Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

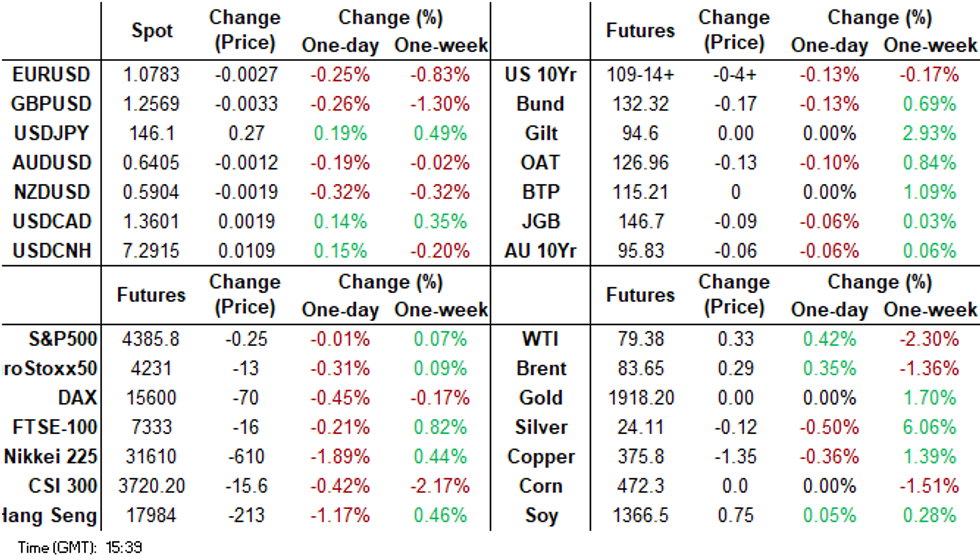

- The greenback has firmed in the Asian session on Friday as Fed Chair Powell's speech this evening comes into view. The greenback has moderately extended gains seen in Thursday's trading, the BBDXY last near 1244.60, +0.20%. EUR/USD is back sub its 200-day MA for the first time since November last year.

- Regional equities are weaker across the board, which has likely helped USD sentiment. China authorities are looking to boost sentiment, aiming to meet with large offshore fund managers in Hong Kong.

- Elsewhere, cash tsys sit little changed across the major benchmarks. In Japan the benchmark 10-year yield is unchanged at 0.656%, after mixed Tokyo CPI data. In the commodity space, oil is showing resilience, although still tracking lower for the week. Metals are modestly weaker.

- Looking ahead, the final read of German Q2 GDP is the highlight in Europe, further out the aforementioned Fedpeak from Powell headlines today's docket.

MARKETS

US TSYS: Narrow Ranges In Asia, Powell In View

TYU3 deals at 109-15, -0-04, a 0-05+ range has been observed on volume of ~120k.

- Cash tsys sit little changed across the major benchmarks.

- Tsys firmed in early dealing, there was no obvious headline driver, as perhaps local participants used Thursday's cheapening as an opportunity to close short positions ahead of Fed Chair Powell's Jackson Hole speech.

- There was little follow through on the moves higher and tsys pared gains to sit in a narrow range for the remainder of the session.

- FOMC Dated OIS price a terminal rate of ~5.45%, there are ~60bps of cuts priced to July 2024.

- There is a thin docket in Europe today, Further out the aforementioned speech from Fed Chair Powell headlines, US University of Michigan consumer sentiment also crosses.

STIR: $-Bloc Terminal Rate Expectations Steady Ahead Of Fed Chair Powell’s JH Speech

Terminal rate expectations across the $-bloc are steady ahead of the keenly anticipated address by Fed Chair Powell at the Jackon Hole Symposium. As of now, terminal rate expectations and the aggregate tightening stand at:

- 5.47%, +14bp (FOMC);

- 5.21%, +21bp (BoC);

- 4.19%, +12bp (RBA); and

- 5.65%, +15bp (RBNZ).

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

JGBS: Futures Pare Losses In The Tokyo Afternoon, Eyeing US Tsys Ahead Of JH Speeches

In the Tokyo afternoon session, JGB futures slightly pared losses, -7 compared to settlement levels, after dealing in a relatively narrow range in the morning session.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Tokyo CPI for August, which was a touch below expectations in terms of the headline and ex-fresh fruit measures.

- Accordingly, local participants have likely been on headlines and US tsys watch ahead of the keenly anticipated address by Fed Chair Powell at the Jackon Hole Symposium.

- US tsys are sitting little changed in Asia-Pac trade. The ranges have been relatively narrow, with the proximity to Fed Chair Powell's speech today a limiting factor.

- Cash JGBs are mixed across the curve, with yield movements bounded by -1.2bp (20-year) and +0.2bp (the futures-linked 7-year). The benchmark 10-year yield is unchanged at 0.656%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- Swap rates are mixed across the curve, with the belly underperforming. Swap spreads are narrower, part from the 40-year.

- Early next week, the local calendar sees June Leading and Coincident Indices on Monday and July Jobless Rate data on Tuesday.

- On Tuesday, the MoF plans to sell Y2.9tn of 2-year JGBs.

JAPAN DATA: Tokyo Headline CPI Moderates Further, Core/Services Inflation Proving To Be Stickier

Tokyo August CPI was a touch below expectations in terms of the headline. We printed at 2.9% y/y, versus 3.0% projected and 3.2% prior. The ex fresh food measure also came in below expectations at 2.8% y/y (2.9% forecast and 3.0% prior). The headline measures are largely evolving as expected, now comfortably off early 2023 peaks (4.4% y/y for headline). The ex fresh-food, energy measure was in line with consensus though at 4.0% y/y, which was also the prior outcome and remains at cyclical highs. The core measure which strips out all food and energy ticked higher to 2.6% y/y from 2.5% in July.

- In m/m terms, we were +0.1% (seasonally adjusted), while ex fresh-food we were 0.2% m/m (prior 0.2%), while ex fresh food and energy printed at 0.3% m/m (prior 0.4%). The ex food and energy m/m print was 0.4%, similar to last month's 0.5%.

- Looking at the sub-sectors, fresh food -1.3%, utilities -3.5% and household goods -0.4% were the main disinflationary forces. Offsets came from entertainment +2.1% and transport, communication +0.8%.

- In y/y terms, outside of utilities -15.0%, the sub-sectors maintained firm y/y momentum for the most part. Entertainment +5.7%, and transport, communication +3.6%, are likely to remains BoJ watch points in terms sticky to firmer services related inflation pressures.

AUSSIE BONDS: At Session Cheaps Ahead Of Fed Chair Powell’s JH Speech

ACGBs (YM -5.0 & XM -5.5) are weaker and near Sydney session lows. With the domestic data docket empty today, local participants have likely been on headlines and US tsys watch ahead of Fed Chair Powell's speech this evening (1505 BST / 0005 AEST) at the Jackson Hole Symposium.

- Aussie 10-year futures are trading above recent lows. Nonetheless, the break of support at 95.685, the Jul 10 low would reinforce a bearish theme, according to MNI’s technicals team.

- US tsys are sitting little changed in Asia-Pac trade. The ranges have been relatively narrow, with the proximity to Fed Chair Powell's speech today a limiting factor.

- Cash ACGBs are 4-5bp cheaper with the AU-US 10-year yield differential -1bp at -8bp.

- Swap rates are 5bp higher.

- The bills strip has bear-steepened, with pricing -1 to -8.

- RBA-dated OIS pricing is 2-6bp firmer for '24 meetings. A 6% chance of a 25bp hike is priced for September.

- Next week, the local calendar sees Retail Sales for July on Monday, ahead of RBA Governor Elect Bullock’s speech on Tuesday. On Wednesday, the CPI Monthly for July is on tap, with Construction Work Done (Q2), Building Approvals (Jul) and Private Sector Credit (Jul).

NZGBS: Closed On A Weak Note Ahead Of Jackson Hole Speeches

NZGBs closed at session cheaps, with benchmark yields 4-5bp higher. Without domestic drivers, local participants likely eyed headlines and US tsys ahead of the keenly anticipated address by Fed Chair Powell at the Jackon Hole Symposium.

- US tsys are sitting little changed in Asia-Pac trade. The ranges have been narrow, with the proximity to Fed Chair Powell's speech today a limiting factor.

- Swap rates are 3-5bp higher, with implied swap spreads little changed.

- RBNZ dated OIS pricing is 1-3bp firmer for meetings beyond October. Terminal OCR expectations sit at 5.65%.

- Bloomberg reports that ANZ Bank says China’s slowing economy could help curb NZ inflation, and may allow the RBNZ to avoid another interest rate hike, according to a weekly report. Nevertheless, ANZ maintains the view that a 25bp hike is needed in November. (See link)

- Next week the local calendar is empty until Building Permits on Wednesday and ANZ Business Confidence on Thursday.

- Next Thursday the NZ Treasury plans to sell NZ$225mn of the 0.25% May-28 bond, NZ$175mn of the 1.5% May-31 bond and NZ$100mn of the 1.75% May-41 bond.

AU/NZ BONDS: AU-NZ 10Y Differential Back In The Bottom Half Of The Range

Today, the 10-year NZGB benchmark has experienced a 4bp increase in yield, aligning with the sell-off in ACGBs. Consequently, the AU-NZ 10-year yield differential remains unchanged at -85bp.

- However, a broader historical perspective unveils a noteworthy underperformance by NZGBs since mid-June. This has positioned the AU-NZ 10-year yield differential within the lower half of the -40bp to -100bp range it has traded in this year.

- In mid-March, the AU-NZ 10-year yield differential reached a concerning -100bp, marking its lowest level since the late 1990s. This sharp decline was triggered by a disappointing deterioration in NZ's current account deficit, which caught the attention of S&P bond ratings, leading to consequential comments from them.

- After this occurrence, the shifts in the AU-NZ 10-year differential can largely be attributed to market perceptions of the expected policy rate trajectories of the RBA and the RBNZ.

- For instance, between March to June, the market reflected expectations of the RBA catching up to the rate hikes that the RBNZ had already executed. This was evidenced by the AU-NZ 1Y3M swap differential moving from -175bp to -75bp over this interval.

- With both the RBA and the RBNZ currently holding their policies steady, the 1Y3M swap differential has subsequently eased back to -128bp versus the official rate differential of -140bp.

Figure 1: AU/NZ 10-Year Yield Differential Vs. 1Y3M Swap Differential

Source: MNI – Market News / Bloomberg

FOREX: USD Firms In Asia, Powell In View

The greenback has firmed in the Asian session on Friday as Fed Chair Powell's speech this evening comes in to view. The greenback has moderately extended gains seen in Thursday's trading, lower regional equities are weighing on sentiment at the margins.

- EUR is pressured, EUR/USD is down ~0.3% and has broken several support levels. ECB's Nagel noted he is yet to make his mind up about the September ECB monetary policy decision. Support now comes in at €1.0767, bull channel base drawn from Mar 15 low, and €1.0733, low from Jun 12. Resistance is at €1.0933, the 20-Day EMA.

- Kiwi is down ~0.3% and sits a touch above YTD lows, bears look to break the low from 21 Aug ($0.5897).

- Yen is a touch pressured, USD/JPY is ~0.1% firmer and sits above the ¥146 handle. The pair has breached Thursday's highs although ranges remain narrow.

- AUD/USD is holding above the $0.64 handle, ranges have been narrow today.

- Elsewhere in the G-10 space GBP is down ~0.3%. The Scandies are also pressured however liquidity is generally poor in Asia.

- Cross asset wise; BBDXY is up ~0.2% and the Hang Seng is down ~1%. US Tsy Yields are little changed across the curve.

- The final read of German Q2 GDP is the highlight in Europe, further out the aforementioned Fedpeak from Powell headlines today's docket.

EQUITIES: Regional Equity Soften Ahead Of Jackson Hole

Regional Asia Pac equities are a sea of red following the negative lead from US and EU markets in Thursday trade. Losses are across the board, while US futures are mixed. Eminis sit a touch higher, last near 4388, while Nasdaq futures are down -0.15% to 14839.50. Markets may also be somewhat cautious ahead of Powell's speech at the Jackson Hole forum later in the US session.

- Hong Kong and China shares are lower to the break. The HSI down ~1%, with the tech index off around 2%. We saw a sharp pull back in US tech sentiment on Thursday.

- The CSI is down close to -0.50%. Brokerages have rallied on reports of lower commission rates for stock trading. This hasn't been enough to drive overall sentiment higher. Morgan Stanley also downgraded its China stock target for 2024 by 14%.

- In Japan, the Topix is down 0.80%, while the Nikkei has fallen ~1.85%. Tech names have weighed on the aggregate indices. The Kospi is off 0.70%, with offshore investors selling -$146.1mn of local shares today. The Taiex is down -1.40%, basically unwinding all of yesterday's gains.

- In SEA markets are weaker, but losses are less than 1%. The Philippines stock gauge down nearly 0.70% to sub 6200, with reports of lower bank lending weighing on the bank sector. The Singapore bourse is one of the few bright spots, last tracking close to flat.

OIL: Tracking Lower For the 2nd Straight Week

Brent crude is modestly higher in the first part of Friday trade. We were last near $83.65/bbl, down slightly from session highs ($83.78/bbl) and after opening at $83.26/bbl. This puts us +0.35% higher for the session to date, building on Thursday's modest 0.2% gain. WTI is near $79.35/bbl, following a similar trajectory to Brent. These trends are outperforming broader risk themes today, with the BBDXY up a further 0.20%, while regional equities are mostly in the red.

- Still, we are tracking lower for the second straight week, Brent off by 1.35% versus closing levels from the end of last week. WTI down 2.3% over the same period.

- Losses this week have been driven by a firmer USD/elevated yield backdrop ahead of the Jackson Hole symposium. Demand concerns out of China haven't helped, while there have also been some signs of greater oil supply from some OPEC members (albeit not core members).

- For Brent, support has been evident in recent sessions around $82/bbl level, which also coincides with the 50-day EMA. The 100-day EMA sits further south near $81/bbl. On the topside the 20-day EMA is around $84/bbl, while the 21 August high sits around $85.85/bbl.

- Outside of the upcoming Jackson Hole symposium (Fri-Sat), next week doesn't deliver many fresh oil specific risk events. Note we get US Q2 GDP on Wednesday and official PMIs from China on Thursday.

GOLD: Treaded Water Ahead Of Fed Chair Powell’s Speech At Jackson Hole

Gold is slightly weaker in the Asia-Pac session, after closing +0.1% at $1916.91 on Thursday. The resilience of bullion was surprising considering the renewed push higher in the USD index and higher US tsy yields.

- Possibly supporting the precious metal was news that the Polish central bank made its largest gold purchase in four years in July, boosting its share to more than a tenth of reserves.

- As a result, gold is on track for its first weekly gain in five ahead of a key speech by Federal Reserve Chair Jerome Powell at the Jackson Hole symposium in Wyoming, where he’s expected to offer clues on the interest-rate outlook.

- Prior to the Jackson Hole symposium, Fedspeak on Thursday conveyed a blend of perspectives. Taking a more hawkish stance, Boston Fed's Collins emphasised the prudence of maintaining elevated rates for an extended duration, underlining the potential necessity for further adjustments. Collins stated, "A preset path may not be conducive; additional increments might be necessary, and we could be on the cusp of a prolonged period of stability."

- Conversely, Philly Fed's Harker indicated to MNI that he leans towards endorsing the maintenance of prevailing interest rates until the conclusion of the year and potentially even beyond.

ASIA FX: USD/Asia Pairs Firm Amid Broad Dollar Gains, Regional Equity Weakness

USD/Asia pairs are higher, amid broad based USD gains (BBDXY +0.20%) and equity losses in the region. USD/CNH is back above 7.2900, while tech sensitive plays have unwound some of yesterday's outperformance. PHP has outperformed at the margins, but isn't too far away from recent lows. On Sunday China industrial profits print for July. Early next week is quiet though from a data standpoint.

- USD/CNH is tracking near session highs (around 7.2945) in recent dealings, last near the 7.2900 level. This puts CNH down around 0.15% for the session so far, in line with the BBDXY's 0.20% gain to date. Additional headwinds have come from a weaker onshore equity tone (the CSI 300 down close to 0.60% at this stage), despite further calls for fund/bank support for local bourses. Earlier headlines crossed from Reuters that the PBoC was asking some banks to limit Southbound Bond Connect outflows in the latest measure to curb potential yuan weakness. The Securities regulator also plans to meet with some of the world's largest fund managers to boost confidence (see this link).

- USD/HKD spot dips remain supported, the pair last near 7.8435, which is close to early June highs at 7.8440. Recent support points have been at 7.8380 yesterday and 7.8400 earlier today. In the USD/HKD outright forward space, the 12 month is still sub 7.7800, last at 7.7785, largely tracking sideways in recent dealings. 6 month is back around 7.8000, also showing waning upside momentum.

- USD/TWD spot has already unwound a good chunk of yesterday's losses, the pair last around 31.825, +0.12% firmer. We are still sub recent highs near 32.00, while yesterday's lows came in close to 31.74. The Taiex is tracking close to 1.35% weaker at this stage, also unwinding a good proportion of yesterday's rally. Broader tech equity sentiment faltered in US trade on Thursday, with the SOX off more than 3%, which has carried over into Asia Pac markets today. Such sentiment is likely to be key for TWD in the near term.

- USD/THB has recovered ground as today's session has progressed. The pair last near 35.14, down slightly from session highs of 35.18. Some of this has reflected catch up with broader USD gains in the past 24 hours, while the July customs trade figures showed a wider than expected deficit at near -$2bn, versus -$1.386bn projected (and a modest $58mn surplus in June). Earlier BoT Governor Suthiwartnarueput spoke on the sidelines of the Jackson Hole symposium in the US, stating the central bank is close to where it wants to be on rates, but it is watching the new government's fiscal stance. Cash handouts and other fiscal measures proposed by new PM Srettha could be inflationary the Governor noted, but it's too early to gauge any potential BoT response.

- USD/PHP is the only USD/Asia pair to be tracking lower in the first part of Friday trade. The pair was last near 56.70, down slightly on closing levels from yesterday. We opened in the 56.85/90 region. The Peso is outperforming generally firmer USD/Asia trends elsewhere and USD strength against the majors. Note though that USD/PHP hasn't been that strongly correlated with broader USD moves this week. USD/PHP is not too far recent highs around 57.00. Recall earlier in the week that Philippines Finance Chief Diokno stated the authorities working assumption on USD/PHP was a 54-57 range. Hence the closer we get to the top end of this range the potential for verbal jaw boning on FX and or actual intervention is likely to rise.

- USD/MYR prints at 4.6515/40, the pair is a touch higher on Friday. The pair sits a touch off its highest level since mid-July as August's gains are consolidated in a narrow range above the 4.65 handle. We sit ~3.2% above the opening levels from Aug 1. There was little reaction to the July CPI print which was a touch softer than expected.

- The SGD NEER (per Goldman Sachs estimates) is marginally softer in early dealing and has ticked away from its highest level since 3 Aug in recent dealing. The measure is ~0.6% below the top of the band. USD/SGD was supported at the 20-Day EMA yesterday and firmed ~0.3% as broader USD trends dominated flows. The pair sits at $1.3570/75, ~0.1% firmer today. In July Industrial Production fell 0.9% Y/Y, stronger than the expected -3.8% Y/Y fall.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/08/2023 | 0600/0800 | *** |  | DE | GDP (f) |

| 25/08/2023 | 0600/0800 | ** |  | SE | Unemployment |

| 25/08/2023 | 0600/0800 | ** | | SE | PPI |

| 25/08/2023 | 0700/0900 | ** |  | ES | PPI |

| 25/08/2023 | 0800/1000 | *** | | DE | IFO Business Climate Index Direction |

| 25/08/2023 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 25/08/2023 | 1400/1000 | ** |  | US | U. Mich. Survey of Consumers |

| 25/08/2023 | 1405/1005 | | US | Fed Chair Powell on economic outlook | |

| 25/08/2023 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 25/08/2023 | 1900/2100 |  | EU | ECB's Lagarde speaks at Jackson Hole |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.