Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

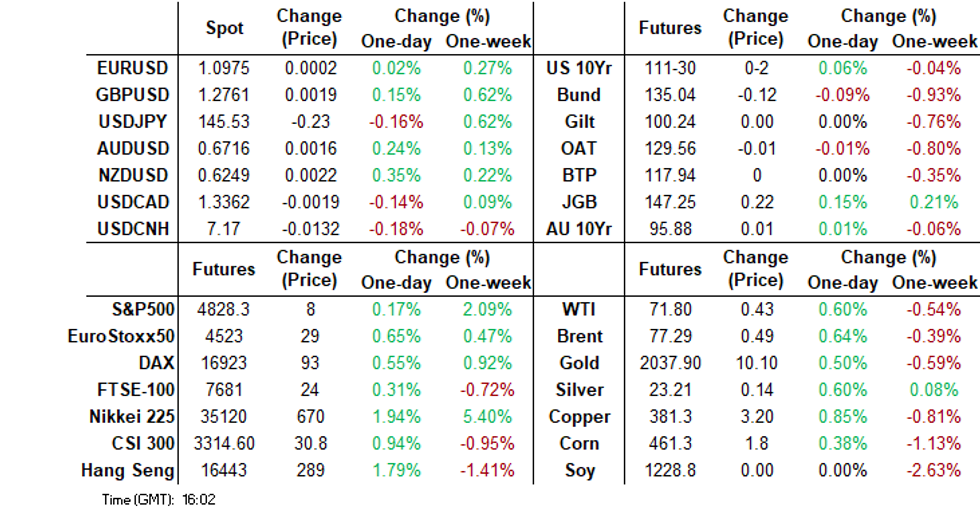

- Positive risk appetite has been most evident in the equity space so far today. Gains have been broad base, with HK and China markets showing a decent rebound. This has curbed USD appetite, with the BBDXY off 0.20% and most Asian currencies higher.

- US yields are down a touch as US CPI comes into view.

- The BOK left rates unchanged as expected and removed its tightening bias. Rate cuts are unlikely within 6 months though according to Governor Rhee.

- Looking ahead the Thursday session will be dominated the US CPI outcome.

MARKETS

US TSYS: Cash Bonds Dealing Little Changed, Markets Await US CPI

TYH4 is trading at 111-28+, 0-00+ from NY closing levels.

- With little in the way of meaningful newsflow, cash US tsys are dealing little changed in today’s Asia-Pac session ahead of the US CPI data release later today.

- Consensus puts core CPI inflation at 0.3% m/m in December, with risk seen to the downside. If analysts are correct, supercore trend rates are likely to remain very strong at 4% annualised handles but treat with some caution as differences in methodology have seen core PCE at notably weaker rates in recent months. (see MNI’s US CPI Preview here)

STIR: $-Bloc Prices An Aggressive Easing Cycle Ahead Of US CPI Data

STIR markets within the $-bloc remain poised for a significant easing cycle in 2024 ahead of today’s US CPI release.

- Consensus puts core CPI inflation at 0.3% M/M in December, with risk seen to the downside. (see MNI’s US CPI Preview here)

- The US and Canada remain the only $-bloc markets with expectations of a greater than 100bp reduction in policy rates by year-end.

- Australia stands out as an outlier, with less than two 25bp cuts factored in by December 2024.

- December 2024 expectations and the cumulative easing across the $-bloc stand at: 3.90%, -143bps (FOMC); 3.84%, -117bps (BOC); 3.89%, -45bps (RBA); and 4.59%, -92bps (RBNZ).

Source: MNI – Market News / Bloomberg

JGBS: Futures At Session Highs Ahead OF US CPI Data, 30Y Supply Tomorrow

JGB futures are higher, +23 compared to the settlement levels, and at session highs.

- There hasn’t been much in the way of domestic drivers to flag given the relatively light local calendar. Leading & Coincident Indices are due later but are unlikely to be market movers.

- OECD urges Japan's central bank to gradually raise interest rates – Reuters.

- Asian participants have opted to remain on the sidelines concerning US tsys in anticipation of the pivotal US CPI data scheduled for later today. As a result, cash US tsys have experienced minimal changes during today's Asia-Pacific session. This cautious stance suggests a wait-and-see approach among Asian investors, highlighting the significance they place on the upcoming US CPI data and its potential impact on market dynamics.

- Cash JGBs are dealing mixed. The benchmark 10-year yield is 0.4bp lower at 0.582% versus a session high of 0.628%.

- The swap curve has slightly twist-steepened, with rates 0.1bp lower to 1bp higher. Swap spreads are wider.

- Tomorrow, the local calendar sees Weekly International Investment Flows, BoP Current Account Balance and Bank Lending data.

- The MoF will tomorrow sell Y900bn 30-year JGBs.

AUSSIE BONDS: Local Participants On The Sidelines Ahead Of US CPI Data

ACGBs (YM -2.0 & XM -2.0) show a slight weakening following a subdued trading session, ahead of crucial US CPI data later today. The domestic market lacked significant catalysts, with the previously highlighted trade balance data failing to have a substantial impact on market movements.

- Asian participants, too, have demonstrated a cautious approach to US tsys, opting to remain on the sidelines. This has resulted in minimal changes in cash US tsys during today's Asia-Pacific session.

- Cash ACGBs are 1-2bps cheaper, with the AU-US 10-year yield differential 1bp wider at +11bps.

- Swap rates are 2-3bps higher, with EFPs slightly wider.

- The bills strip has slightly bear-steepened, with pricing flat to -4.

- RBA-dated OIS pricing is flat to 3bps firmer across meetings, with December leading. A cumulative 51bps of easing is priced by year-end.

- Tomorrow, the local calendar is relatively light, with Home Loans data as the sole release.

AUSTRALIAN DATA: Trade Surplus Surges On Weaker Consumer Good Imports

The November trade data saw a healthy rise in the trade surplus to A$11.4bn, versus A$7.3bn expected. Exports rose 1.7% m/m (prior 0.8%), while imports fell -7.9% m/m (prior -2.9%).

- On the export side, commodity exports were mixed. Iron ore down 1.1% m/m, along with natural gas (-2.6%). However, coal exports rose 8.8% m/m. Agricultural exports were also a touch higher (0.3% m/m).

- On the import side, we saw a 14%m/m drop in consumer imports, while capital imports were down nearly 3%.

- This hints at a softer domestic demand backdrop, although the levels of imports are coming off elevated levels seen at the end of Q3. Also note retail sales data for Nov, from earlier in the week, was still firm.

NZGBS: Little Changed, Narrow Ranges, Awaiting US CPI

NZGBs closed flat to 1bp cheaper across benchmarks after dealing in relatively narrow ranges for today’s local session. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined homebuilding approvals for November.

- With US CPI due later today, local participants have been content to stay on the sidelines, especially with cash US tsys trading little changed in today’s Asia-Pac session.

- Consensus puts core CPI inflation at 0.3% m/m in December, with risk seen to the downside. If analysts are correct, supercore trend rates are likely to remain very strong at 4% annualised handles but treat with some caution as differences in methodology have seen core PCE at notably weaker rates in recent months. (see MNI’s US CPI Preview here)

- Swap rates closed 4-5bps higher, with implied swap spreads ~3bps wider.

- RBNZ dated OIS pricing closed unchanged across meetings. A cumulative easing of 92bps is priced by year-end.

- Tomorrow, the local calendar is once again empty.

FOREX: USD Loses Ground Amidst Firmer Equity Backdrop

USD loses have extended as the Asia Pac session has progressed. The BBDXY sits 0.20% lower, last near 1223.50. A better risk on tone from equities, with Asia Pac markets higher and US futures ticking up, has weighed on USD sentiment. US yields are little changed as the CPI print comes into view.

- NZD and AUD have outperformed, consistent with the risk on theme, although JPY is not far behind.

- NZD/USD is up nearly 0.40% to 0.6250, but we remain comfortably within recent ranges. Earlier data showed Nov building permits down over 10%m/m, but this followed a strong Oct rise.

- AUD/USD is up +0.30%, last in the 0.6720/25 region. The Nov trade surplus surged thanks to a lower import bill as consumer imports slumped.

- USD/JPY sits in the 145.30/35 region, around 0.30% stronger in yen terms. Lows for the session rest at 145.29. The OECD sees scope for the BOJ to adjust away from ultra easing settings, with wages growth expected to keep inflation close to the BoJ target.

- All eyes in the US session will be on the CPI release.

EQUITIES: Major Indices Tracking Higher, Japan Benchmarks Still Outperforming

The major regional equity indices are all tracking higher, with some pockets of weakness in SEA. We had a positive lead from US cash trading on Wednesday, while US futures have also firmed in the first part of Thursday trade. Nasdaq futures are outperforming, up 0.35%, and the active contract is back above 17000. Eminis are up 0.19% at this stage, near 4829.

- Japan markets once again remain the standout. The Nikkei 225 is tracking nearly 2% firmer at this stage, after posting a similar gain yesterday. The Topix is trailing slightly at +1.7%.

- A modest yen recovery hasn't dampened sentiment, although the yen has only pared Wednesday losses modestly. The electric appliances sector has led the way again.

- Hong Kong markets are much stronger to the lunch time break, +1.51% for the HSI. The beaten up tech sub sector is up 1.83% to the break.

- China mainland indices are higher, but only modestly. At the break, the CSI 300 is up 0.29%.

- The Kospi and Taiex indices are modestly higher at this stage, but still underperforming Japan gains.

- In SEA, Malaysia and Thailand markets are weaker, while modest gains are evident elsewhere.

OIL: Benchmarks Recoup Some Of Wednesday's Fall, But Still Down For The Week

Oil benchmarks sit marginally above Wednesday session lows. Front month Brent was last near $77.10/bbl, while WTI was near $71.65/bbl. This is a gain of around 0.40%, but only partially offsets the more than 1% drop recorded for Wednesday's session. Moreover, we remain below end Friday levels from last week as well.

- Wednesday's move lower was driven by an unexpected build in US crude stocks. EIA Weekly US Petroleum Summary - w/w change week ending Jan 05: Crude stocks +1,338 vs Exp -199, Crude production 0, SPR stocks +606, Cushing stocks -506.

- Market expectations had been skewed the other way and the stock build helped offset renewed concerns around Red Sea tensions.

- Today's gain is in line with a slightly better risk appetite tone, with Asia Pac and US equity futures rising, while the USD has also been softer.

GOLD: Slightly Stronger Ahead Of US CPI Data

Gold is 0.3% higher in the Asia-Pac session ahead of US CPI data later today, after closing 0.3% lower at $2024.41 on Wednesday.

- Bullion was initially supported on Wednesday by geopolitical risks before fading into NY session close despite a softer USD index.

- Investors were possibly gearing up for turbulent trading following the release of US CPI data, which may firm views on when the Fed will start easing monetary policy.

- Cash US Treasuries are dealing little changed in today’s Asia-Pac session after cheapening slightly on Wednesday.

- Economists polled by Bloomberg expect core inflation to fall to 3.8% y/y in December from 4% prior.

- From a technical standpoint, the yellow metal approached support at the 50-day EMA of $2012.8 on Wednesday.

BOK: Reference To Further Rate Hikes Removed, But Policy To Stay Restrictive

The BoK statement, which accompanied its on hold decision, removed the reference to judging whether rates needed to be raised further. At the same time though the central bank stated that it would keep policy restrictive for a sufficiently long period to ensure that inflation returns to target.

- Other highlights from the statement included: the inflation slowdown is likely to moderate from here and fluctuate around 3% for some time (they have a 2.6% forecast for 2024). Core inflation is expected to continue to ease modestly.

- GDP growth is seen broadly in line with what was expected in November (2.1% for 2024). Consumption and construction investment are expected to recover slowly, with exports remaining the lead at this stage.

- Risks were highlighted in the real estate project finance sector.

- We now wait for BoK Governor Rhee's press conference. The central bank is clearly done with rate hikes, but a shift to rate cuts may still be at least quite a few months away.

SOUTH KOREA: Early January Export Data Up 11.2% Y/Y

The first 10-days of January trade data for South Korea showed further improving trends for export growth.

- We were up 11.2%y/y terms and there was no difference with the daily average print. Chip exports were +25.6%, car exports +2.2%. By country exports to China rose 10.1% and remained firmed to the US, +15.3%.

- Note full month exports for Dec were up 5.1% in y/y terms.

- Imports for the first 10-days were down -8.3% y/y. The trade deficit was still just over $3bn, but this tends to improve as the full month progresses.

ASIA FX: KRW and CNH Enjoy Positive Spill Over From Equity Gains

USD/Asia pairs are mostly lower, albeit to varying degrees. Positive spillover from regional equity gains is evident. USD/CNH is back sub 7.1700, while 1 month USD/KRW is back to the 1312 handle. PHP has also had its first gain in 5 sessions. Gains have been less evident elsewhere, with the upcoming US CPI print likely providing some caution. Tomorrow the main focus will be on China Dec inflation data, while Dec trade figures are also out.

- China equities are finally seeing some positive gains, the CSI 300 up nearly 1%, with surging HK markets (HSI +2%) helping. This is amidst broader regional gains and positive US futures. USD/CNH is back sub 7.1700 after opening above 7.1830. The USD/CNY fixing error widened as well.

- 1 month USD/KRW is tracking lower, last near 1312, around 0.40% stronger in won terms. Positive spill over from equity gains has been evident, along with lower USD levels against the G10. Still, offshore investors have sold a chunky -$352.5mn of local shares. The BoK held rates steady as expected. The implicit tightening bias was removed, but Governor Rhee stated rates cuts within 6 months was unlikely.

- USD/THB is a touch higher, but continues to find selling interest above 35.00. Comments late yesterday from Pm Srettha around BoT's independence have likely aided sentiment and reduced fears of a near term policy shift. On the data front, consumer confidence continues to improve, up to 62 from 60.9, which is highs back to early 2020.

- PHP is tracking higher for the first time in 5 sessions. USD/PHP is back near 56.10, after Wednesday highs near 56.40. Higher onshore equities (+1.2%), and lower oil prices are likely helping Peso sentiment at the margins.

- USD/IDR is relatively steady, last little changed at 15560/65, with the 1 month NDF slightly higher. The rupiah is not enjoying positive spill over from stronger equities seen in the region so far today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/01/2024 | 0800/0900 | ** |  | ES | Industrial Production |

| 11/01/2024 | 0900/1000 | * |  | IT | Industrial Production |

| 11/01/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 11/01/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 11/01/2024 | 1330/0830 | *** | | US | CPI |

| 11/01/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 11/01/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 11/01/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 11/01/2024 | 1740/1240 | | US | Richmond Fed's Tom Barkin | |

| 11/01/2024 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 11/01/2024 | 1900/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.