Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

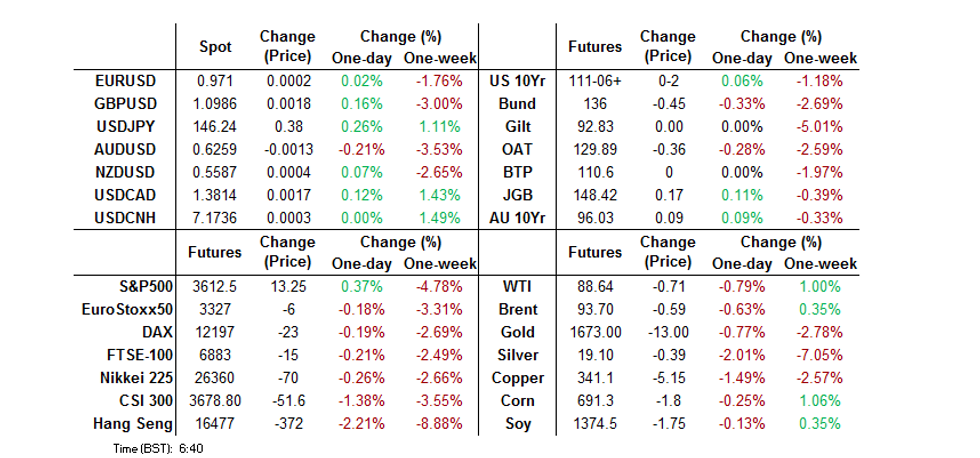

- Asia-Pac trade saw a spike higher in GBP FX crosses as the Financial Times reported that “the Bank of England has signalled privately to bankers that it could extend its emergency bond-buying programme past this Friday’s deadline," clouding guidance given BoE Governor Bailey less than 12 hours before. The initial move has largely pared, with policy uncertainty and a can kicking mentality paring seeing the GBP off of best levels.

- USD/JPY crossed above the previous intervention zone, registering a fresh multi-decade high in the process.

- Notable data releases today include UK economic activity indicators & Eurozone industrial output. Plenty of speeches are scheduled from Fed, ECB & BoE policymakers, with the minutes from the most recent FOMC meeting also due.

US TSYS: BoE Bond Buying Speculation Dominates

Cash Tsys run 1-2bp richer across the curve into London hours, with the belly leading the bid, while TYZ2 is +0-03 at 111-07+, hovering around the middle of its 0-14 overnight range on volume of ~105K (~40K of which changed hands in the last hour or so).

- The uptick in volume came as the space firmed on an FT source report suggesting that the BoE could extend its temporary Gilt purchases beyond the current Friday deadline (despite comments to the contrary from BoE Governor Bailey on Tuesday), with the Bank reportedly focused on the cash reserves of LDI pension funds in respect to potential margin call requirements.

- Still, it would seem that market participants are taking this as a case of kicking the can down the road, given the “temporary” nature of the already deployed, but ever evolving, BoE purchase scheme. This leaves the space off of richest levels at typing.

- 4x block sales of FV futures (-3.4K apiece) provided the highlight on the flow side before the FT story hit.

- Gilt gyrations will set the tone in pre-NY dealing. Further out, Wednesday’s local docket includes the minutes from the latest FOMC meeting, 10-Year Tsy supply and Fedspeak from Bowman, Barr & Kashkari. Although Thursday’s CPI print is of more interest.

JGBS: Curve Steepens, With Broader Core FI Bid Doing Little For Super-Long End

The curve was under early Tokyo steepening pressure as participants made room for this afternoon’s 30-Year JGB supply and reacted to Tuesday’s comments from BoE’s Bailey.

- It was a less than convincing round of 30-Year JGB supply which saw the tail widen notably, low price miss broader expectations and the lowest cover ratio seen at a 30-Year auction seen since March ’21.

- It would seem that ongoing market vol., the relative lack of BoJ control over this area of the curve and worry surrounding further cheapening in wider core global FI markets deterred bidders from stepping up.

- The previously flagged FT sources piece re: a potential extension of the BoE’s temporary bond buying scheme then allowed the space to firm into the bell, leaving JGB futures +15 at typing, off best levels, although the contract was fairly resilient when compared to the rest of the JGB space throughout the duration of Tokyo trade.

- Cash JGB trade sees the major benchmarks run 1.5bp richer to 5bp cheaper, with 7s outperforming on the bid in futures and super-long paper still lagging on the day.

- Note that domestic headline flow was dominated by familiar rhetoric from Japanese officials re: FX intervention matters as USD/JPY registered a fresh multi-decade high, breaching September’s intervention zone.

- Tomorrow’s domestic docket is headline by PPI data.

AUSSIE BONDS: Firmer Throughout Sydney Trade

YM & XM operate off of best levels after the previously alluded to FT sources piece re: a potential extension of the BoE’s temporary bond purchase scheme allowed both contracts to briefly show through their respective overnight peaks. That leaves YM +6.5 & XM +8.0, with a fairly parallel 7-8bp of richening seen across the wider cash curve.

- There was little in the way of idiosyncratic news flow to drive the space, with comments from RBA Assistant Governor (Economic) Ellis providing a little bit more detail into the RBA’s thought process surrounding the idea of the neutral cash rate, albeit with little meaningful deviation from Governor Lowe’s previous musings and a continued insistence that the concept of a neutral rate acts more as a guide than as a required hard outcome for the Bank. The lack of hawkish surprises on this front allowed a slight bid to develop.

- A firm round of pricing in the latest round of ACGB Nov-32 supply provided little impetus for the wider ACGB space.

- Bills sit 4-8bp richer through the reds, with a terminal rate of just under 4.00% observed in RBA dated OIS, little changed on the day.

- Looking ahead., consumer inflation expectations data headlines Thursday’s domestic docket.

NZGBS: Bailey-Related Pressure & LGFA Bond Pricing Weigh On NZGBs

NZGBs cheapened on Wednesday, with the major benchmark yields running 5-6bp higher on the day, in lieu of Tuesday’s bear steepening of the U.S. Tsy curve which was aided by comments from BoE Governor Bailey, who pointed to the already outlined end to the BoE’s temporary Gilt purchases as a hard deadline (a subsequent FT story has drawn questions over that idea, but that came after the NZGB market closed).

- 2-Year swap rates hit a fresh cycle high before edging away from best levels.

- Pricing of the latest round of bond issuance from LGFA (’25 & ’29 paper) likely applied some background pressure to NZGBs.

- Note that the RBNZ showed little want to adjust its 1-3% inflation target band during the initial stages of the latest review of its monetary policy remit, although it will consult on the matter ahead of the final publication.

- RBNZ dated OIS indicate a terminal rate of just over 4.90%, little changed on the day.

- Local data was headlined by the latest REINZ house price readings, which revealed the continued impact of higher interest rates on the housing market (lower prices and reduced sales).

- Looking ahead, Thursday’s domestic docket will be headlined by the latest round of NZGB supply (which includes NZGB Apr-25, May-32 & May-41), with the latest food price index readings also due.

FOREX: GBP Bid On BoE Readiness To Extend Bond-Buying, USD/JPY Past Prior Intervention Levels

Yen sellers forced their way through the pivotal Y145.90 level against the greenback, printed on Sep 22 when Japanese officials intervened in currency markets and re-tested yesterday. The initial foray above that figure was short-lived, but the rate posted another upleg at the Tokyo open. It continued to trade with bullish bias, despite the generally limited headline flow, touching a fresh 24-year high at Y146.39. USD/JPY 1-week implied volatility climbed to a two-week high.

- The move through Y145.90 put market participants on intervention watch. Officials stuck to their regular script, pledging to monitor FX moves with heightened urgency and take appropriate measures against excessive volatility. On the other hand, FinMin Suzuki suggested that the focus is on the speed of the moves rather than any specific levels.

- Early gains for the broader U.S. dollar facilitated the upswing in USD/JPY, albeit the BBDXY index pulled back into negative territory ahead of the London session. The U.S. data docket for the next two days includes a couple of key risk events, namely FOMC minutes (Wednesday) and CPI report (Thursday).

- Renewed greenback losses were driven by a spike in sterling crosses as the Financial Times reported that “the Bank of England has signalled privately to bankers that it could extend its emergency bond-buying programme past this Friday’s deadline."

- Further weakness in iron ore sapped some strength from the Aussie dollar. AUD/USD printed new cyclical lows at $0.6240.

- Other notable data releases today include UK economic activity indicators & EZ industrial output. Plenty of speeches are scheduled from Fed, ECB & BoE policymakers.

ASIA FX: Won Leads Gains After BoK Flags FX Concerns, Rupiah & Ringgit Falter

The Bloomberg/J.P. Morgan Asia Dollar Index (ADXY) hovered near cyclical lows as cautious mood remained amid familiar concerns surrounding global growth prospects. The Asia EM space got some reprieve as we approached the Asia/Europe crossover, with the USD erasing its earlier gains on the back of an FT source report suggesting that the Bank of England has privately communicated to bankers that it could extend its emergency bond-buying scheme past this Friday's deadline.

- USD/CNH ground higher in early trade, ignoring the 30th consecutive firmer-than-expected yuan fixing, with the divergence from sell-side expectations widening to ~650bp. Participants scrutinised the PBOC's statement from yesterday, where officials said "the yuan will achieve equilibrium by itself as supply and demand plays a decisive role." The late-doors dip in the greenback drove USD/CNH into negative territory.

- The South Korean won outperformed its peers in emerging Asia. Spot USD/KRW dipped as BoK Gov Rhee said FX developments were one of the main reasons for the central bank's decision to raise the key policy rate by the expected 50bp increment today. Worth noting that there were two dovish dissenters, which makes it the first split vote since August 2021.

- The currencies of top palm oil exporters (IDR and MYR) were among the worst performers in the region, even as the tropical oil clawed back some of its yesterday's losses. Weakness in the broader commodity complex may have weighed on those currencies. Separately, Indonesian FinMin Indrawati warned of a "hurricane" of risks facing EMs.

- Spot USD/PHP kept testing record highs. The Bankers Association of the Philippines issued a statement, where lenders vowed to cooperate with Bangko Sentral ng Pilipinas in curbing speculation in the FX market.

- Spot USD/THB trimmed its initial gains as Thailand's consumer confidence climbed to an 8-month high. The minutes from the BoT's September monetary policy meeting flagged elevated risks to the inflation outlook.

EQUITIES: E-Minis Tick Higher On BoE Hope, Chinese Tech Continues To Struggle

The 3 major e-mini futures contracts have added ~0.5% vs. Tuesday’s closing levels in lieu of an FT source story flagging the potential for an extension of the BoE’s temporary Gilt buying scheme, pushing back against the idea of a hard pre-weekend cessation.

- Wider Asia-Pac equities had struggled on the negative lead from Wall St., which was tied to comments from BoE Governor Bailey, after he stressed that the BoE would pullback from Gilt purchases after the upcoming weekend.

- Continued focus on China’s ZCS policy applied further weight to the major indices in China & Hong Kong.

- Continued worry re: Sino-U.S. tensions surrounding the tech sphere added a further (constant) leg of weakness to Chinese tech names,

- The ASX 200 & Nikkei 225 looked to the FT source report for support, registering very modest net gains on the day in lieu of the release.

OIL: Prices Retreating In Face Of Gloomier Demand Outlook

Oil prices continued to unwind their gains from last week after OPEC+ announced production cuts, because of a weakening demand outlook. WTI is down 0.8% from its close to be trading below $89/bbl and approaching its 50-day MA, while Brent is -0.6%, but both are off of their session lows.

- Last week’s supply concerns have been overtaken by worries about the global economy as the IMF revised down its GDP forecasts and Biden stated that a “slight recession” was possible. China’s assertion that its “Zero-covid policy” is the best way to face the virus, has added to expectations that global oil demand will weaken.

- Biden reiterated his anger at Saudi Arabia for agreeing to the OPEC+ cuts and stated that the US will be revisiting its relationship with the major oil producer.

- OPEC, the International Energy Agency and US Energy Information Administration are all scheduled to release outlooks this week. A downward revision to demand expectations is likely to put further pressure on prices.

- US data remain the focus of the week with the September PPI out today as well as the FOMC minutes followed by the CPI on Thursday.

GOLD: Coiling In Asia

Spot gold has stuck to a narrow range in Asia-Pac dealing, last printing little changed at ~$1,665/oz, after a firmer dollar and push higher in Tsy yields weighed on gold into Tuesday’s close. That move came in lieu of BoE Governor Bailey confirming the already scheduled withdrawal of the Bank’s temporary Gilt purchases.

- U.S. real yields and the broader DXY continue to operate within their recent ranges, after shunting higher during ’22.

- A lack of macro headline flow has made for subdued Asia-Pac dealing, with bears remaining focused on the cycle low at $1,615.0/oz, with the 3 Oct low ($1,659.7/oz) providing immediate intermediate support.

- U.S. CPI data (due Thursday) provides the key macro risk event this week, with U.S. PPI & the minutes from the latest FOMC meeting (both due Wednesday) also eyed.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/10/2022 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 12/10/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/10/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 12/10/2022 | 0600/0700 | *** | | UK | Index of Production |

| 12/10/2022 | 0600/0700 | ** | | UK | Index of Services |

| 12/10/2022 | 0800/0900 | | UK | BOE Haskel Keynote Speech at The Productivity Institute | |

| 12/10/2022 | 0900/1100 | ** |  | EU | Industrial Production |

| 12/10/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/10/2022 | 0930/1030 | | UK | BOE FPC Sept 30 meet minutes | |

| 12/10/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/10/2022 | 1135/1235 | | UK | BOE Pill in Conversation with SCDI | |

| 12/10/2022 | - | | EU | ECB Lagarde & Panetta IMF/World Bank Annual Meetings | |

| 12/10/2022 | 1230/0830 | *** | | US | PPI |

| 12/10/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 12/10/2022 | 1330/1530 | | EU | ECB Lagarde in Conversation with Tim Adams (IIF) | |

| 12/10/2022 | 1400/1000 | | US | Minneapolis Fed's Neel Kashkari | |

| 12/10/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/10/2022 | 1700/1800 | | UK | BOE Mann Canadian Association for Economics Webinar | |

| 12/10/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 12/10/2022 | 1745/1345 | | US | Fed Vice Chair Michael Barr | |

| 12/10/2022 | 2230/1830 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.