Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

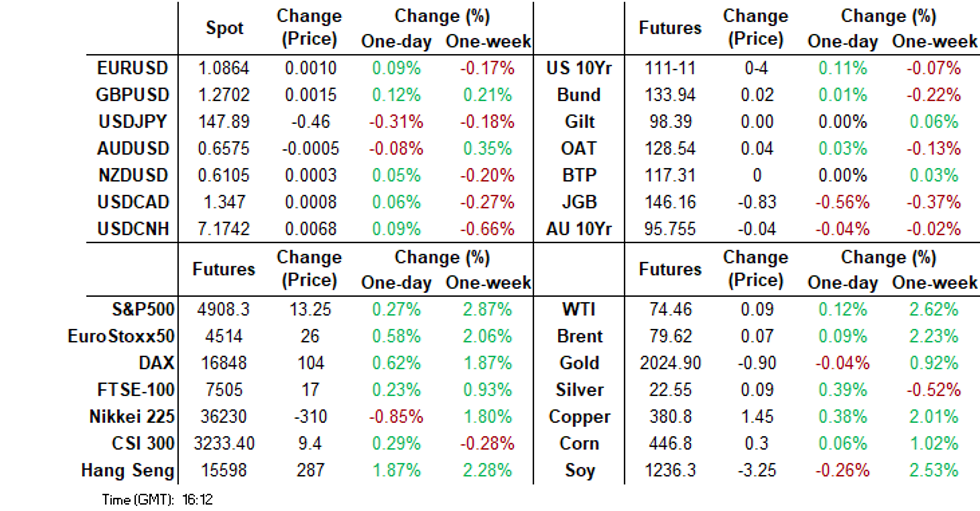

- JGB futures are holding sharply lower but above the session’s worst level, -82 compared to the settlement levels, after traders judged comments from the BoJ on Tuesday to be hawkish. There has been no spill over to US yields though, which sit slightly lower.

- JPY has outperformed in the G10 space, but only marginally. Trends elsewhere have been relatively steady. NZD rallied on stronger domestic price pressure data, but there was no follow through. RBNZ dated OIS pricing closed 3-6bps firmer across meetings beyond February.

- USD/CNH losses have stalled today amid easier funding conditions. China onshore equity sentiment has volatile, but we currently track higher.

- Later preliminary January PMIs for US/Europe are released and the Bank of Canada’s decision is announced.

MARKETS

US TSYS: Tsy Yields Marginally Lower, Ignoring JGB Yield Spike On Potential BoJ Exit

TYH4 is trading at 111-11+, + 04+ from NY closing levels.

- JGB yields rose sharply as traders brought forward bets on BoJ hikes. There was little spill over to UST yields though. US Tsys yields were lower today with the 2Y 1.1bps lower while the 10y is 1.6bps lower, reflecting a slight flattening in the curve.

- It was quiet in terms of dedicated US news flow today, other than Trump winning New Hampshire Rep Primary, while Nikki Haley has confirmed she will not be dropping out of the race.

- Later tonight, flash US PMIs, the BoC decision and 5Y supply

JGBS: Bear-Steepening, Market Looks To An Early Exit To NIRP

JGB futures are holding sharply lower but above the session’s worst level, -82 compared to the settlement levels, after traders judged comments from the BoJ on Tuesday to be hawkish.

- While the BoJ left all policy levers unchanged yesterday, the central bank expressed increased confidence in achieving its 2% sustained inflation goal, although without specifying the expected timeline. In the press conference, Governor Ueda struck a balance between the dovish tone of the statement and a reference to policy normalisation. Overall, the recent developments did little to alter expectations that the BoJ is poised to increase policy rates at the April meeting. (See MNI’s BoJ Review here)

- There hasn’t been much in the way of domestic data drivers to flag, outside of the previously outlined Trade Balance and Preliminary Jibun Bank PMIs.

- The cash JGB curve has sharply bear-steepened, with yields 1-10bps higher. The benchmark 10-year yield is 5.3bps higher at 0.724% versus the Nov-Dec rally low of 0.555%. The 20-year is the underperformer, with the 40-year yield 5.3bps higher at 2.078% ahead of tomorrow’s supply.

- The swaps curve has also bear-steepened, with rates 2-5bps higher. Swap spreads are tighter beyond the 5-year.

- Tomorrow, the local calendar sees Weekly International Investment Flows, Tokyo Condominiums for Sale, Dept Store Sales and Machine Tool Orders data.

BOJ: MNI BoJ Review - January 2024: Still On Track For An April Hike

Executive Summary

- The Bank of Japan (BoJ) retained the -0.1% short-term interest rate, alongside the soft 1.0% 'reference' target rate for the 10-year government bond yield. Forward guidance remained intact, with a commitment to "not hesitate to take additional easing measures if necessary."

- Notably, the central bank expressed increased confidence in achieving its 2% sustained inflation goal, although without specifying the expected timeline.

- In the Quarterly Outlook Report, the BoJ adjusted its forecast for core CPI excluding fresh food, revising it to 2.4% y/y from 2.8% for FY2024 but raising it to 1.8% from 1.7% for FY2025. A more hawkish development would have been if the FY2025 forecast was at or above 2%.

- In the press conference, Governor Ueda struck a balance between the dovish tone of the statement and a reference to policy normalisation. He highlighted the gradual rise in the BoJ's confidence, citing strong indications from firms about raising wages and the upward trend in service inflation.

- Overall, the recent developments did little to alter expectations that the BoJ is poised to increase policy rates by 10bps (to 0.00%) at the April 26th meeting.

- Full review here.

AUSSIE BONDS: Cheaper But Well Above Worst Levels, NZ CPI Eyed

ACGBs (YM -2.0 & XM -5.5) are weaker but well above Sydney session cheaps after rebounding from a mid-session slump. In the absence of market-moving data, the local market largely swung with offshore developments. That said, a relatively poor demand showing (cover ratio below 3.0x) at today’s Nov-33 ACGB auction did appear to add to lunch-time weakness.

- Offshore, there has been an extension of overnight weakness in US tsys in today’s Asia-Pac session, although there has been little follow-through on early selling. US tsys are flat to 1bp cheaper across benchmarks.

- There was also some spillover selling from NZGBs following the release of Q4 CPI data. NZGB benchmarks were as much as 4bps cheaper in post-CPI dealings, but that was pared to around 2bps following the release of the RBNZ’s core CPI measures.

- Cash ACGBs are 1-4bps cheaper, with the AU-US 10-year yield differential 2bps wider at +12bps.

- Swap rates are 1-3bps higher, with the 3s10s curve steeper.

- The bills strip is cheaper, with pricing -1 to -3.

- RBA-dated OIS pricing is 1-3bps softer for meetings beyond May. A cumulative 38bps of easing is priced by year-end.

- ICYMI, QTC launched a new 4.75% 2 February 2034 A$ fixed rate green bond. Transaction expected to price tomorrow.

- Tomorrow, the local calendar is empty.

AUSTRALIA: Tax Cut Plan Likely To Be Changed, Announced Thursday

PM Albanese is taking revised stage 3 tax cuts to the party room today and is likely to announce the plan and “cost-of-living” assistance tomorrow at 1230 AEDT at the National Press Club. During the 2022 election campaign, the Labor Party promised to implement the tax cuts of the previous government unchanged. After pressure from within the party and the union movement, that now appears to have changed ahead of a March by-election, May budget and next year’s election.

- The original proposal was meant to reduce the government’s reliance on income tax and was designed to flatten the income tax structure by having a 30% rate for those earning between $40k and $200k. The rates would drop from 32.5% and 37%. The top 45% bracket threshold would be increased $20k to $200k. These measures would already be in the RBA’s projections as they have been planned for some time.

- The Australian is reporting that the 37% rate for those earning more than $135k will be retained in the PM’s revised plan. The top 45% band will now start at $190k down from $200k. With the money saved being put into tax relief for those earning less than $135k, including a possible increase in the tax-free threshold. The PM has said that “everyone will be getting a tax cut” and the SMH has reported that he will say that the reform had to be altered due to global events since he was elected. Changes will require new legislation.

- Former Treasurer Costello has said that changing stage 3 will “unbalance the whole package”, according to The Australian. He noted that there has been significant bracket creep over the last 15 years. Business groups have said that the plan should be implemented unchanged on July 1 and they also criticised the states’ payroll tax.

AUSTRALIAN DATA: PMI Signals Profit Squeeze As Firms Absorb Higher Costs

The preliminary Judo Bank composite PMI for January increased to 48.1 from 46.9, signalling that growth was not quite as weak at the start of 2024 as at the end of 2023 and that the economy should still achieve a soft landing. Jobs growth continued and business confidence improved, while new business was slightly less negative across services and manufacturing. There was good news for the RBA with selling price inflation easing to close to a 3-year low.

- The growth in business costs was still above average in January driven by rising shipping and raw material prices but these were not fully passed onto customers so as to boost sales.

- Business sentiment improved on the back of expected rate cuts for 2024.

- The manufacturing PMI improved to 50.3 from 47.6, signalling a slight expansion in activity after contracting for 10 months. Respondents mentioned an increase in shipping delays from strike-related “port congestions” and tensions in the Middle East, which added to suppliers’ delivery times. New orders continued to fall but less so than in December. Employment contracted but at a slower pace.

- The services sector continues to contract but at a slightly slower rate with the PMI rising to 47.9 from 47.1. The 3-month average was stable at 47.0. Services continued to hire but at an easier pace. Cost and selling price inflation remained above the historical average.

- See Judo Bank PMI report here.

Source: MNI - Market News/Bloomberg

AUSTRALIAN DATA: NZ Signals Easing Aussie Q4 CPI But Also Sticky Domestic Pressures

Australian and NZ headline inflation have a correlation of over 90%, thus today’s NZ Q4 CPI suggests that there could be significant moderation in Australia’s when it is released on January 31. This is also in line with the 4.6% October/November average of the monthly CPI series. But just like in NZ, the details will be important, and NZ saw persistently sticky domestically-driven non-tradeables and core inflation in Q4. Just as with the RBNZ, this would make the RBA cautious when it meets in February.

- The correlation between the two countries’ non-tradeables inflation is around 90% and even higher for underlying measures. NZ’s non-tradeables inflation remained elevated and well above headline at 5.9% down from 6.3% in Q3.

- The RBNZ’s measure of core moderated to 4.5%, below headline, but core non-tradeables was stubbornly higher at 5%, down only 0.2pp.

- Services are a focus for the RBA given prices are significantly impacted by wages. NZ services inflation remained elevated but eased considerably to 4.7% from 5.6%.

Source: MNI - Market News/ABS/Refinitiv

NZGBS: Cheapen Further After Q4 CPI Details Keep Market Cautious

NZGBs closed 5bps cheaper across benchmarks, with the 10-year underperforming its US counterparts. At the local close, the NZ-US 10-year yield differential closed 3bps wider at +55bps.

- The underperformance came despite Q4 CPI data printing in line with consensus and below the RBNZ’s forecast. It was the details that had the market thinking the RBNZ would likely remain cautious given persistent domestically driven inflation. While the pace of increase in the domestically determined non-tradeables CPI eased to 1.1% q/q from 1.7% in Q3 and 1.5% in Q4 2022 (data is non-seasonally adjusted), annualised it is still at 4.3%. The annual rate moderated to 5.9% from 6.3%, which remains too high for the RBNZ to feel that the inflation fight has been won.

- On a more positive note, the RBNZ’s sector factor model later in the day showed core CPI inflation easing to 4.5% y/y in Q4 from 5.2% in Q3 and the peak of 5.7% in the previous three quarters. It was the lowest rate since Q4 2021.

- Swap rates closed 5-7bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 3-6bps firmer across meetings beyond February.

- Tomorrow, the local calendar sees the Government’s 5-month Financial Statements.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the Apr-27 bond, NZ$175mn of the May-34 bond and NZ$75mn of the Apr-37 bond.

NZ DATA: Inflation Moderates, Domestic Pressures Persist

While Q4 CPI printed in line with consensus and below the RBNZ’s forecast, the details show that the central bank is likely to remain cautious given persistent domestically-driven inflation. Headline rose 0.5% q/q moderating to 4.7% y/y from 5.6% in Q3. The RBNZ had projected 5% y/y. But the moderation was driven by the tradeables component, while non-tradeables rose 1.1% q/q.

- Housing and utilities drove the 0.5% q/q rise in the CPI but food prices put downward pressure on the index. Statistics NZ notes that around a third of items in the basket fell in Q4, which was “the most in over three years”.

- While the pace of increase in the domestically-determined non-tradeables CPI eased to 1.1% q/q from 1.7% in Q3 and 1.5% in Q4 2022 (data is non-seasonally adjusted), annualised it is still at 4.3%. The annual rate moderated to 5.9% from 6.3%, which remains too high for the RBNZ to feel that the inflation fight has been won.

Source: MNI - Market News/Refinitiv

- Non-tradeables inflation was driven by rents, construction and tobacco products.

- Tradeables fell 0.2% q/q bringing the annual rate down to 3% from 4.7% but there was downward pressure from overseas air transport.

- Both goods and services prices rose 4.7% y/y down around 1pp from Q3. Services posted the lowest rate since Q2 2022 and goods since Q2 2021.

- The RBNZ’s measure of core inflation is also released today at 1500 local time (1300 AEDT).

FOREX: Yen Outperforms On Higher JGB Yields, AS BoJ Outlook Assessed

Yen strength has been evident in the G10 FX space as the Wednesday session has progressed. The BBDXY sits a touch below NY closing levels but is still holding above 1238 at this stage.

- Slightly lower USD index levels are largely due to a firmer yen backdrop. USD/JPY is back sub 148.00, the pair around 0.40% stronger in yen terms (last near 147.80).

- A modest move and well above Tuesday lows (146.99), but JGB yields have risen strongly as traders assess the risks around a BoJ move in the first half of the year. The 10yr US-JP government bond yield differential is back sub +340bps, comfortably off recent highs (near +350bps). Outright 10yr JGB yields are back to 0.74%, fresh highs since mid Dec last year.

- AUD and NZD have lost some ground against the USD, with yen cross sales a potential factor. AUD/USD last near 0.6570, off close to 0.20%. NZD/USD is down 0.10%, so outperforming slightly, the pair last near 0.6095.

- Earlier we had stronger than expected non-tradables Q4 inflation, which has helped the Kiwi at the margins.

- Looking ahead, a host of European Flash PMIs preview the latest strength of regional economies. The Bank of Canada rate decision will also highlight.

EQUITIES: Equities Mixed As Traders Bet on BoJ Rate Hikes

Regional equities are mixed today with China and Japanese Equities lower. US Equity futures have again continued their trend higher, led by Nasdaq futures, up 0.35%, while Eminis were last +0.22% higher.

• Japan Equity indices are lower today as investors weighed comments late yesterday from BoJ Governor Ueda. A potentially earlier NIRP exit saw the 10Y yield move 10bps higher and 30Y yield moved 12.5bps higher. This led the move lower in equities with the Nikkei 225 down 0.902%, while the Topix is down 0.70% at this stage.

• Hong Kong extended gains from yesterday in part as a continuation from yesterday's announcement around a rescue package for to boast China equity markets, Hang Seng currently trading 0.45% higher today at the break. Share buybacks for Alibaba (from owner Jack Ma) have also aided sentiment.

• China regulators ask funds to restrict short selling of stock index futures (RTRS), still mainland equities all trading lower today with the CSI 300 down by 1.0% at this stage.

• In Australia, the ASX 200 is trading flat today, miners have performed as China steel demand grows. In SEA markets, Philippines are trading 0.70% higher and India is 0.80% higher continuing their winning streaks.

OIL: Crude Little Changed As Geopolitics Offset Fundamentals

Oil prices have traded in a tight range and are little changed during APAC trading today as continued geopolitical tensions offset soft supply fundamentals, a trend that has been in place through January. WTI is at $74.28/bbl, close to the low, and Brent hasn’t been able to break through $80 and is currently at $79.44 following a low of $79.43. The slightly lower US dollar hasn’t provided a boost to crude.

- Supply is expected to remain plentiful and with production beginning to come back on line in Libya following protests and in the US after a cold snap, markets are struggling to rally. But Brent’s bullish prompt spread’s backwardation structure has widened over January, signalling a tightening market.

- Bloomberg reported that US crude inventories fell 6.67mn barrels in the latest week, according to people familiar with the API data. Gasoline rose 7.18mn but distillate fell 245k. The data is likely impacted by recent very cold weather which reduced output and refining. The official EIA data is released today.

- Later preliminary January PMIs for US/Europe are released and the Bank of Canada’s decision is announced.

GOLD: January’s Narrow Range Continues To Hold

Gold is slightly weaker in the Asia-Pac session, after closing 0.4% higher at $2029.28 on Tuesday.

- Bullion has traded in a relatively narrow range this month as investors seek further clues on whether the Federal Reserve will start reducing interest rates as soon as March. Lower interest rates are typically positive for non-interest-bearing gold.

- The market is currently assigning less than a 50% chance to a 25bp rate cut in March. This compares to the near 70% chance seen a week ago.

- Fed speakers are in blackout ahead of next week’s FOMC meeting.

- US data scheduled for later in the week include the latest GDP figures and core PCE index, which is the central bank’s preferred gauge of underlying inflation and will likely drive sentiment for the precious metal in the short term.

ASIA FX: CNH Loses Ground, Weaker Spot Levels For THB & IDR, BNM Still To Come

USD/Asia pairs have had a positive bias for today's session. USD/CNH gains have been in focus, with the pair back above 7.1700. Elsewhere spot USD gains have reflected catch up to Tuesday dollar gains, with NDF levels relatively steady. Still to come is the BNM decision in Malaysia with no change expected. Then tomorrow we have South Korean business sentiment early, followed by Q4 GDP. Later on, Hong Kong trade data prints for Dec.

- USD/CNH sits higher today, the pair last above 7.1700, but unable to crack above 7.1800 in earlier trade. Funding conditions in the CNH have eased somewhat, TN back at +2.9, while CNH deposit rates have edged down. This has worked against CNH at the margin, while local equities have struggled to build on yesterday's gains. We have a PBoC press conference at 3pm local time, where economic conditions are likely to be discussed.

- 1 month USD/KRW hasn't spent too much time outside of a 1336/1338 range so far today. Local equities have struggled but this hasn't been a meaningful headwind for the won. North Korea fired cruise missiles in the latest sign of tensions, but again market impact was negligible. Earlier consumer confidence rose, while inflation expectations eased.

- In India, HSBC Jan P PMIs have shown sequential improvement on the Dec outcomes. The manufacturing up to 56.9 from 54.9 prior. Services rose to 61.2 from 59.0. This paints a resilient growth backdrop. INR us relatively steady though, last near 83.15, maintaining a very low vol to broader USD trends.

- USD/IDR spiked higher in early trade, but is off earlier highs. Spot's move above 15700 was largely reflective of NDF weakness in US trade on Tuesday as US real yields printed fresh multi-week highs. We haven't been above 15700 since Nov last year.

- USD/THB also rallied strongly from the open, but we are seeing some resistance around the 35.85/90 region, which is a touch above mid Dec highs from last year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/01/2024 | 0815/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 24/01/2024 | 0815/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 24/01/2024 | 0830/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 24/01/2024 | 0830/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 24/01/2024 | 0900/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 24/01/2024 | 0900/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 24/01/2024 | 0900/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 24/01/2024 | 0930/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 24/01/2024 | 0930/0930 | *** | | UK | S&P Global Services PMI flash |

| 24/01/2024 | 0930/0930 | *** | | UK | S&P Global Composite PMI flash |

| 24/01/2024 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 24/01/2024 | 1100/1100 | ** | | UK | CBI Industrial Trends |

| 24/01/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 24/01/2024 | 1445/0945 |  | CA | BOC Monetary Policy Report | |

| 24/01/2024 | 1445/0945 | *** | | CA | Bank of Canada Policy Decision |

| 24/01/2024 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/01/2024 | 1445/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/01/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 24/01/2024 | 1530/1030 | | CA | BOC Governor Press Conference | |

| 24/01/2024 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 24/01/2024 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.