Moderately Pressured In Asia

The greenback is moderately pressured in Asia today, BBDXY is down ~0.2% last printing at 1214 a touch above year to date lows (1210.29)

- Kiwi is firmer, NZD/USD has consolidated Thursday's gains and sits a touch above the $0.63 handle. There was little reaction to the fall in March BusinessNZ Manufacturing PMI. The measure fell to 48.1 with February's print revised lower to 51.7.

- Yen is also firmer, USD/JPY is ~0.2% softer. The pair last prints at ¥132.35/45. Technically yesterday's price action added to the evidence that the latest recovery was corrective in nature. Bears now target a break of low from Apr 10 (¥131.83) which open ¥130.64 the low from Apr 5 and key support.

- AUD/USD is little changed from yesterday's closing levels. The pair has observed a narrow range with little follow through. Resistance was seen ahead of yesterday's high.

- Elsewhere in G-10 EUR/USD is through yesterday's high printing its highest level of 2023. Resistance was seen at $1.1076 the high from Apr 1 2022.

- Cross asset wise; regional equities firmer benefitting from the strong lead from Wall St. US Treasury Yields are little changed across the curve.

- In Europe today we have the final print of French CPI and ECB speak from Lagarde and Panetta. Further out we have US Retail Sales, Business Inventories, Industrial Production and UofMich Consumer Sentiment.

FX OPTIONS: Expiries for Apr14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0890-00(E2.2bln), $1.0950(E1.1bln), $1.1000(E1.8bln), $1.1050(E630mln)

- USD/JPY: Y130.00($1.2bln), Y132.00($910mln), Y133.00($661mln), Y134.00($602mln)

- NZD/USD: $0.6400(N$1.1bln)

- USD/CAD: C$1.3440-45($1.7bln)

- USD/CNY: Cny6.8000($503mln), Cny6.9000($914mln), Cny6.9050($514mln)

EQUITIES: APac Equities Bid, E-Minis Little Changed To A Touch Softer Ahead Of Bank Earnings

The positive lead from Wall St. and the continuation of the recent USD softening generally supported Asia-Pac equities into the weekend, with the major benchmarks running 0.3-1.2% firmer.

- The Nikkei 225 outperformed, aided by quarterly earnings from Fast Retailing, which were accompanied by an upgrade in the company’s full-year operating profit guidance.

- There hasn’t been much in the way of meaningful news flow catalysts since the NY-Asia handover, but we note that northbound net flows seen in the HK-China Stock Connect schemes are running at the highest level since March 17. This comes after Chinese President Xi called on foreign investors to deepen their presence in Chinese markets as the country improves its business operating environment (on Thursday).

- E-minis were incrementally lower vs. settlement, holding to a tight range, with focus on large cap financial earnings later today (J.P.Morgan, Wells Fargo, Citi & BlackRock), which come in the wake of the well documented banking tumult seen in March. There wasn’t much impact from Boeing warning that it will likely have to reduce deliveries of its 737 Max plane owing to part issues, although the company noted that the problems caused are not an “immediate safety of flight issue and the in-service fleet can continue operating safely.”

GOLD: Gold Holds Just Below Cycle Highs, Supported By Weaker USD In Asia

The softer USD narrative in Asia-Pac hours supported bullion, pushing spot back towards Thursday’s cycle highs, last dealing +$5/oz at ~$2,045/oz. A breach of yesterday’s cycle high ($2,048.7/oz) would expose the March ’22 highs, which protect the all-time high from ’20. The Fed pivot narrative continues to dominate when it comes to support for bullion, with the softer USD fuelling the bid in gold, although our weighted U.S. real yield monitor has ticked away from its multi-month trough in recent days. When it comes to flows, known ETF holdings of gold now sit at the highest level observed since late January, after bouncing from cycle lows registered around the time of the well-documented U.S. banking tumult observed in March.

OIL: On Track For A Fourth Straight Weekly Gain

Oil looked to a softer USD for some light support in Asia-Pac hours, with WTI & Brent crude futures adding ~$0.35 apiece after Thursday’s downtick (in the wake of the notable rally from cycle lows observed in recent weeks). In the background, signs of tighter market conditions continue to underpin crude, leaving the major benchmarks on course for a fourth consecutive weekly gain, with news outlets pointing to more than ample demand in physical crude markets across both Europe & Asia. Both Brent & WTI remain in bullish patterns from a technical perspective, with the Jan 23 highs in both providing the major points of nearby technical resistance.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/04/2023 | 0600/0800 | *** |  | SE | Inflation report |

| 14/04/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 14/04/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 14/04/2023 | - |  | EU | ECB Lagarde and Panetta in IMF/World Bank Spring Meetings | |

| 14/04/2023 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/04/2023 | 1230/0830 | *** |  | US | Retail Sales |

| 14/04/2023 | 1230/0830 | ** | | US | Import/Export Price Index |

| 14/04/2023 | 1245/0845 | | US | Fed Governor Christopher Waller | |

| 14/04/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 14/04/2023 | 1315/0915 | *** | | US | Industrial Production |

| 14/04/2023 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/04/2023 | 1400/1000 | * | | US | Business Inventories |

| 14/04/2023 | 1600/1700 |  | UK | BOE Tenreyro Panellist at the IMF Meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.