Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

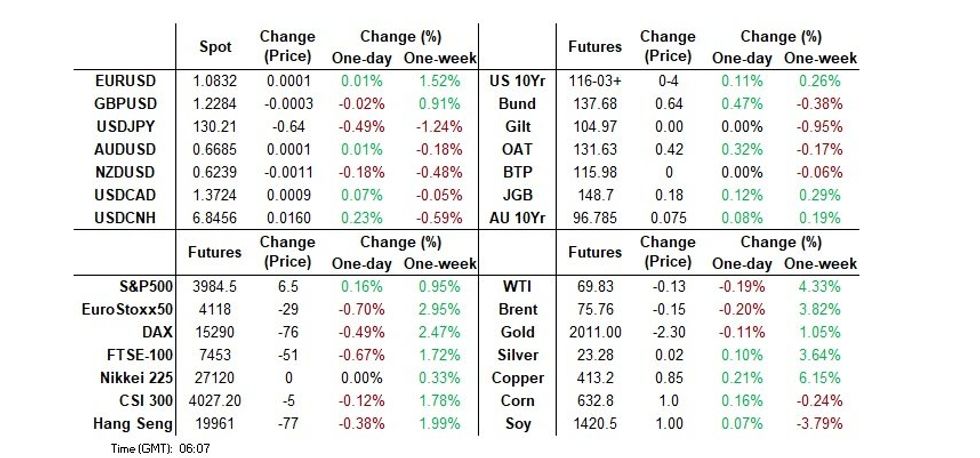

- USD/JPY sits a touch off session lows into London trade. The yen is the strongest performer in the G-10 FX space. U.S. Treasury yields have ticked lower, boosting demand for the JPY.

- Broader risk assets struggled in early Asia-Pac trade, without much of a headline driver evident. A bid in Hong Kong tech names then seemed to stabilise wider risk sentiment, allowing e-minis to trade back in the green.

- Flash PMI data from across the globe, along with Fedspeak from Bullard, ECB speak from across the hawk-dove spectrum and further commentary from BoE's Mann headline ahead of the weekend.

US TSYS: Richer In Asia, TYM3 Bid Capped At Thursdays Highs

TYM3 deals at 116-05+, +0-06, with a 0-18 range observed on volume of ~134k.

- Cash tsys sit 4-5bps richer across the major benchmarks, the belly is leading the bid.

- The short end of the treasury curve was cheaper in early dealing as Asia-Pac participants digested remarks late in yesterday's NY session by Tsy Sec Yellen, she softened her language on deposit insurance pledging additional actions if warranted.

- Despite the absence of a headline driver tsys firmed off session lows. The bid extended as e-minis retreated from best levels and the USD firmed alongside the Yen.

- The bid was capped as TYM3 failed to break Thursday's NY session high (116-08) and 2s failed to break 3.75% as yields moved lower.

- Despite marginally paring gains tsys have held richer as we approach the European session.

- Preliminary PMIs from France, Germany and EU headline in Europe. Further out we have Durable Goods Orders and US flash IHS Markit Manufacturing Index and S&P Global Services Index. Fedspeak from St Louis Fed President Bullard will also cross.

JGBS: Contained End To The Week, Twist Steepening Evident

JGB futures operated in a contained range in the grander scheme of things, failing to challenge the extremities witnessed in the overnight session during Tokyo dealing. Gyrations in U.S. Tsys were in the driving seat for the most part, outside of the early super-core CPI-related blip lower, while weakness in the longer end of the JGB curve became more pronounced, before fading.

- JGB futures are +10 into the close, while cash JGBs are 3.5bp richer to 2bp cheaper, with 40s the only benchmark softening on the day.

- The swap space has been more non-committal, operating within -/+0.5bp of yesterday’s closing levels at typing.

- In terms of the details, national CPI data saw the headline and excluding fresh food measures experience Y/Y moderations that were in line with expectations, owing to government subsidies surrounding energy. Meanwhile, the excluding fresh food and energy metric saw a larger than expected uptick, topping expectations by 0.1ppt to print a fresh cycle high at +3.5% Y/Y (incoming BoJ Governor Ueda had previously pointed to peak inflation being in the rear view).

- Services PPI data headlines Monday’s domestic docket.

JAPAN: Global Banking Worry Triggers Huge Bond Purchases

Bond flows dominated when it came to the latest round of weekly international security flow data provided by the Japanese MoF, with the tumult surrounding the global banking sphere and related central bank repricing at the fore in the week ending 17 March.

- Japanese investors lodged the second largest ever round of net purchases of foreign bonds as a result, with the amount only surpassed by one week of net purchases observed during the initial COVID outbreak.

- Foreign investors recorded the largest ever round of weekly net purchases of Japanese bonds, adding further momentum to post-BoJ short cover.

- On the equity side Japanese investors were small net buyers of international equities, breaking a run of seven straight weeks of net sales. Meanwhile, international investors were net sellers of Japanese equities for a fourth consecutive week, registering the largest round of weekly net sales seen since September of last year in the process.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 3334.8 | 914.2 | 4308.6 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 118.2 | -169.7 | -540.1 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 4095.7 | -146.1 | 2937.8 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -1080.6 | -835.6 | -2914.2 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

AUSSIE BONDS: At Bests Ahead Of Key Local Data Releases

ACGBs closed just shy of bests (YM +7.0 & XM +7.5) after U.S Tsys re-visited but failed to breach NY highs in Asia-Pac trade. Cash ACGBs richened 6-7bp with the 3/10 curve 1bp flatter and the AU-US 10-year yield differential -1bp at -16bp.

- Swaps closed 5-6bp stronger with the 3s10s 1bp flatter and EFPs 1-2bp wider.

- Bills strip flattened with pricing +1 to +10.

- A subdued session for RBA dated OIS with pricing 1-6bp softer across meetings with 30bp of easing priced by year-end. April meeting pricing was at +2bp.

- The AOFM released its weekly Issuance schedule with a planned sale of A$150mn of 0.75% Nov-27 indexed bond (Tue), A$800mn of 3.75% May-34 bond (Wed) and A$500mn of 0.25% Nov-25 bond (Fri).

- After a light few days, the calendar heats up again next week with the scheduled release of February Retail Sales (Tue) and Monthly CPI (Wed). These two releases were highlighted in the RBA Minutes as important inputs to the April policy decision.

- Until then, the market’s attention will be on U.S. Tsys and global STIR as it continues to process the dovishly perceived hike by the Fed this week.

NZGBS: Closes At Bests

NZGBs close at session bests after richening with U.S. Tsys but then failing to weaken with them after they bounce off NY highs. The 2-year and 10-year cash benchmarks closed respectively 8bp and 4bp stronger with the 2/10 curve 4bp steeper. NZ/US & NZ/AU cash 10-year yield differentials closed respectively +1bp at +72bp and +2bp at +88bp.

- Swaps closed 6-7bp richer, implying a flatter swap spread box, with the 2s10s curve 1bp flatter.

- RBNZ dated OIS pricing closed 2-10bp softer for meetings beyond April with terminal rate expectations at 5.14%. April meeting pricing continued to hold in its recent 20-25bp of tightening range at 23bp.

- The NZ calendar is light until late next week with the first major release being ANZ Business Confidence and Building consents on Thursday.

- A more interesting data week for Australia with the scheduled release of February retail sales (Tue) and monthly CPI (Wed). These two releases were highlighted in the RBA Minutes as important inputs to the April policy decision.

- With the global calendar light today, the global roll-out of flash PMIs as the highlight, the market attention will be on U.S. Tsys as it continues to process the dovishly perceived hike by the Fed this week.

BONDS: AU Curve Too Flat Vs. U.S.

The change in narrative over recent weeks from data dependency to global banking concerns delivered a sharp 45bp steepening in the U.S. Tsy 2/10 curve. On the back of hawkish messaging from Fed Chair Powell in early March, the U.S. cash curve had moved to -107bp, it's most inverted since the 1980s.

- In sympathy with U.S. Tsys, the AU 3/10 curve also steepened as global curve correlations returned as the key driver.

- Prior to recent adverse credit developments, the AU curve had been trading in a 25-60bp range. Moreover, domestic developments had been imparting a significant influence on AU curve movements consistent with the notion that global curve correlations lessen as the tightening cycle matures and policy rates follow their independent paths.

- A simple regression of the AU 3/10 – US 2/10 curve box against the AU 3-year/US 2-year yield differential (over the tightening current cycle) suggests the AU curve is 10-15bp too flat relative to the US curve given the AU-US short-end yield differential.

- When global banking concerns dissipate, one would expect the AU 3-year/US 2-year yield differential to re-exert itself as the key driver of relative curve movements.

Fig. 1: AU 3/10 – US2/10 curve box (% Y-Axis) Vs. AU 3-year/US 2-year Yield Differential (% X-Axis)

Source: MNI – Market News / Bloomberg

BONDS: AU/NZ 10-Year Yield Differential Lifts Off Low

AU/NZ cash 10-year yield differential has pushed 10bp higher this week to -88bp versus its multi-decade low of -100bp set in the wake of the worse-than-expected deterioration in NZ’s current account deficit (-8.9% of GDP).

- NZGB 10-year benchmark’s outperformance versus ACGB has been consistent with the relative price movement in AU and NZ STIR. NZ 1-year forward 1-month (1y1m) OIS has outperformed AU by 16bp over the past week as $-Bloc STIR has priced additional easing this year after a perceived dovish hike by the FOMC.

- A simple regression of the NZ/AU 10-year yield differential on the AU/NZ 1y1m OIS differential (over the current tightening cycle) however suggests the 10-year yield differential remains 15-20bp too negative, most likely reflecting the divergent current account situations in AU (record surpluses) and NZ (record deficits).

Fig. 1: AU/NZ 10-Year Yield Differential (%) Vs. AU/NZ 1y1m OIS Differential (%)

Source: MNI – Market News / Bloomberg

FOREX: Yen Firmer In Asia, NZD Pressured

USD/JPY sits a touch off session lows. The pair is ~0.5% lower and the yen is the strongest performer in the G-10 space at the margins. US Treasury yields have ticked lower, boosting demand for the JPY.

- USD/JPY prints at ¥130.15/25, the next downside target is ¥129.75 76.4% retracement of the Jan 16 to Mar 8 rally. On the wires this morning Japan's February National CPI crossed. Headline (3.3%) and Core (3.1%) figures were in line with expectations. Core-core measure was a touch above expectations at 3.5%.

- Kiwi is the weakest performer in the G-10 space today thus far. NZD/USD prints at $0.6235/40 ~0.2% softer. ANZ downgraded their milk price forecast to $8.25/kg. The NZ Ministry said the economy may have shrunk in Q1 due to Cyclone Gabrielle.

- AUD/USD is little changed from yesterday's closing levels, the pair was pressured in early dealing as e-minis came off best levels and sparking a risk off move seeing the USD and Yen firm alongside US Treasuries. Support was seen at $0.6660 and AUD/USD pared losses.

- Cross asset wise, US Treasury Yields are ~4bps lower across the curve. E-minis are up ~0.1% and Hang Seng is marginally softer. BBDXY is flat.

- Preliminary Services and Manufacturing PMIs from France, Germany and EU headline in Europe. UK Retail Sales and flash Services and Manufacturing PMI will also print. Further out we have Durable Goods Orders and US flash IHS Markit Manufacturing Index and S&P Global Services Index.

FX OPTIONS: Expiries for Mar24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600-05(E1.7bln), $1.0675-80(E627mln), $1.0700-10(E1.4bln), $1.0800(E1.6bln), $1.0850(E539mln), $1.0875(E509mln), $1.0890-10(E656mln)

- USD/JPY: Y130.00($830mln), Y131.00($592mln), Y132.95-00($1.3bln), Y133.75($749mln)

- EUR/GBP: Gbp0.8900(E635mln)

- AUD/USD: $0.6700(A$669mln)

- USD/CAD: C$1.3600-05($606mln), C$1.3620-30($1.1bln)

- USD/CNY: Cny7.3635($1.4bln)

EQUITIES: Asia-Pac Equities Struggle Even With Hang Seng Tech Bid, E-Minis Nudge Higher

Broader risk assets struggled in early Asia-Pac trade, without much of a headline driver evident.

- A bid in Hong Kong tech names then seemed to stabilise wider risk sentiment, allowing e-minis to trade back in the green.

- The bid in Hong Kong tech names was aided by after hours news from Thursday, which saw Beijing release its regular round of computer game approvals, which will have supported related names. Also of note, Meituan, the food delivery company, will report Q4 earnings later today.

- The Hang Seng Tech Index is off best levels, but still prints more than 1% firmer on the day.

- Broader financials generally struggled after a heavy session for U.S. bank names on Thursday, with the well-documented worry re: the space still reverberating.

- The major regional equity benchmarks all trade lower, albeit by less than 1%, while the 3 major e-mini contracts are 0.1% better off into London hours.

GOLD: Thursday’s Gains Consolidated In Asia

Bullion has consolidated Thursday’s gains during the final Asia-Pac session of the week, last dealing little changed, just above the $1,990/oz mark. Spot once again failed to consolidate above $2,000/oz on Thursday, after drawing support from shifts in market pricing which pointed to deeper Fed cuts through late ‘23/early ’24. Still, gold managed to register the highest daily close since March of last year.

- Technically, trend conditions in gold remain bullish. The breach of former resistance at the Feb 2 high confirmed a resumption of the bull trend that started in late September ‘22. The recent forays above $2,000/oz open the way to $2,034.0/oz (a Fibonacci projection), which represents the next meaningful area of technical resistance.

- Known ETF holdings of gold continue to tick away from cycle lows, with the well-documented worry re: the global banking sector and associated repricing in the outlook for interest rates across the major global central banks in the driving seat there.

- Looking ahead, U.S. durable goods orders and flash S&P global PMIs present the headline data points ahead of the weekend, while comments from St. Louis Fed President Bullard are also due.

OIL: Recovering From Early Asia Lows To Trade Little Changed

WTI and Brent initially extended on Thursday’s weakness with risk assets on the defensive in early Asia-Pac trade, before stabilising as e-minis recovered and the Hang Seng Tech Index firmed, leaving the global oil benchmarks $0.10 or so below their respective settlement levels into London hours. Still, WTI & Brent remain on track to snap a two-week streak of weekly net losses.

- To recap, crude tracked broader risk sentiment for the most part on Thursday, before legging lower late in the day as US Energy Secretary Granholm noted that it will be somewhat “difficult” to refill the SPR during ’23, even with crude prices operating within the already disclosed target purchase band. This also fed into early Asia-Pac price action.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/03/2023 | 0700/0800 | ** |  | SE | PPI |

| 24/03/2023 | 0700/0700 | *** |  | UK | Retail Sales |

| 24/03/2023 | 0730/0730 | | UK | DMO to Publish Apr-Jun Gilt Op Calendar | |

| 24/03/2023 | 0800/0900 | ** |  | ES | PPI |

| 24/03/2023 | 0800/0900 | *** | | ES | GDP (f) |

| 24/03/2023 | 0815/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 24/03/2023 | 0815/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 24/03/2023 | 0830/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 24/03/2023 | 0830/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 24/03/2023 | 0900/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 24/03/2023 | 0900/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 24/03/2023 | 0900/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 24/03/2023 | 0930/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 24/03/2023 | 0930/0930 | *** | | UK | S&P Global Services PMI flash |

| 24/03/2023 | 0930/0930 | *** | | UK | S&P Global Composite PMI flash |

| 24/03/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 24/03/2023 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 24/03/2023 | 1330/0930 | | US | St. Louis Fed's James Bullard | |

| 24/03/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/03/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/03/2023 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 24/03/2023 | 1500/1500 | | UK | BOE Mann Panellist at Global Independence Center Conference Ukraine | |

| 24/03/2023 | 1630/1630 | | UK | BOE Announces Q2 Active Gilt Sales Schedule |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.